In an increasingly digitized world, having access to banking services is nearly as essential as having a home address or a phone number. A bank account is often the cornerstone of personal financial management, enabling individuals to receive income, pay bills, and save money.

However, for various reasons, some people cannot open a standard bank account. This predicament can be due to a range of factors, including a lack of required documentation, poor credit history, or previous banking issues such as unpaid overdraft fees. For those in such a situation, it’s important to understand that there are alternatives available.

Table of Contents

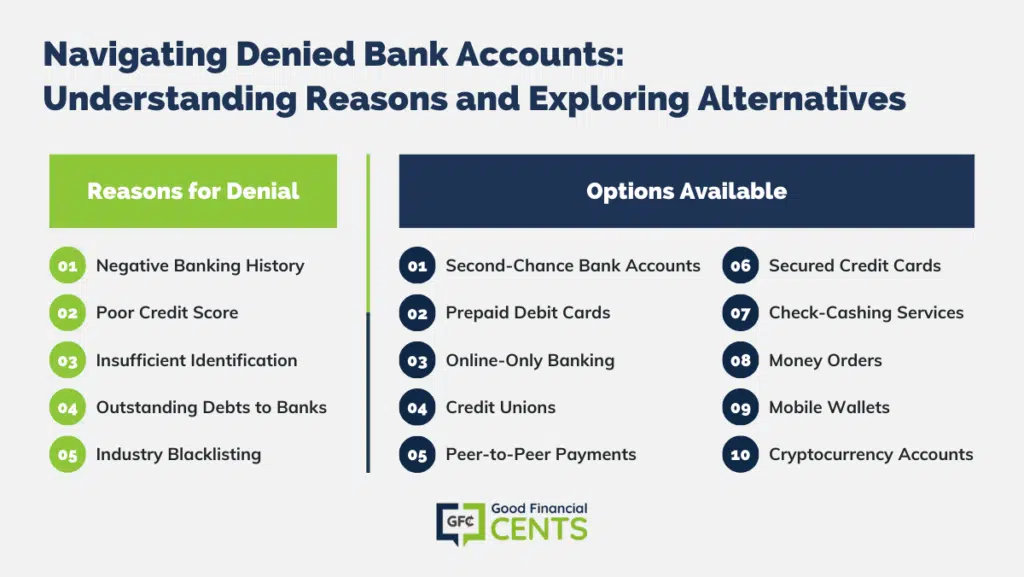

Reasons for Being Denied a Bank Account

Before delving into the alternatives, it’s crucial to understand why someone may not have access to a traditional bank account. Banks typically use systems like ChexSystems, a reporting agency that provides information about how individuals manage checking and savings accounts.

Understanding the common reasons for such denials can help in taking proactive steps to manage one’s financial health and eventually secure banking services. Here are some prevalent reasons why an individual might be denied a bank account:

Negative Banking History

Banks and credit unions often use reports from systems like ChexSystems, Early Warning Services, and TeleCheck to assess the risk of potential customers. If an individual has a history of unpaid overdrafts, bounced checks, fraudulent activity, or account closures due to mismanagement, this information can lead to a bank choosing to deny a new account.

Poor Credit Score

Insufficient Identification

To comply with government regulations, including the USA PATRIOT Act, banks require specific identification to open an account. Suppose someone cannot provide adequate identification, such as a government-issued ID, Social Security number, or proof of address. In that case, the bank may not be able to legally open an account for them.

Outstanding Debts to Banks

Owing money to another bank, especially if it’s due to unpaid fees or overdrafts, can result in a denial of service. Banks are interconnected in more ways than ever, and they share information about delinquent accounts that can affect your standing with other financial institutions.

Industry Blacklisting

Rarely, individuals involved in industries considered to be ‘high-risk’ by financial standards (such as the gambling industry or cryptocurrency exchanges) may be denied a bank account based on their professional activities alone.

However, even if you are denied a regular checking account because of your history, you do have other options to look into.

Options Available

Second-Chance Bank Accounts

Many financial institutions offer “second-chance” bank accounts aimed at individuals who have been rejected for standard accounts. These accounts may come with monthly fees or have more restrictive terms, such as no overdraft facilities, but they provide most services that standard accounts do. Over time, with good financial behavior, customers can often upgrade to a regular account.

Prepaid Debit Cards

Prepaid debit cards function similarly to traditional debit cards but aren’t linked to a checking account. Users can load money onto the card and use it for purchases, bill payments, and even ATM withdrawals. While they can be a convenient alternative, it’s essential to be aware of potential fees for activation, reloading, and maintenance.

Online-Only Banking

Fintech companies have emerged as significant players in the financial services sector, offering online-only banking solutions. These institutions often have lower overhead costs and can provide services to those who have had difficulties with traditional banks. However, customers must be comfortable managing their accounts entirely through a website or mobile app.

Credit Unions

Credit unions are nonprofit organizations that offer many of the same services as banks but are typically more lenient with their requirements. Since they are community-based and member-owned, credit unions can be more flexible and provide a more personalized banking experience.

Peer-to-Peer Payments

Services like PayPal, Venmo, and Cash App allow users to receive and send money without a traditional bank account. While these can be convenient for casual transactions, they may not be suitable for all financial needs, such as receiving a steady paycheck or paying rent.

Secured Credit Cards

For those looking to rebuild credit, secured credit cards can be a step towards financial rehabilitation. These require a cash deposit that serves as collateral and the credit limit. Responsible use of a secured card can help improve credit scores over time.

Check-Cashing Services

Certain retailers and dedicated check-cashing outlets will cash checks for a fee. This option can be expensive over time, but it’s a readily available service for those without a bank account.

Money Orders

Money orders can be purchased at various locations, including post offices, supermarkets, and even some banks. They are a way to pay bills or send money without needing a checking account, though there is typically a small fee involved.

Mobile Wallets

Technologies like Apple Pay, Google Wallet, and Samsung Pay enable users to make contactless payments in stores or online. Some of these services also offer ways to receive money from others, which can partially substitute for the functions of a bank account.

Cryptocurrency Accounts

For the more tech-savvy, cryptocurrencies offer an alternative financial system entirely. Some services allow users to receive wages in cryptocurrency and pay for goods and services. However, the volatile nature of cryptocurrencies and regulatory uncertainties make them a riskier option.

Conclusion

Lack of access to traditional banking can be a significant obstacle, but there are numerous alternatives available that can help individuals manage their finances. Each option comes with its own set of pros and cons, and what works best will depend on the individual’s circumstances and needs. It’s important to carefully consider the fees, limitations, and risks associated with each alternative.

For those who are determined to open a traditional bank account, it may be worthwhile to address the underlying issues that are preventing them from doing so. This could involve paying off debts, disputing errors in ChexSystems, or working to improve one’s credit score. Financial literacy programs and consultations with nonprofit financial counselors can also provide guidance and assistance in navigating the complex financial landscape.

In the end, being informed and proactive is key. While not having access to a bank account can be challenging, exploring and utilizing the variety of available alternatives can ensure that one