What is the true cost of home ownership? A closer look at which is best between a 30-year fixed mortgage rate or a 15-year fixed mortgage rate…

Have you ever been in a situation where you wanted to buy something really bad? Maybe it was something that you wanted really bad, but you really didn’t quite need it.

Just for hypothetical sake, let’s say you really need (I’ll say want) the new Apple iPad with its nice entry price of $499. You have to buy it, but unfortunately, you don’t have the cash right now, so you buy it on credit.

Everyone else is doing it, why not you?

Needing a line of credit you head to the first lender and they strike you a deal that will allow you to pay it back over 3 months for $200 per month.

Over the 3 months, you’ll pay a total of $600 of which $100 is interest. Not sure if you’re getting the best deal you shop around and head to the 2nd lender.

The 2nd lender entices you with a sweet offer that only makes you pay $125 a month but you do so for a 6-month period. The grand total you’ll pay is $750 of which $250 is interest.

Although with the second lender, you pay less per month, it takes you longer to own your iPad and you end up paying one and a half times what it is actually worth! How bad do you really need it?

Table of Contents

Which Loan Would You Choose?

If a similar situation, which lender would you borrow from? As I’m sure you can tell, there is a lot of similarity in buying a home.

When you’re deciding between a 15-year mortgage and a 30-year mortgage, be sure to consider and weigh all the pros and cons before making your decision.

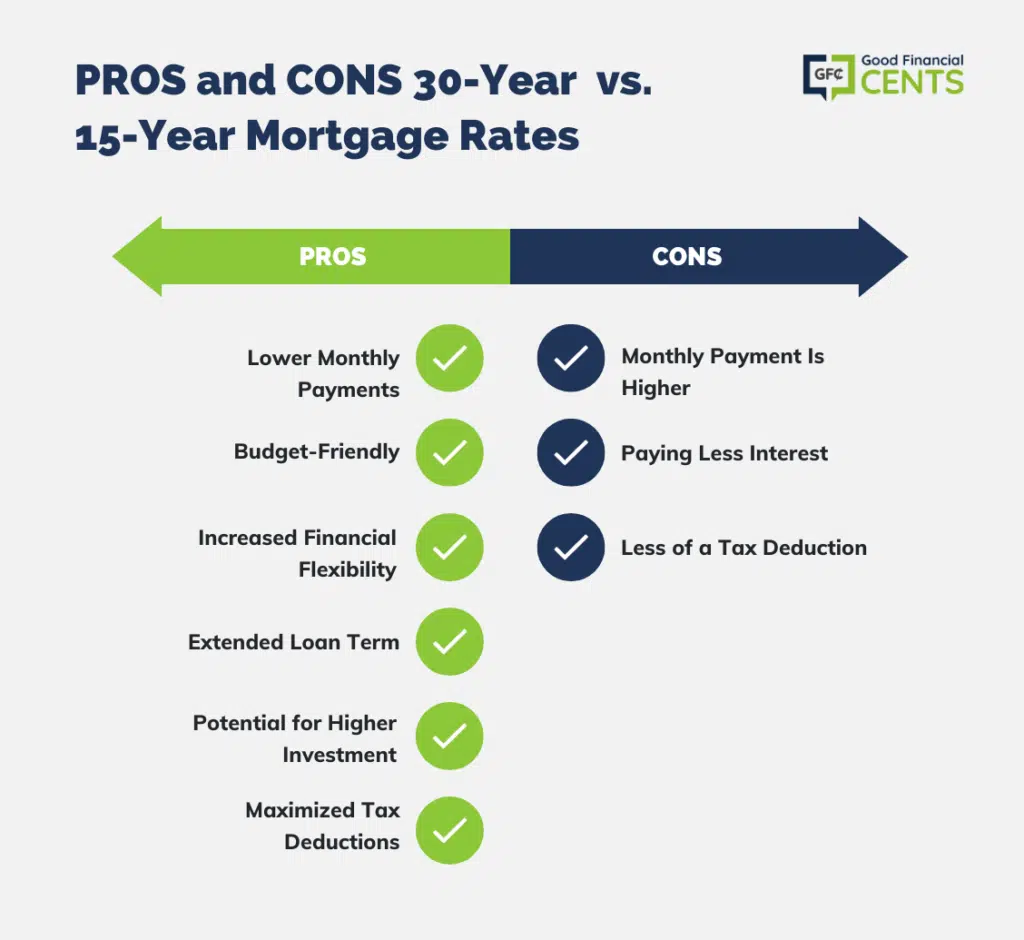

Pros of Choosing a 30-Year Mortgage Rate Over 15 Year Mortgage Rate

In general, the reason most homebuyers take out a 30-year mortgage is because they cannot afford (or think they cannot afford) a higher monthly payment.

But if you can find a way to make a 15-year mortgage rate work within your budget, it could really pay off in the long run.

You would own your home sooner and pay less for it (ultimately), and you would probably also lock in your mortgage at a lower interest rate.

For example … Let’s say you want to buy a house for $300,000. If you took out a 30-year fixed rate mortgage at 6.5%, you’d pay around $1900 per month. In the end, you will have spent $300,000 on your house, and $382,633 on interest.

That’s a total of $682,633 … over twice the price of your home.

If you bought the same house with a 15-year fixed rate mortgage at 6.0%, your monthly payment would be about $2,532.

However, at the end of 15 years, you will have spent only $455,682. That’s $300,000 on the house and only $155,682 on interest.

That’s $226,951 less than with the 30-year mortgage!

What Could You Do With an Extra $226,951?

That “extra” money could be invested, used to fund your child’s education, used to renovate the house, etc.

It’s up to you to decide if the additional money paid each month is worth the long-term payoff.

REMEMBER:

Cons in Choosing 15 Year Mortgage Rate Over 30 Year Mortgage Rate

Being overzealous in paying down your home mortgage does have its risks. The first

What are the downsides? Well, the most obvious downside is that the monthly payment is higher.

This can mean significantly altering your spending habits.

Another Downside:

Making an Extra Payment

While the attraction of having your house paid off in 15 years sounds exciting, it’s a pipe dream for many.

My wife and I had toyed with the idea of choosing a 15-year mortgage for our new house, but when we started to crunch the numbers we realized that we were dreaming and dreaming big.

Our solution was to make an extra payment per year.

For example, if you use the example above, a $300,000, 30-year fixed-rate mortgage at 6.5%, and if we contribute just $200 extra each month (0r $2400 per year) toward the principal, we could potentially pay off our mortgage nearly 7 years sooner and save over $100,000 in interest.

For us, we get the benefit of paying off the mortgage sooner while not having to be tied down to a higher monthly payment in case we have any unexpected jolts to our income later on in life. Typically, this is the same method that I would suggest to most.

There’s a lot of value in flexibility and leaving your options open.

Bottom Line: 30-Year vs. 15-Year Mortgage Rates

Choosing between a 15-year and 30-year mortgage hinges on your financial capability and long-term goals.

While a 15-year mortgage means higher monthly payments, it offers significant savings on interest and a quicker route to full homeownership. Conversely, a 30-year term has lower monthly payments but accrues more interest over time.

However, flexibility can be achieved with a 30-year mortgage by making extra payments, accelerating the payoff timeline, and still maintaining manageable monthly expenses. Make an informed choice considering both immediate budget constraints and long-term benefits.