Your credit score can have a dramatic impact on your life, and that’s true regardless of your age, your gender, and where you live. After all, a good credit score can make it possible to purchase a home or finance a car so you can get to work.

Bad credit or poor credit, on the other hand, can make it difficult to qualify for a loan you truly need, especially not one with the best rates and terms.

This is part of the reason it’s smart to care about your credit early on — well before you need it. If you’re hoping to build credit now so you can live the life you want when you’re ready, read on to learn how credit scores work and the best ways to build credit that lasts.

Key Takeaways

- Your credit score can impact your ability to buy a house, finance a car, or take out a personal loan.

- The most common credit score is the FICO score. This type of score is used by 90% of top lenders.

- There are five main factors that make up your FICO score — your payment history, the amounts you owe, the length of your credit history, new credit, and your credit mix.

- Building credit from scratch can be a challenge, yet there are several credit-building financial products that can help.

Table of Contents

How Credit Scores Work

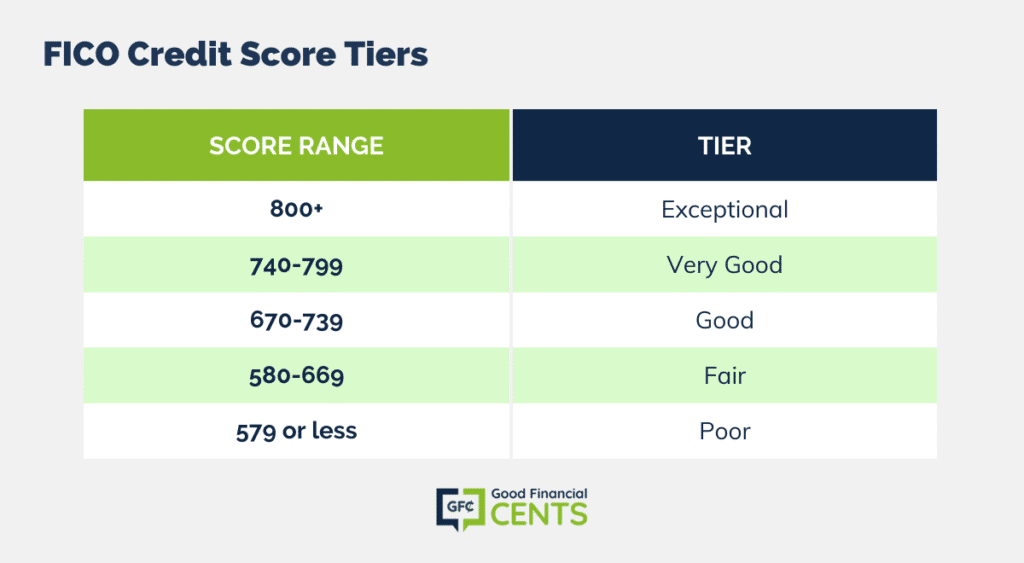

Before you learn how to build your credit score, you should have a basic understanding of how credit scores are determined in the first place. When it comes to FICO scores, you should first note the fact that your score can fall between 300 and 850, with higher scores showing better credit health.

Within that broad range, there are different tiers of scores to strive for. With the FICO scoring method, credit score ranges are as follows:

According to USA Today, the average VantageScore (another type of credit score that works similarly to the FICO score) is currently at 702, which is up from the average score of 697 reported in 2022.

Regardless, it’s best to shoot for a score of 670 or higher, mostly because this is the threshold where lenders believe you have a good credit score.

Knowing credit score ranges can help you find a goal to shoot for, but you also need to know the factors that come into play. The FICO scoring method considers five different factors when determining your score:

- Payment history (35%): This factor looks at how often you pay your bills early or on time, as well as whether you have any late payments.

- Amounts owed (30%): This factor looks at how much debt you owe in relation to your credit limits.

- Length of your credit history (15%): This factor looks at the average length of all your credit accounts combined.

- New credit (10%): This factor considers how many newer hard inquiries and credit accounts you have.

- Credit mix (10%): Your credit mix considers the types of credit you have, including revolving credit, installment credit, and more.

6 Ways to Build Credit Fast

If you want to know how to build your credit score, taking a look at the factors we outlined above can help. However, there are some specific steps you can take to build your credit score fast, including the following:

Get a Secured Credit Card

Building credit can be a challenge when you have none, mostly because it’s difficult to get approved for any type of credit card or loan. However, secured credit cards help you sidestep that issue altogether — that is if you’re willing to put down collateral.

With a secured credit card, consumers typically put down a cash deposit of $49 to $200 or more. This collateral secures their line of credit, which gives them a small amount of purchasing power.

Many secured credit cards don’t require an annual fee, and some even let you earn rewards. Also, note that the cash deposit you put down is fully refundable when you close your account or upgrade your card in good standing.

The most important benefit of secured credit cards is the fact they report to the three credit bureaus — Experian, Equifax, and TransUnion.

This means that, as you use a secured credit card for small purchases and pay your bill on time, your secured credit card can add depth to your credit history and boost your credit score.

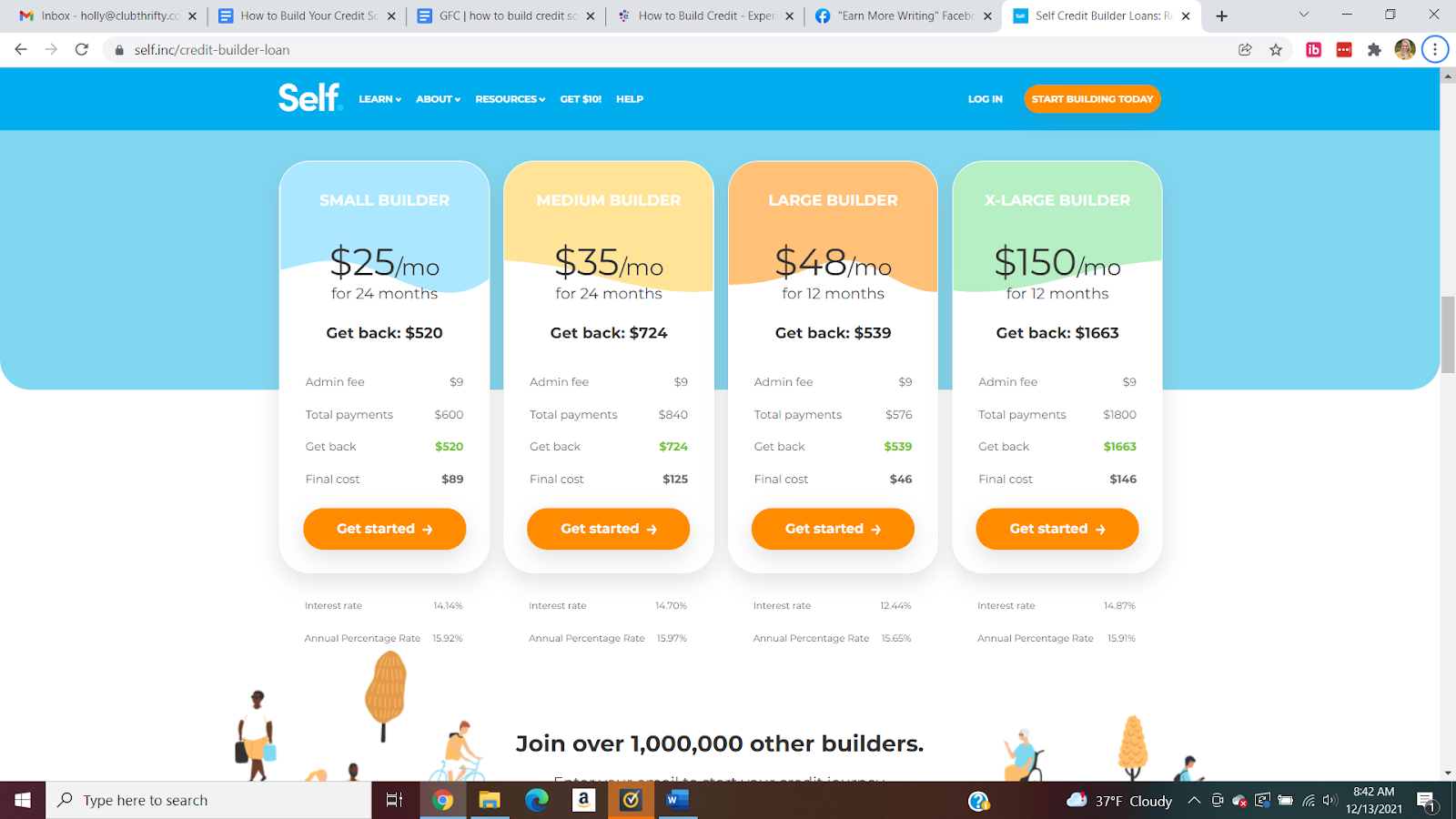

Apply for a Credit Builder Loan

Another option for building credit involves applying for a credit builder loan. With this type of loan from Self, for example, consumers take out a “loan” of sorts that allows them to make payments to a savings account.

While a small amount in fees and interest is charged along the way, the loan user gets the money they pay toward the loan back in the end. More importantly, the payments they make are reported to the credit bureaus, giving them the chance to build their credit score quickly.

While credit builder loans aren’t free by any means, they don’t have to be costly, either. As you can see from the screenshot below, a credit builder loan from Self can cost as little as $48 over 12 months.

Try Credit-Building Apps

Also consider a handful of free apps that can help you build credit without much work on your part, and without taking out any type of loan. With Experian Boost, for example, consumers can download the app and start getting credit for streaming services they pay for, utility bills, and more.

Experian Boost is entirely free, and you can even get a free look at your FICO® Score 8 just by downloading the app. However, it’s worth noting that you need six months of credit history to get a FICO credit score and to better assess your creditworthiness over time.

Look Over Your Credit Reports

Another step you can take to build credit involves making sure you don’t have any glaring mistakes on your credit reports. After all, incorrect reporting on your credit reports can adversely affect your score, yet you won’t know you have any problems unless you take the time to look your reports over.

Fortunately, the website AnnualCreditReport.com lets users look at the credit reports from the three credit bureaus — Experian, Equifax, and TransUnion — for free.

While you could only see each of your reports once every 12 months in the past through this site, you can now check your credit reports up to once per week for free due to the COVID-19 pandemic.

Once you download all three of your credit reports, make sure to look them over for incorrect reporting, such as false late payments or incorrect balances owed. If you find any problems or incorrect information, you should dispute credit report errors and have them removed.

Become an Authorized User

Becoming an authorized user of another person’s credit card can also help build credit fast. When you’re an authorized user, payments made to the primary cardholder’s account can help add depth to your credit reports, thus boosting your score.

However, it’s worth noting that the opposite is also true and that a primary cardholder who pays their bills late has the potential to damage your credit score. This is why, at the end of the day, you should only become an authorized user alongside someone you trust and vice versa.

Use Credit Responsibly

Whether you apply for a secured credit card, take out a credit builder loan, or use the available credit you already have as a means to build your credit score, there are plenty of steps that can help you prove your creditworthiness to potential lenders.

The most important credit-building moves include the following:

- Pay all your bills early or on time. Since the most important factor that makes up your FICO score is your payment history, paying bills early or on time is the best move you can make.

If you’re worried you’ll accidentally miss a bill, take steps to make sure you don’t forget, such as setting calendar reminders or setting your bills up on autopsy.

- Keep your credit utilization on the low side. Maxing out your credit cards is a surefire way to make sure you look risky to potential lenders. Generally speaking, you should strive to keep the amounts you owe — also called your credit utilization — below 30% of your available limits.

If possible, keeping your utilization below 10% is even better.

- Don’t open too many new accounts. Since new credit also plays a role in determining your FICO score, you should strive to avoid opening new accounts you don’t actually need.

At the very least, try to space out new account applications by several months if you can.

- Keep old accounts open. Also, avoid closing older accounts you have if they’re in good standing. Keeping old accounts open can help increase the average length of your credit history — even if you’re not using them.

- Monitor your credit score. Finally, it can help to keep an eye on your credit score as you build it over time. By monitoring your progress, you can see how you’re doing and find out quickly if something has gone wrong.

Difference Between Building Credit and Fixing Credit

The steps we outline above are good ones regardless of where you are in your credit-building journey, but it’s still important to understand the difference between building credit and fixing credit mistakes you have made in the past.

In the former scenario when you have no credit to speak of, your main focus should be qualifying for some basic lines of credit (credit builder loans, secured credit cards, etc.) in order to start building a credit history.

In the latter scenario, however, additional steps may need to be taken to get your credit where it needs to be.

For example, let’s say you have credit accounts in default. In this case, the steps above won’t necessarily help your situation until you get your defaulted accounts in good standing.

If you’re trying to fix credit, your next best move typically involves making payments on old accounts in default and working to pay them off.

Of course, you can also turn to a credit repair agency like Credit Saint for help. Not only can a credit repair agency serve as your advocate, but they can help negotiate with creditors to lower your interest rates or secure better repayment terms.

Credit Saint and other similar companies also work to identify problematic items on your credit reports so they can get those items resolved.

The Bottom Line

Building credit takes time and patience, but it also requires a certain amount of credit-building skills and knowledge. Fortunately, the process isn’t that complicated, and there are credit-building products geared specifically toward people who need to build credit or repair credit mistakes from the past.

If you need to start building credit, you know now exactly which steps to take next. The sooner you get started, the sooner you’ll have a credit score you can be proud of.