If you owe more than a few thousand dollars, especially on high-interest credit cards, you’ve probably considered debt consolidation. But exactly what is debt consolidation, and how does it work? More specifically, when does it make sense, and when is it the wrong strategy?

Let’s drill down into the basics of debt consolidation to help you decide when it’s the right move, and when it holds the potential to only make your situation worse.

Table of Contents

Debt Consolidation Guide

What Is Debt Consolidation?

Debt consolidation is a financing arrangement with the goal of wrapping two or more loans or credit lines into a new, single loan. It’s one of the best strategies to consider if you’re contemplating how to get out of debt. For many individuals and couples, it’s the first step toward debt freedom.

But what’s critical to understand with debt consolidation is that it doesn’t reduce the amount of debt you owe. It simply repackages it into a single, more manageable debt.

That alone can be an excellent strategy to get out of debt. Many debtors find it easier to manage a single monthly payment on one loan than to juggle multiple payments on several obligations.

But in a classic debt consolidation scenario, you’re not only consolidating multiple debts under a single loan, you’re also working to reduce your monthly payment. That will be possible if you’re able to obtain a loan that has a lower interest rate than the debts you’re consolidating.

The problem with credit cards is their revolving nature. Even as you make payments on your credit cards, the balance never seems to go down. That owes to a combination of very high-interest rates – often over 20% – as well as continued use of the card for new purchases.

With a fixed-term debt consolidation loan, you may be able to pay off all your outstanding debt in no more than three or five years. By contrast, credit cards tend to become permanent debt. Debt consolidation is a way to put a stop to that.

How Does Debt Consolidation Work?

Let’s say you have outstanding balances on five credit cards. The five cards together have a combined balance of $20,000, with an average interest rate of 24%.

Your monthly payment is about $500, or 2.5% of the outstanding balance. But $400 of that is interest! That means only $100 per month is going toward principal reduction. At that rate, it will take you at least a dozen years to pay off your credit cards, if it ever happens.

You have an opportunity to do debt consolidation. The loan is for $20,000, which will enable you to pay off all five cards. The term is five years at an interest rate of 8%. That’ll give you a monthly payment of $405.53.

By taking the debt consolidation, you’ll not only save almost $95 per month on your monthly payment, but you’ll also chop years off the payoff of the credit cards. Just the peace of mind that comes from knowing you’ll be debt-free in five years will justify debt consolidation.

But you’ll also save a fortune in interest. The monthly interest charge on the debt consolidation loan will be $133.33. That’s just one-third of the amount of interest you’re currently paying on your credit cards!

The best way to do debt consolidation is by using a personal loan. By taking advantage of the best personal loans you may be able to get a high enough loan amount to pay off all your debt and at a much lower interest rate. To do that, you’ll need to thoroughly understand how to get a personal loan approved. Many personal loans are now available from online sources, so you’ll need to know exactly how the application process works.

What Are the Pros/Cons of Debt Consolidation?

Pros

Cons

Some debtors have been known to do serial debt consolidations, rolling one consolidation loan into an ever-larger one.

Debt Consolidation and Your Credit

One of the unexpected benefits of debt consolidation is that it can improve your credit. Many borrowers have experienced an almost immediate 20 to 30-point upward bounce in their credit scores after doing a consolidation.

The reason for this score improvement is the way credit scores are calculated.

Two important factors in the calculation are 1) the number of accounts with outstanding balances, and 2) revolving credit vs. installment debt.

By doing a debt consolidation and paying off several credit cards, you’ll be reducing multiple credit lines down to one debt. That alone is worth a few points on your credit score. But you’ll pick up a few more points because you’ll be moving from revolving debt to installment debt. The credit bureaus prefer installment debt, because of its greater predictability, especially with regard to interest rates.

But that’s only the beginning. As you make regular, on-time payments on the debt consolidation, your credit score will continue to rise.

In fact, debt consolidation can be an important step in how to build your credit score, especially if your score needs improvement.

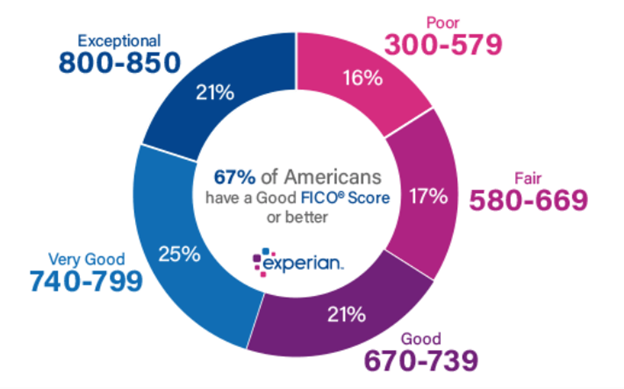

As you can see, good credit starts at 670. If your score is lower, you may need to consider working with one of the best credit repair services to bring your score up to where it needs to be.

When to Seek Out Debt Consolidation

A debt consolidation loan is never something that should be done automatically. You’ll first need to fully consider your financial situation, then ask yourself the question: should I do debt consolidation?

A debt consolidation loan makes sense if any of the following apply:

1. Your income and credit score are high enough that you can get a large enough loan to pay off all your debts.

2. Your credit score is high enough to give you the benefit of a lower interest rate than you’re currently paying on your debts.

3. The monthly payment on the debt consolidation loan will be lower than the combined payments on your current debts.

4. You have a budget in place and you’re able to live within your means.

5. You’re fully committed to the idea of getting out of debt. You’re prepared to avoid new debt once the debt consolidation loan is in place.

A debt consolidation loan may not make sense if any of the following apply:

1. You’re unable to get a debt consolidation loan for enough money to pay off all your debts.

2. Your credit score is fair or poor, and there’ll be no savings on the interest rate.

3. The monthly payment on the debt consolidation loan may be higher than the combined payments on your current debt.

4. You have no budget in place, and it’s not certain you can live within your means even after the consolidation.

Neither you nor your spouse are fully prepared to avoid using credit in the near future.

Bottom Line – Debt Consolidation

Debt consolidation can be a debtor’s best friend. You can think of it as something of a get-out-of-jail-free card. That’s because debt consolidation is something like voluntary bankruptcy.

Rather than defaulting on your loans, you’re consolidating them into a single loan with one monthly payment and then paying off all your debt within a few years. And as a bonus, the debt consolidation will produce an improvement in your credit score, which is the exact opposite of what will happen with bankruptcy.

But just remember that debt consolidation will only work if you have the discipline to maintain control over your finances and avoid incurring new debt until the consolidation is fully paid.

If you can get those two factors under control, debt consolidation may be the right strategy for you.