“Your net worth to the world is usually determined by what remains after your bad habits are subtracted from your good ones.” -Benjamin Franklin

Have you ever tried to break a bad habit?

What about starting a good one?

Sometimes the good ones can be even tougher!

Some of the good habits that I’ve struggled with sticking to are: eating clean during the week (stupid late-night cravings), waking up at 5 a.m. to work out (the snooze button is way too tempting), and being distracted by social media (hold up, I just thought of something funny I need to Tweet).

One of the worst habits I used to have was that I would always lose my keys after I got home from work.

I’m always in a rush when I get home, and for the life of me, can never remember where I put them.

My wife, tired of me asking her, “Where did I put my keys,” attempted to break me of my bad habit by placing a small box on the countertop by our back door.

This box became the designated spot for my keys and my wedding ring.

Did I mention that I often misplace that, too? Shhhh….don’t tell the wife about that one. 😉

Some days I did well and placed them in the box. Other days I didn’t, and she was quick to remind me where to put them (thank you, Baba!). Over time, it worked.

Essentially, my wife created a system for me to break my bad habit.

When I followed the system, everything worked and I always knew where to find my keys.

When I didn’t, every morning sucked as I was trying to find my keys while scrambling to get our kids ready and out the door. Without the system I was a wreck. (Feel free to call me pathetic here. I’m used to it.)

What’s Your Bad Financial Habit?

Misplacing your keys doesn’t hurt you too much other than time and plenty of frustration. Unfortunately, bad financial habits can ruin you.

Always ordering an appetizer when you eat out (when you can’t afford it), paying unnecessary late fees on your credit card bill (because you procrastinate), not knowing your credit score, which can cost you thousands on loans and insurance rates (because you’re too passive).

These are just a handful of bad habits that many possess. Are you one of them? Don’t worry, I might have the solution for you. Read on….

How to Break a Bad Habit

The founder of my coaching program, The Strategic Coach, Dan Sullivan, developed the concept of the 21-Day Positive Focus.

In his experience working with successful entrepreneurs over the years, he discovered the most common reason for their success was the fact that they all possessed many positive habits. These positive habits didn’t just happen overnight.

Similar to the system that my wife created for me with the keys, these entrepreneurs worked to develop these tasks until they became part of their ordinary routine.

Sullivan went on to create the 21-Day Positive Focus as a way to celebrate each day that you achieve a positive habit. By taking time each day to focus on that positive achievement, you’ll become more confident in that habit. Sullivan says,

“You’ll have the energy and motivation to do more, and you’ll find yourself enjoying the results of your efforts more, too.”

Sullivan’s findings were also echoed in Charle’s Dughigg’s New York Times Best Selling Book The Power of Habit.

Once you understand that habits can change,” Dughigg concludes, “you have the freedom — and the responsibility — to remake them.

My favorite example in Duhigg’s book was how Tony Dungy trained his players to make basic moves that they would practice over and over again.

He believed that by practicing these skills, his players would just react, not think, and have an edge on their opponent. He trained them to have winning habits, which finally came to fruition when his team won Super Bowl XLI.

Table of Contents

Readers Share Their Habit Experiences

A while back, I took a poll of my readers to learn some of their bad habits that they are currently struggling with or others they have been able to overcome. Here’s what some of them shared:

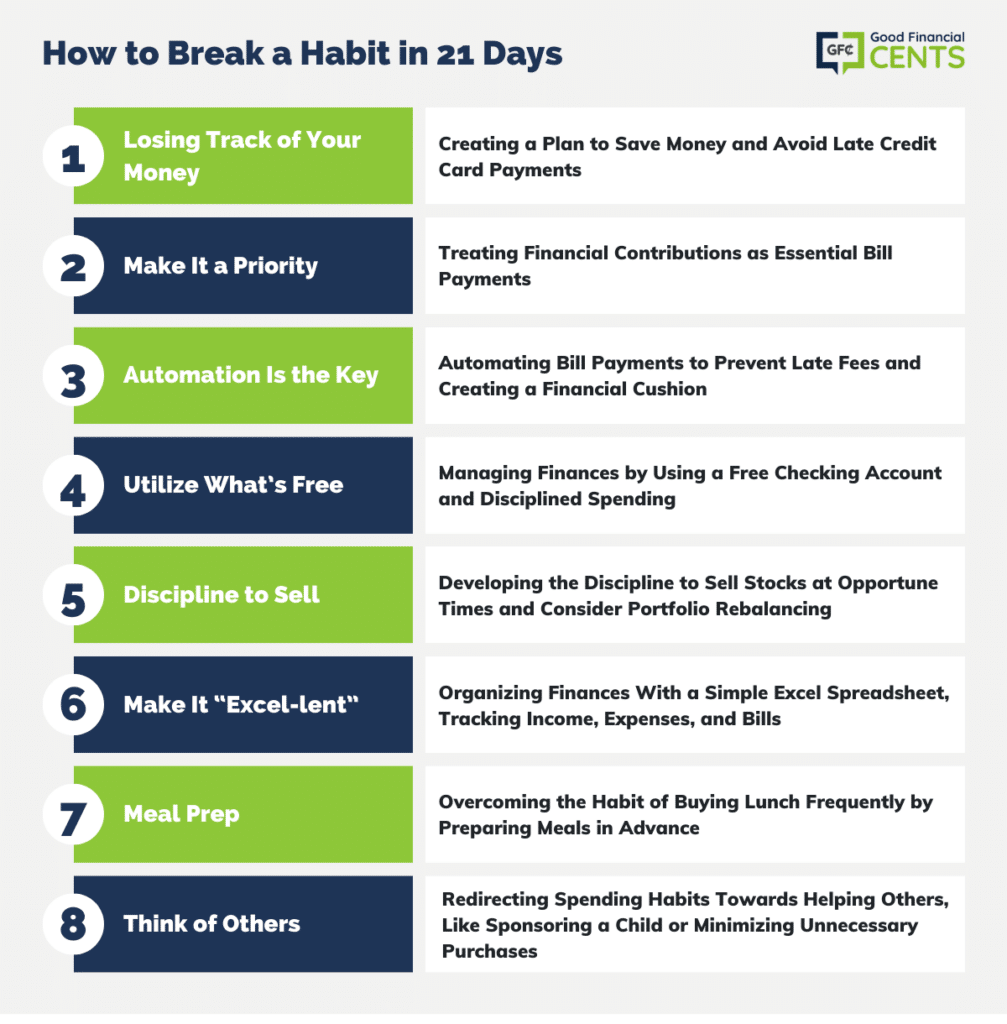

Habit #1: Losing Track of Your Money

This amount of money was never accounted for; it was like ghost money. We put a plan into action and have been saving every month way more than $300.00. To break the bad habit of paying credit card bills late, I did two things:

- Set up automatic payments online. So that if I goof up and pay late, at least I don’t have $29 in late/penalty fees in addition to the interest.

- Check all my credit card and bank accounts online every few days. I keep track of all new transactions on Quicken, so I know if any bank accounts are approaching zero and can see within a couple of days any new credit card statements that have been generated.

When I see a new credit card statement, I schedule a payment online for a day before the due date. This way, I keep my money in an interest-bearing account almost as long as possible, but if I ever do need to beg for mercy from a credit card company, I can say, But I usually pay EARLY!

Habit #2: Make It a Priority

Our Roth and 529 contributions are treated like bill payments. They are scheduled to automatically be sent every month out of our checking account.

Habit #3: Automation Is the Key

I’ve got a couple, but the best one was automating all of my bills to stop late payments and reconnect fees. I also have a $500 ‘cushion’ in my checking that was not added to the register to cover in case one of those automated bills hits before I deposit my check.

Habit #4: Utilize What’s Free

Open a free, no minimum balance checking account with a debit card and automatically transfer your agreed-upon and BUDGETED “allowance” into the account each week.

When the money’s gone, wait until next week. I have done this for myself and my wife for about 15 years, and it eliminates so much stress and strife that it becomes a habit.

With online banking, the charges show up almost instantly, but after a few months, you can almost keep track in your head.

Using a debit card requires discipline, unlike a credit card which is always a budget buster. I believe in keeping a minimal buffer of funds in a debit card account, so I spend my small allowance down.

On the other hand, my wife, who gets a little more (for groceries, etc.), likes to see how much she can accumulate, so there’s a challenge for everyone.

One reason we get the FREE accounts and FREE online banking is because we have other accounts at the bank that meet their overall balance requirements. I hope this benefit doesn’t disappear.Note: Here’s our recap of the best online banks to maximize your savings.

Habit #5: Discipline to Sell

I have a difficult time allowing myself to sell a stock once I have made a good gain. I seem to fear that the stock has made a good run, but it could go higher, and by selling, I will miss the additional gain.

Usually, after a nice run-up in price, I hold the stock too long, and then it has a pullback, and I sell in somewhat of a panic, thinking it will continue to go down in value.

Consequently, I have made a gain, but a lesser one than if I had sold earlier. I don’t have the discipline to set a selling point, and once I reach that target, I take money off the table. Bad habit. Lack of discipline.

One bad habit that I “would like” to break and know I should is: REBALANCE the portfolio periodically rather than just riding out the market. I still have not broken the habit since it takes time and effort to do this periodically. In addition, when is the right time?

At this time, bonds are not up or down but seem to be following the market instead of being inverse. This makes it seem that rebalancing will not accomplish anything.

Habit #6: Make It “Excel-lent”

My husband and I use an Excel spreadsheet that is very simple. The left column lists income streams and the bills that we regularly pay, separated by the 1st and 15th of the month paydays across the top, which we list each month.

We also list non-regular expenses such as taxes, vacations, gifts, etc. Estimates and budget amounts are entered in blue font and changed to black when the actual is entered and the bill is paid. The expenses are subtracted from the income, telling us if we “have more money than last month.”

We are then able to tell right away whether or not we will have money available to take a weekend trip or attend a concert.

The added benefit to us is that either one of us knows what is due, so we aren’t paying the same bill twice, and we know if a bill has been missed, so we can get it paid before we incur any late fees.

Having the whole year’s payments on one sheet makes it easy to pull tax information together and look at areas for improvement in spending. We use our bank’s online bill pay so we don’t have to bother writing checks or finding stamps.

Habit #7: Meal Prep

My bad financial habit was buying lunch multiple times a week instead of bringing it to work. What worked best for me to break that habit was to get into a routine of prepping the night before (I am not a morning person).

When cleaning up the kitchen after dinner, I pack the leftovers into serving-size containers.

That makes it easy to grab lunch in the morning, and there are no excuses because it’s already there. I’m the type that prefers a hot (reheated in the microwave) lunch over a sandwich, but in an emergency, I can always fall back on PB&J and an apple.

Not wanting to eat PB&J motivates me to make sure I have something I like for lunch.

So now, instead of buying lunch a few times a week, I now buy lunch a few times a year. I’m kind of proud of that. 🙂 Of course, the step before “packing up the leftovers” was to break my bad habit of not cooking dinner (because if you don’t cook dinner, there are no leftovers).

I am still a work in progress on this one, but the best indicator of whether I will be successful at cooking dinner most nights in a week is if I sit down on the weekend, make a menu plan and shopping list for the week, and then go grocery shopping.

I know that’s basic, but when you’re a working mom with three busy children, some weeks it’s harder to be disciplined about that than others.

When I’m not disciplined enough to make a real dinner, we fall back on what I consider “homemade fast food,” like tacos, spaghetti, or a ready-made roast chicken from Costco. It’s better than eating out, but it can get boring.

If we cheat and eat out or pick up something for dinner, at the very least, I try to make sure to get something that makes good lunch leftovers. The bonus is that I don’t overeat.

My family always teases me that a restaurant dinner entree for me equals food for two more days!

The bottom line is that a little extra time and conscious effort to prep — a few minutes at night (making lunch and also putting into the fridge what needs to be defrosted for tomorrow night’s dinner) and a couple of hours on the weekend (making a menu/list and going grocery shopping) — makes all the difference in our eating and therefore our financial habits.

Habit #8: Think of Others

Perfume/Lotion: I broke my habit of buying expensive lotion and perfume after reading “The Ultimate Cheapskate’s Road Map to True Riches” by Jeff Yeager. Page 97 explains how we could feed the world’s hungry if we put the money we spend on perfume towards helping people who are starving.

This just weighed so heavily on my heart that every time I reach for some expensive cream or some perfume, I stop and think of a starving child.

I started sponsoring a child in Honduras, which costs me $60 a month. That’s money well spent, and it prevents me from buying more crap as I’m buying unnecessary lotions, etc.

Children’s Toys/Books/Clothes: This has carried over to other spending; we don’t buy toys and books for our child because she has so many that other people buy for her.

We use Thredup.com, a site where you can send out your children’s old clothes to parents who need them, and you can order boxes for your kids.

You only pay for the shipping; it’s like a big hand-me-down network. We don’t even have clothing as a line item in our budget; we purchase it so rarely.

School: I’m also going to school at night, and all my textbooks I buy used if I can, and as soon as the semester is over, I post them online to sell them again. DVDs: My husband used to buy DVDs of all the movies he liked. We never really watch them.

When I see him hunting for a new release, I remind him that we usually watch it once before it sits there collecting dust. ***** Thanks to everyone who shared their habit stories! Now it’s your turn…

Have a bad habit that you’ve been trying to break? What about a good habit that was part of your New Year’s resolution that lasted only two weeks? Yeah, I’m looking at you.

I want you to either stop a bad habit or start a good one that you’ve wanted to do for a long time. Are you in? How about some financial incentives? Now do I have your attention? 🙂 Challengers will have a chance to win:

- 1 $50 Amazon Gift Card (chosen by me for the best habit conquered)

- 2 $25 Amazon Gift Cards chosen by random submission

- 2 copies of my book, Soldier of Finance, chosen by random submission

Rules of the Challenge: You can choose any habit that you want to break or start. It does not have to be financially related.

- Want to work out for 20 minutes a day? Great!

- Want to make time to read your Bible before the kids get up? Fantastic!

- Want to do 100 pushups every single day while you’re at the office? Welcome to the club. 🙂

I don’t care what the habit is as long as it goes towards making you a better person.

Here are the specific rules:

- Leave a comment announcing you’ve joined the Breaking Bad Habit Challenge and what your target habit is.

- Download The Bad Habit Destroyer worksheet (pictured above). This is part of the Money Dominating Toolkit that is exclusive to the GFC community.

[get-toolkit-shortcode] How Long Does the Contest Run? I’m running the contest until the end of the year (Dec 31, 2013). Winners will be contacted by me directly and shared via the blog in January 2014. Any way else I can help promote the contest? Why I’m glad you asked. 🙂

First off, share this post on your social media channels (Twitter, Facebook, Pinterest, Instagram, Google+, etc.). For your convenience, I’ve already prepared this Tweet to spread the word. Just click the link to share.

Lastly, print off The Bad Habit Destroyer and write down the habit you want to focus on. Take a picture and tag me on Facebook or Instagram. Let’s help others conquer their habit goals too!

“We are what we repeatedly do. Excellence, then, is not an act, but a habit.” -Aristotle

Final Thoughts – How to Break a Bad Habit in 21 Days

The journey to break bad habits and embrace positive change is not just a matter of willpower but of strategic planning and consistent effort. Benjamin Franklin’s insight holds true: our true potential emerges when we subtract detrimental habits from our lives.

The 21-Day Positive Focus, as espoused by successful entrepreneurs, underscores the significance of incremental progress. Similarly, Charles Duhigg’s “The Power of Habit” reinforces the malleability of our habits and the freedom to reshape them.

Ultimately, these shared experiences highlight the profound impact that intentional habits can have on financial well-being and personal growth.

I used to be a big spender. I was overweight, and, in order to mask up my excess weight, I used to buy tons of expensive clothes and perfumes to cheer myself up. I also used to eat lunch outside every day, which added up to the excess weight I didn’t seem to lose. Then suddenly, a financial shake up made me live with $ 1000 less a month, which made me change my habits suddenly. I started to pack lunch to work and as I couldn’t afford ready made meals and processed food, I bought fruits and vegetables, which not only were cheaper, but also healthier. This allowed me to lose over 5 dress sizes, and I m now slimmer and fitter. I also stopped buying expensive clothes, as my weight loss forced me to give all my clothes to charity. The financial loss turned out to be a victory for me, as I learned to live frugally and healthily, and surprisingly enough, I even managed to save up money for a 5 star holiday which I couldn’t do when I was earning more money and overspending! I really like the advices given in this article, such as going vegetarian twice a week, and stop spending a lot of money on expensive perfumes and lotions, as this is what I di for the past few years, and which lead me to nothing but losses! This article gave me more confidence about myself, and no regrets about living a frugal life!

I believe in breaking any kind of habit in 3 weeks or 21 days. I like to take that approach to all things in life, health related as well.

Had a snag getting sick and traveling with my habits but have finally accomplished them late!

Hey! A bit late to the game but there are still 21 days before the 31st. I want to break the habit of pushing the snooze button when my alarm goes off in the morning. That means waking up right at 5 during the week and 7 or 8 on the weekends. When this happens I can read the Bible right away too. Thanks for the challenge!

They go on to point out that the key to fixing the bad habit in this case isn’t in giving up entirely on the socialization and the relaxation—if you do that, you’ll just make yourself unhappy and alienate yourself from your coworkers, and therefore more likely to slide back into your old habits. They suggest instead trying to get one of the coworkers you go drinking with to do something else—running, yoga, rock climbing, anything—that gives you the same rewards and is triggered by the same cue. Whatever you do, the key to success is to fix the routine without breaking the other elements of the loop.

I have a habit of taking EVERYTHING seriously, I want to break this and lighten up… perhaps not to take everything literally. A lifetime habit will be broken in 21 days!

I want to break the habit of not being an effective listener. I often overtalk or cut ppl off. That is a habit I need to break.

@ Chaz I sometime struggle with this, too. I sometimes have to mentally take a breath before I let myself talk.

The other thing I’ve realized is that the more you let other people talk, the more they like you and think you genuinely care. Why? Because you take time to listen.

Good luck and be sure to use the worksheet on this one. It will be a good daily reminder to help you out.

Joining in on the challenge!

I’ve got to lose some weight before traveling to the Midwest to see family this Christmas. (Yeah, I’m one of those people – I’ve got to look good!). So, this is excellent motivation to keep me focused!

I’m going to break my “sweet tooth” habit and eat cleaner, also plan to exercise 45 mins – 1 hr. a day.

Thanks!!

Good luck Christina! Saw the pic on Instagram. 🙂

I’m in! Just got back to work after maternity leave today. Won’t see my kids until early evening…so no social media/messaging/blogging until all kids are in bed!

I did kind of start today, but will make it official tomorrow…

Am picking a financial challenge also because I started work today – no buying lunch, I have to pack one every SINGLE day (for 21 days at least).

Thanks for the challenge Jeff Rose!

You are welcome Alyson!

I’m in Jeff! I usually like to do everything at the same time, but I’m going to stick with 2.

1. Exercise every day for at least 30 minutes

2. Bible study and/or devotion every night

I feel like these 2 things are going to put me in a much better mindset, especially going into 2014.

I want to break the bad habit of me pulling my eyelashes, and give up on soda, but I’m not ready yet haha.

I’m in on this challenge! My two-year-old daughter has several food allergies; dairy, eggs, soy, and (the scary one) peanuts. I am committing to adopting her restricted diet for myself. We already make most family meals to compensate for her so she doesn’t feel left out. But, I’ve decided to be strict about it. No more sneaking in cheese, or butter, or any processed foods! (they all contain soy) Hopefully this will help me to better support her and improve my health as a bonus!

I have joined the The Breaking Bad Habit Challenge, and I will bring my coffee and lunch to work with me every day, and I will be sure to set up the coffee and make my sandwich the night before.

I’m in. We just had our third daughter two days ago, and I’ve already got a 5 1/2 year old and a 3 1/2 year old. My goal for the next 21 days is to spend 10 minutes during the day with each child individually. (one on one time) reading, playing my little pony, coloring… whatever they want to do. .

I’m hoping to have a better relationship with them and ease the shock of new baby for my other two.

I’m going to get straight out of bed in the mornings with absolutely no snoozing! Harder than it seems for the likes of me. 🙂

I am joining this challenge too! I am committing to do two things over the next 21 days:

1. Workout for 30 minutes a day either by myself (or preferably with others).

2. Do a devotional each day with my son.

I’m in! My goal is to work out at least 30 minutes every day.

You can do it Janet!

I am joining the challenge! I get incredibly frustrated by how messy our house “always” seems to be! My goal is to keep the house “company ready” all the time – picking up after I finish a project, compiling an actual cleaning schedule, and putting things where they belong when I get home sound like good places to start!

Woo-hoo Jessica! That sounds exactly like my wife. She’s always picking up after the boys and I. 🙂

I’m all about this! No more sugar for this mama.

I’m going to stop making excuses, and doubting myself. I’m going to blog 5 days a week.

Thank you for doing this. I really needed this push.

@ Tawny Be sure to use the checklist. I promise you that crossing it off each day will help. https://www.goodfinancialcents.com/bad-habit-worksheet

Jeff! Love this challenge so much!

I’m going to attempt to break two bad habits by replacing them with positive things.

1.) No negative thoughts. My brain tends to immediately jump to the worst case scenario. Instead, when the dark clouds start to creep in I’m going to make sure I STOP..and immediately replace those with a few positive thoughts to turn around the process. This IS a daily struggle of mine.

2.) Put my phone down when it’s bedtime for my son. That is a special time for us to bond and I admit most night’s I try and speed it up so I can have a break. No more of that. Time goes by way too fast. I vow to savor these moments 🙂

I intend to leave all but one credit card at home. It is part of a strategy to plan my usage better. the one card I plan to usually bring is my ‘food’ card.

Great tips all around especially on how to manage one’s finances. I especially like the #1 -4 but based on experience it can be bit frustrating to teach this to a technologically-challenged person, like my parents. 😀

I’m in! I’ve been needing this so desperately! I’m going to follow your lead and read my Bible 10 minutes a day. I’m also going to focus on not biting my nails. That’s a lifelong bad habit.

So…I made another goal…but I want to be intentional about praying over someone (preferably someone I don’t know well) each day, then being intentional to encourage one person each day who I know is struggling.

@ Lauren What a great goal! Even if you don’t pray for someone (like hands on prayer) I think intentionally praying for someone each day is great.

It’s funny you mention this because I was released to pray over people at our church for our hands on prayer ministry team for at least 6 weeks now. Up until today, I haven’t prayed over anyone yet. Not that was scared (maybe kinda) but there wasn’t really the opportunity.

Well finally today I got that chance! I prayed over a young man who has been struggling to sleep through the night. I’m really hoping that tonight is his best night’s sleep in a while. 🙂

Anyway, had to share because of your goal. 🙂

I am committing to 15 min of bible reading per day.

Awesome Brenda! We’ll do this together. 🙂

I’m joining the challenge! I would love to develop the good habit of tracking my spending. I want to know where my money goes… I am probably not going to like what I see but that might be the kick I need!

@ Meredith Great! This post offers some free tools that might help you out. https://www.goodfinancialcents.com/best-free-online-budgeting-tools/

Good luck!

Hey there! I’m joining in, and going to get in the Word every day. First thing, no excuses! I know from experience it makes me whole day a lot better, but always get lazy after a while. No more!

@ Lauren I agree…no more excuses. For us both!

I will take on a dual challenge 1) do 25 sit-ups a day 2) pay my bills as soon as I get paid instead of putting it off and feeling defeated! Time to conquer!

Sounds great, Vicki! Try and do the sit-ups 1st thing in the morning. You’ll feel that much more confident the rest of the day.

Up for the challenge! Endeavoring to start my day with Bible reading first thing!

@ Sybil Welcome to the challenge!

I am starting the 21 day challenge tomorrow which is perfect since every good goal must start on a Monday 🙂 I am aiming to accomplish 2 good habits! Working out everyday and reading before bed instead of watching tv! Thanks for the motivation Jeff! You and Mandy are both awesome!

@ Cricket Good luck on the challenge. So glad to have you on board. 🙂

Hi, I just joined after reading about the challenge! I plan on eliminating eating out and start up a work out routine again. Get rid of one bad habit and start up a new one. Wish me luck!

What better time to stop smoking once and for all? Thanks for the inspiration Jeff.

@ Greg I’m holding you to it!

Great advice, Jeff! And LOVE the Aristotle quote, it’s also one of Mark’s favorites. 🙂

The ending of your video made me chuckle!

Thanks Malori! Had fun filming that video. 🙂

NO MORE SODA! Goodbye Coke, I’ll miss you!!

@ Kelly I was trying to get my wife to do the same thing, but she responded with “Do you really want to be around me without at least one fountain coke a day? Didn’t think so.”

We agreed that she would work on another habit. 🙂

The obvious point here is to get rid of any items whose sole purpose will be to tempt you away from your best intentions. (As in, bring any remaining Halloween treats to work the morning after, or just be really generous in the last part of the evening. Better yet, give out something that doesn’t lead anyone else down that Pied Piper path to begin with – more help on that this week.) If your triggers are less object-oriented and more contextual, toss the typical routines that encourage bad habits. Meet friends for a walk in the park instead of for dinner. Take up a fitness or dance class with your partner instead of spending Friday nights parked on the couch. Put the kids in charge of their own morning routine and get in a workout or meditation session instead. Taking on a long-held habit usually means taking charge of your life in a new way.

Another nail biter here too! Bad habit since I was a child, and it’s really embarrassing. Good luck to all those participating!

I am joining the challenge. I am going to focus on my bad habit of nail biting. Seriously. I gnawed on them the entire time I was reading this. This habit has to stop. So, 21 days… here we go!

@ Tiffany Woop woop! Welcome to the challenge. 🙂