One of the best things you can do for your finances is to pay down debt. There are a number of different strategies designed to help you get rid of your debt.

Among the more popular strategies is debt consolidation. With debt consolidation, you gather all your debts in one place.

You can get a debt consolidation loan that pays off all the smaller loans and leaves you with the larger loan, or you can manage your debt consolidation through a third party, which collects payment from you and then disburses it to your creditors.

Debt consolidation can be a great way for some consumers to put a solid dent in their debt.

This is because it gets all of the debt in one place, where it can be easily managed. You only have one payment to worry about, and one interest rate. Being able to concentrate your efforts can go a long way toward getting rid of debt.

However, debt consolidation isn’t for everyone, and it’s no guarantee that you will be able to get rid of your debt effectively — especially if you fall prey to the following 3 pitfalls:

Table of Contents

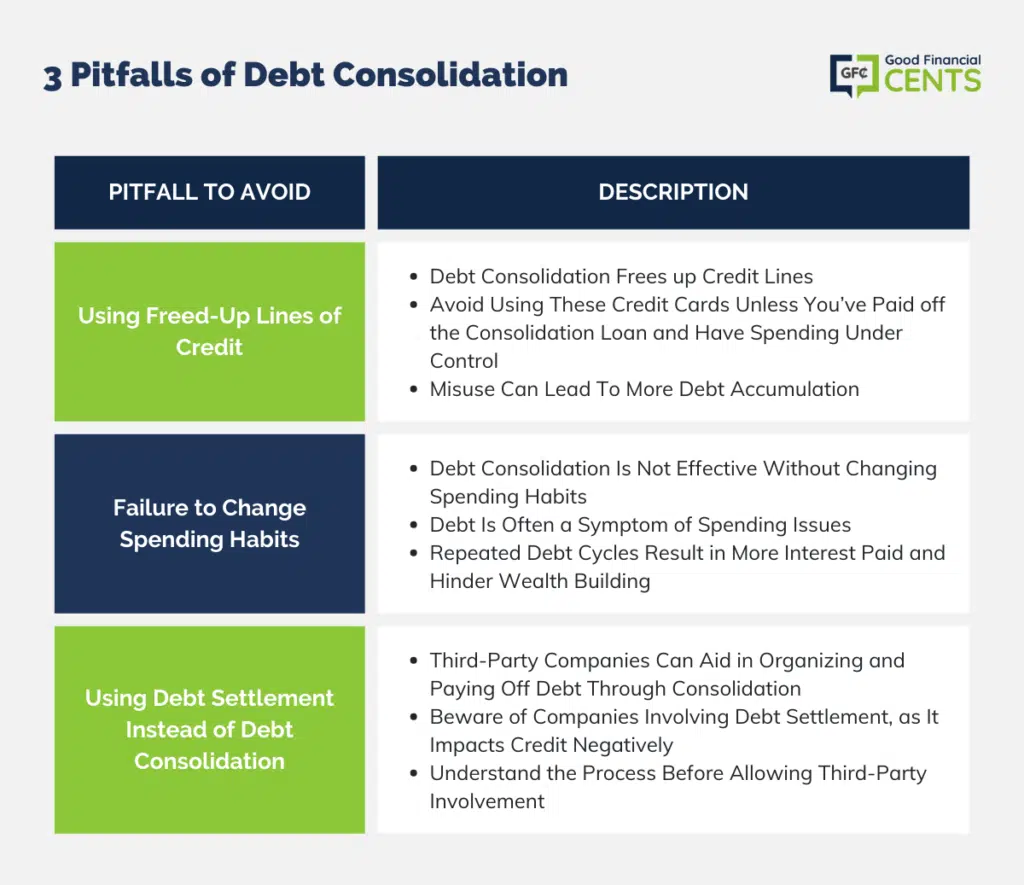

1. Using Your Freed-Up Lines of Credit

If you get a debt consolidation loan, the result is more freedom in terms of lines of credit. You paid off your credit card balances with the debt consolidation loan, so now you have fully available credit cards.

Many consumers start using these credit cards again as soon as the debt consolidation process is complete.

This can be a huge mistake. Savvy use of credit cards with 0 APR can be helpful, but you have to pay off the balances each month in order to avoid high-interest charges. If you continue to use your credit cards and carry balances, you will rack up even more debt than you had to begin with.

Don’t use your freed-up lines of credit unless you are done paying off your debt consolidation loan, and your spending is under control so that you aren’t living beyond your means.

I worked with one person who borrowed money using Lending Club to pay off all their high-interest debt. 18 months later they had double the debt and no way to consolidate. Don’t be this person!

2. Failure to Change Your Spending Habits

If you aren’t planning to completely change your spending habits, debt consolidation — in any form — isn’t going to help you. You need to stop thinking of debt as the problem.

In most cases, debt isn’t the problem; it’s a symptom of your spending problem.

You can pay off debt time and time again, but unless you change your current habits, and make a fundamental shift in the way you approach your money, you will end up back in debt.

The more times you go through the debt cycle, the more interest you pay. This eats into your ability to build wealth over the long haul.

If you want to really make your debt consolidation effort a success, your plan has to be accompanied by fundamental changes in the way you handle your money.

3. Using Debt Settlement Instead of Debt Consolidation

A third-party company can help you organize your debt, and pay it off quickly through a form of consolidation. Properly certified credit counselors can help you create and execute a pay-down plan. You make one payment, and the company handles all of the transactions.

You will be charged a fee for the service, but for some consumers, this fee amounts to less than they would have paid in interest had they continued struggling with a debt pay-off plan on their own.

What you have to watch out for are companies that actually involve you in debt settlement rather than debt consolidation. With debt settlement, you make regular payments to the company, and the money is held in an account.

The company withholds payment from your creditors. After a time, your creditors are willing to settle for a lump sum payment that is less than what you owe. The money you have been paying into an account is used to settle with your creditors.

However, this process takes a very large toll on your credit. As long as you keep making payments on time, your debt consolidation efforts won’t likely have a huge impact on your credit score (although your credit utilization will remain high).

Go through debt settlement, though, and your payment history — the largest factor in determining your score — will be destroyed.

Editor’s Note

Before you agree to allow a third party to handle your debt consolidation, make sure you understand what it entails and that you truly understand the process.

The Bottom Line – Avoid These 3 Pitfalls of Debt Consolidation

Debt consolidation, a strategic approach to financial stability, can be a lifeline for individuals overwhelmed by multiple debts. However, it’s not a one-size-fits-all solution.

The effectiveness of this strategy hinges on disciplined financial behavior, avoiding the temptation of available credit, and a thorough understanding of the consolidation process.

Missteps, such as falling back into old spending habits or mistaking settlement for consolidation, can exacerbate financial woes. For those willing to adapt and remain vigilant, debt consolidation can be a stepping stone toward fiscal responsibility and long-term financial health.

I think it’s no surprise that the first two pitfalls focus on changing your financial habits. With enough time and determination anyone is likely to pay off their debts, but so many just dig a new hole for themselves because they never took the time to fix what is wrong – their financial habits. If one can master those, then debt will never become a problem again!

Very useful tips shared.. The detailed explanation of debt settlement is something which i have found the most useful here.. I think being thrifty is the way to go till the entire debt is paid off.. no matter in whatever situation you are as a borrower!

As always great tips. Getting debt under control is like a war that you must win. Defeat isn’t an option.

One avenue for the debt consolidation loan might be Peer 2 Peer lender like Lending Club or Prosper. Once you get the debt monster under control, start the emergency savings plan. By the way down the line Lending Club and prosper are good places to invest as well