My wife is deathly afraid of storms. I, on the other hand, would kill love to be on the show Storm Chasers. (Does that make weird? Don’t answer that…..)

Either way, hearing that first tornado siren of the season is a frightening reminder each year that we live in the path of some pretty terrifying storms. We’ve yet to go through an actual tornado, a town close ours was hit. A few years ago our region was also hit by an “inland hurricane” that left significant damage.

Year after year, I find that I don’t think about the possibility of a natural disaster until my wife rounds up our family and we are all huddled in the basement watching the weather radar on our iPhones. Otherwise, it doesn’t often occur to me to think about preparing for the possibility of a disaster.

Table of Contents

Of course, being ready to ride out a natural disaster is about much more than having a safe zone ready in the house and stocking up on bottled water. The aftermath of a natural disaster can be financially devastating for survivors, particularly if they have not taken the time to prepare.

Here are six things you need to do to be sure that you and your family will be protected in the event of a natural disaster.

Put them on your to-do list now, so you’ll be ready if and when a big storm hits:

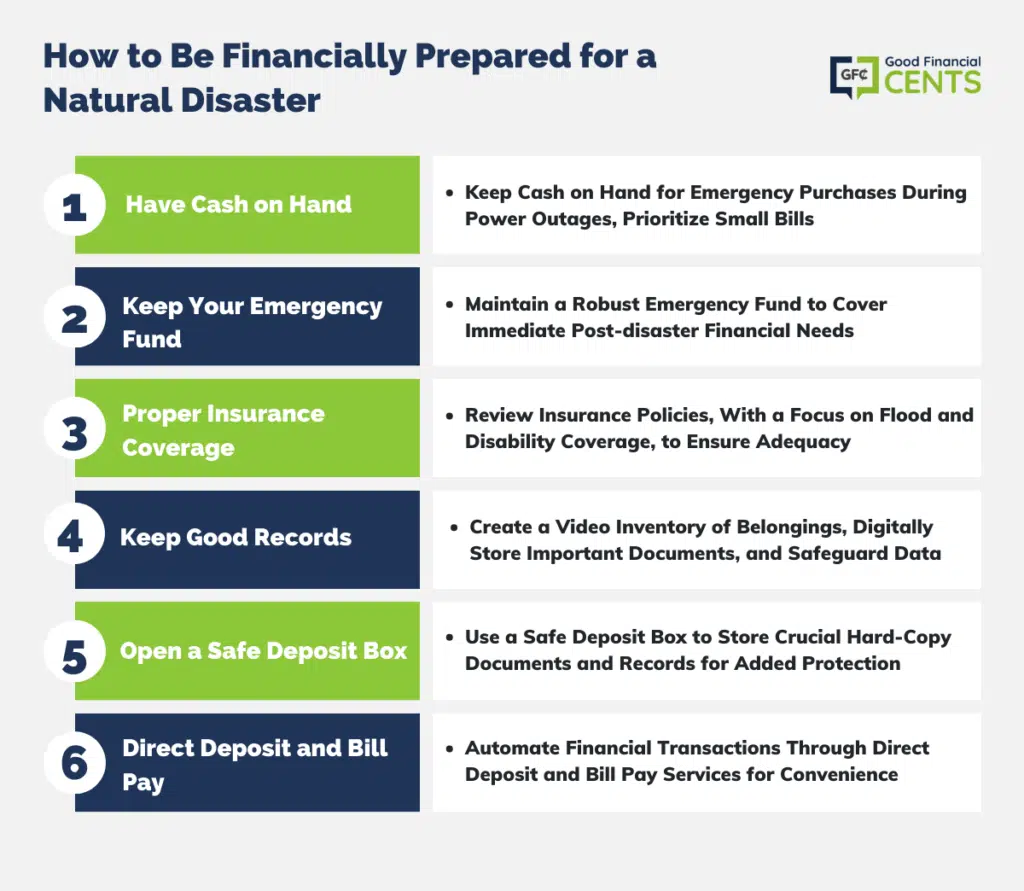

1. Have Cash on Hand

Natural disasters often take out power to entire communities, which means you’re stuck paying cash for anything you need from local merchants. It’s a good idea to have enough cash in the house to handle necessary purchases until power is restored—generally about $200-$300.

In addition, make it a point to have your cash in small bills. There’s the possibility that stores might be unable to make change easily after a disaster, and you’d hate to end up spending $20 or $50 for a carton of milk just because you don’t have anything smaller. (Although it might be difficult to explain to your wife exactly why you’re bringing home $200 in singles).

2. Keep Your Emergency Fund Robust

It’s called an emergency fund for a reason. If you have damage to your home or car or are unable to return to work immediately after a natural disaster, you will need to live on something while you are waiting for your insurance.

You can store money at your local bank, but in a big enough natural disaster that bank branch could be damaged or out of cash from everyone pulling out deposits. Using an online bank like Capital One 360 with can keep your money safe away from your local area.

3. Make Sure You Have Proper Insurance Coverage

It can be easy to assume that your homeowners’ insurance is enough to handle anything Mother Nature can throw at you. But unfortunately, your policy does not necessarily cover any and every bad thing that could happen to you or your property in the event of a disaster (or other loss). Very few homeowners could say off the top of their heads exactly what their policy covers, and policy-holders have a tendency to misremember what their coverage entitles them to. That can make for a nasty surprise when you’re in a position to file a claim.

So it’s important to go over your policy with a fine-toothed comb to determine whether you have adequate coverage. In particular, make sure you have flood insurance, as it one of the most common claims that is not covered by basic homeowners insurance.

Additionally, looking separately into disability insurance is a good idea in preparing for natural disasters—and everyday life. According to the site Disability Can Happen, just over a quarter of today’s 20-year-olds will become disabled before they retire. That’s a pretty chilling statistic, and it means any worker would probably benefit from disability coverage.

4. Keep Good Records

Having the proper insurance is not enough, however, if you are unable to provide proof to an adjuster about what you owned before a loss. It used to be that insurance companies recommended that homeowners make exhaustive lists about their property for this purpose. But, because we now live in the future, making a record of your belongings is much less of a hassle.

Simply walk around your home making a video of every valuable item that you own, using your smart phone, tablet, or other recording device. While you record your belongings, provide narration for the video by stating the brand and approximate purchase date and price for each item. This will prove invaluable for a future claim, and it will take less than 30 minutes of your time.

In addition, it’s a good idea to save that video and other important documents and records digitally, so that you can access them even if your hard copies are destroyed. Have your records scanned and email them to yourself as a simple way to make sure they are accessible anywhere but still secure.

5. Open a Safe Deposit Box

For those documents that need to be saved as hard copies, it can be easy to just leave them in your home safe and consider it good. But keeping your hard copy information in a safe deposit box at your local bank increases the likelihood that this important documentation will also survive the disaster.

Information that you should keep in your safe deposit box includes:

- Birth Certificates

- Marriage and Family Records

- Adoption Papers

- Property Deeds

- Wills

- Insurance Policies

- Passports

- Social Security Cards

- Immunization Records

- Bank Account Information

- Credit Card Account Information

- Contracts

If you’re not sure how long you should keep them, refer to our post “How Long to Keep Important Financial Documents“.

6. Take Advantage of Direct Deposit and Automatic Bill Pay

The aftermath of a natural disaster is a difficult time to remember to pay the mortgage and utility bills. With automatic banking transactions, you can focus on cleaning up rather than trying to find your checkbook or a viable internet connection in order to pay your bills.

The Bottom Line

Getting prepared for a potential natural disaster is one of those important-but-not-urgent tasks that we can often forget about for years at a time. But taking a little time now to get your financial ducks in a row long before you hear the first siren or see the first “Stormageddon!” weather forecast will definitely be time well spent.

Have you ever been through a natural disaster? Were you financially prepared?

I absolutely recommend to have a “rainy-day” fund for situations like natural disasters! You never know what might happen, and you don’t want to be left broke. I have a savings account just in case anything of the sort happens. I use SavedPlus for automatic savings, just to have money coming in regularly in case of a fire, earthquake, or just loss of a job!

Safe deposit boxes, on the other hard, are just a prone to natural disasters and banks will most likely be mobbed in the event of a serious issue. Your thoughts further?

After reading Jeff’s article I realize I have more planning to do, even though my neighborhood isn’t common for natural disasters. You never know what is going to happen in the future!

Good tips. And something it’s easy to forget to think about. The first thing I thought of when I saw your headline was your No. 1: Keep some cash in the house. That can come in very handy when the time comes.

Great list! I survived the Northridge earthquake! It had no financial consequences for me. A little planning and preparation goes a long way to resolvingg these kinds of problems.

These are good thoughts. We live in an area subject to regular mega-quakes, so these sorts of preparations are often on my mind. One I haven’t done yet is the safe deposit box. The sort of quake we’re expecting could be magnitude 9+, huge and devastating. My concern is the collapse–literally–of banks and that I may not get access to my safe deposit box for a long time, if ever. And some parts of our community–notably the downtown–are built on tailings from coal mining. Some predict this oceanside property will liquefy when The Big One hits and the ocean will reclaim the area. Again, not good for the prospects of a safe deposit box in the area. But I need to do something…

I actually did live though a natural disaster. I was without power for a week. The one thing that I wish I had was more cash on hand.

One kind of unusual way of being financially prepared is simply to own less stuff. I rent an apartment so I don’t really care if the place gets wrecked. I have an old car. I’ll be sad if it gets demolished, but it won’t be too expensive to replace. The list goes on.