If you’re a first-time homebuyer, you may be feeling shut out of the market in the current fast-rising house price environment. But precisely because you are a first-time homebuyer, there may be help on the horizon. Major lenders, local governments, and non-profit organizations commonly offer first-time homebuyer programs to help you purchase a home.

You may be able to get a first-time homebuyer program that provides the loan to purchase the home, the down payment, or even a combination of both. More than anything, it’s a matter of knowing what the programs are and where to find them.

And don’t worry if you’re not technically a first-time homebuyer. First-time homebuyer programs have a very generous definition of what qualifies as a first-time homebuyer. If you haven’t owned a home in the last few years, it’s likely you’ll qualify for most programs.

What Are First-Time Homebuyer Programs?

Table of Contents

- What Are First-Time Homebuyer Programs?

- Common First-Time Homebuyer Program Requirements

- How Many Types of First-Time Homebuyer Programs Are There?

- First-Time Homebuyer Mortgage Programs

- Down Payment Assistance Programs

- Where to Start Your Search for First-Time Homebuyer Programs

- What Are the Benefits of First-Time Homebuyer Programs?

- Are There Any Drawbacks to First-Time Homebuyer Programs?

- Final Thoughts: First-Time Homebuyer Programs

First-time homebuyer programs recognize the greater challenges first-time homebuyers have, compared with those who either currently own a home and are trading up or have at least owned a home in the past.

Though some first-time homebuyer programs are offered as first mortgages, many more provide down payment assistance. That assistance recognizes the special difficulty first-time homebuyers have in coming up with the down payment to make that first home purchase.

Though a down payment is an issue in most markets, it could be especially problematic in high-cost areas. Just coming up with a down payment of 5% on a $500,000 home in a high-cost market means a first-time buyer would need to save $25,000.

Given that many first-time homebuyers are in the low- to moderate-income range, saving that much money can take several years. While the buyer is saving the money needed, property values may continue to escalate, further increasing the amount of the down payment needed. That can lock the buyer into a Catch-22 situation of always being behind the amount of cash needed to make the down payment.

First-time home buyer programs are available to help buyers overcome that dilemma.

Common First-Time Homebuyer Program Requirements

If you’re interested in a first-time home buyer program, you should know that there are requirements you’ll need to meet.

First, a common requirement is that you cannot have owned a home within the previous three years. Under this definition, you won’t be excluded from a first-time homebuyer program even if you have owned a home in the past. As long as the ownership did not take place within three years before purchasing a new home, you can still qualify.

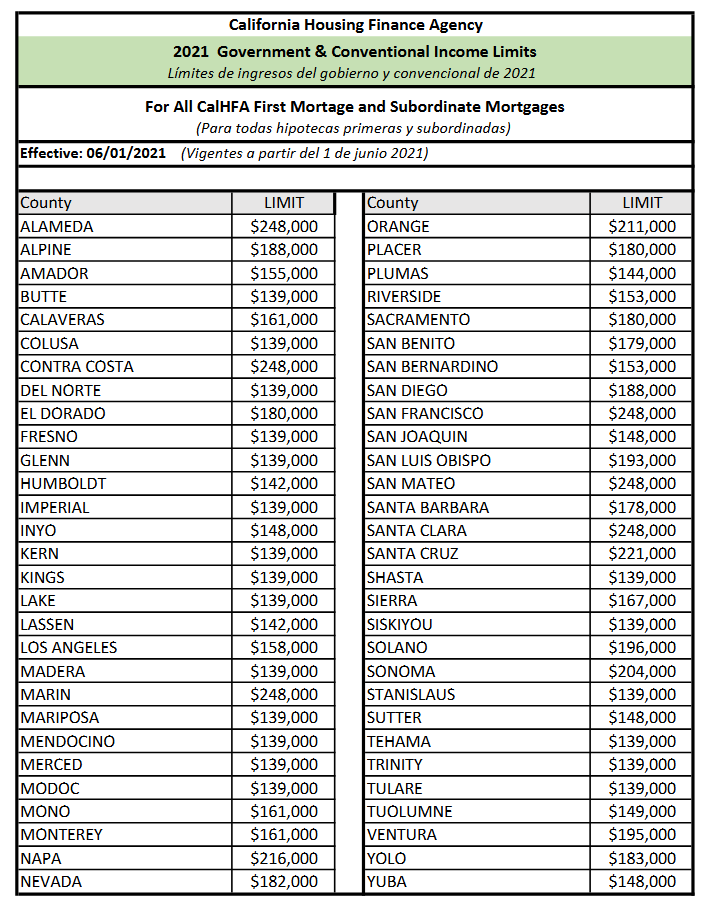

Another very common restriction is income limitation. First-time homebuyer programs will generally limit your household income to a certain percentage of the median household income for the county where the home is being purchased. The program might put a ceiling of 150% of the median income for the county. If the median household income in the county is $80,000, the maximum income to qualify will be $120,000.

As an example, the screenshot below shows the income limits for participation under the California Housing Finance Agency (CalHFA) MyHome Assistance Program:

Still another limitation is property type. In most cases, you’ll be limited to purchasing a single-family home, which typically will include condominiums and planned unit developments. Manufactured housing may be permitted, but only when it is built on a permanent foundation. In addition, the property must be owner-occupied by the purchaser as a primary residence.

Finally, there’s usually a homebuyer education requirement. Because the programs are designed for first-time homebuyers, the education requirement is imposed to make sure that would-be homeowners fully understand the financial implications of the transaction they are about to enter. Typically, homebuyer education will be provided by government agencies or nonprofit organizations. You must earn a certificate of completion in the course to be eligible for the first-time homebuyer program.

How Many Types of First-Time Homebuyer Programs Are There?

As mentioned at the beginning of this article, first-time homebuyer programs are available for purchase money mortgages, down payment assistance, or even a combination of both.

First-Time Homebuyer Mortgage Programs

These are typically low-down-payment loan programs. However, they’re not necessarily designed specifically for first-time homebuyers.

For example, VA loans are designed specifically for veterans and generally provide 100% financing. That eliminates the down payment requirement, which is the primary purpose of first-time homebuyer down payment assistance programs. VA loans also tend to be more consumer-friendly for veterans. For example, VA loans tend to be more lenient with credit than conventional mortgages.

FHA mortgages are similar, except they do require a down payment of 3.5% of the purchase price. However, down payment assistance programs are often provided in conjunction with FHA mortgages, resulting in zero-down payments. This is especially true with down payment assistance programs provided by local governments. Meanwhile, FHA is more flexible in evaluating your credit than conventional mortgages are.

Not to be outdone, conventional mortgages also offer advantageous first-time homebuyer loan programs.

For example, the Federal National Mortgage Association (FNMA), commonly known as “Fannie Mae”, offers its HomePath program. The program provides homebuyers with exclusive access to repossessed properties before they are made available to investors.

That will give homebuyers an opportunity to purchase these properties at a lower price than might be the case in an open bidding situation. In addition, buyers are able to purchase these homes with a down payment of just 3% of the purchase price.

In addition, Fannie Mae offers the ability for homebuyers to purchase homes with up to 105% of the value of the property by using a subordinate lien in conjunction with the first mortgage. The lien must be an eligible Community Seconds loan.

In yet another benefit of the program, Fannie Mae reduces the cost of the private mortgage insurance required for the first mortgage. However, it does require a minimum credit score of 680, which may require some first-time homebuyers to consider an FHA loan instead.

Down Payment Assistance Programs

One of the biggest obstacles to homeownership for first-time homebuyers is coming up in the down payment. But if you qualify as a first-time homebuyer, there are often down payment assistance programs that will cover your down payment. Some will also provide additional funds to cover closing costs if those will not be paid by the property seller.

Down payment assistance programs are commonly offered by local government agencies, including states, counties, and even cities. Others are provided by nonprofit agencies.

Down payment assistance programs can come in the form of either a loan or a grant. In many cases, a down payment assistance loan will be forgiven if you meet certain requirements.

Down Payment Assistance Loans

An example of down payment assistance is, once again, the California Housing Finance Agency (CalHFA) MyHome Assistance Program. The program offers a deferred payment junior loan of the lesser of 3.5% of the purchase price or appraised value with a down payment and/or closing costs, or $15,000, whichever is lower.

However, there is no cap on the loan amount if the homebuyer is an employee of either a school or fire department or those purchasing new construction homes or manufactured homes.

First-time homebuyers cannot apply directly with the Housing Authority for the loan. Instead, CalHFA makes the loans available through approved lenders. Interest rates will vary based on your financial circumstances, as well as lender fees and other factors. The program does require homebuyer education.

Because it is a deferred loan, it is considered a “silent second”. That means payments on the loan are deferred, so you don’t have to make any until the home is sold, refinanced, or the loan is paid in full.

Most states offer some type of down payment assistance loan program, though the specific details will vary from state to state. Check with your lender or do a web search using “(YOUR STATE) down payment assistance programs”.

Down Payment Assistance Grants

Some down payment assistance programs start out as loans but eventually convert into grants. These are commonly referred to as forgivable loans.

For example, you may receive second loan proceeds from a government agency, but the loan may be forgiven if you remain in the home for at least five years. Such loans often carry 0% interest rates, which ultimately makes them grants or loan/grant hybrids.

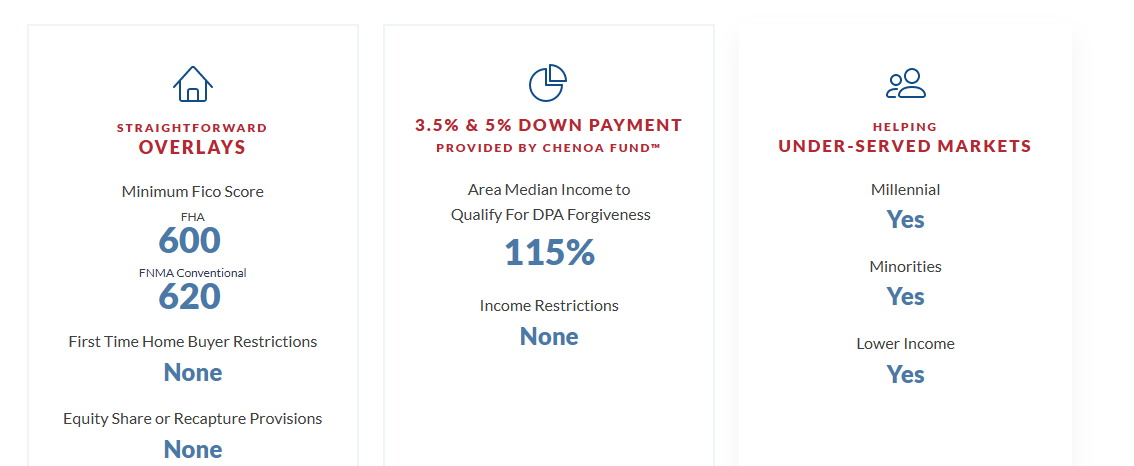

An example of this type of loan is the Chenoa Fund. It’s a federally chartered, public purpose-driven government agency that exists to provide affordable and sustainable homeownership to creditworthy borrowers who lack the funds to make a down payment. And fortunately, it’s available nationwide.

The fund will provide down payment assistance to cover a down payment of 3.5% (FHA) or 5% (conventional) of the purchase price of the property. The program has no income restrictions, but your income cannot exceed 115% of the median income level in your area to be eligible for loan forgiveness.

The program does have credit requirements and is not restricted to first-time homebuyers alone.

The screenshot below provides a summary of the program benefits and requirements:

Where to Start Your Search for First-Time Homebuyer Programs

Quicken Loans/Rocket Mortgage

Rocket Mortgage is the origination arm of Quicken Loans, which is the largest retail, residential mortgage originator in the country. You’ll apply for your loan through Rocket Mortgage – generally on the mobile app – but the loan will ultimately be funded by Quicken Loans.

Rocket Mortgage operates entirely online and provides conventional, FHA, and VA mortgages. Because the entire process is online, they can process loans faster than much of the competition. This is because they can often obtain verification of employment and savings directly from employers and financial institutions. That will eliminate much of the documentation typically associated with the mortgage application process.

Veterans United

As the name implies, Veterans United specializes in VA mortgages. In fact, they’re the largest VA mortgage lender in the country. It’s not hard to see why. The company regularly consults with former senior enlisted members of each branch of the US military. This helps to make the lending process as comfortable and accommodating as possible for veterans and active-duty members of the military.

They also have the advantage of having their own network of real estate agents, under Veterans United Realty. Since VA loans are a special type of mortgage, there are certain requirements a real estate agent will need to be aware of. Because the network is comprised of agents experienced in VA mortgages, they’re better able to serve the needs of veterans, current military members, and their families.

Credible

Credible is an online loan aggregator. They provide student loans, student loan refinances, personal loans, and credit cards. But they also specialize in home loans, including first mortgages.

Because it is a loan aggregator, you’ll complete a brief online application and receive loan quotes from multiple mortgage lenders. You can then choose the lender offering the program and pricing that will work best for you. In this way, Credible is an excellent choice if you’re looking to shop for the best lender for your home purchase.

loanDepot

loanDepot is a nationwide mortgage lender providing conventional, Jumbo, FHA, and VA loans. Much like Rocket Mortgage, it operates as an online lender. You’ll complete the loan application online and upload any documentation directly onto the website.

Because it is an online process, it can be handled either from your home or your place of employment.

What Are the Benefits of First-Time Homebuyer Programs?

- Covers your down payment and sometimes closing costs, enabling you to purchase a home with no money out-of-pocket.

- Recognized programs that can work with conventional, FHA, and VA first mortgages.

- Though many do have minimum credit score requirements, you don’t need perfect credit to qualify.

- Programs generally target those who fall in the low- to moderate-income category.

- Many down payment loan assistance programs offer loan forgiveness, eliminating the need to make repayments.

Are There Any Drawbacks to First-Time Homebuyer Programs?

- With many first-time homebuyer programs, you will be required to meet certain income standards. They are not typically available to the general home-buying public.

- Programs are available only for owner-occupied primary residences, not vacation homes or investment properties.

- Because you won’t be making a down payment, you’ll have no equity in the property you’re purchasing. If the property value declines significantly, you could be in a negative equity position for many years.

- The 0% equity situation can also lock you into staying in the home for many years. If a home turns out to be the wrong choice, you’ll still be locked in.

- If you don’t stay in the home long enough to qualify for loan forgiveness, you’ll be required to pay off the down payment assistance loan balance upon the sale of the property.

- Refinancing the home or converting it to an investment property could also trigger a repayment requirement.

- Some down payment assistance loan programs do require monthly payments, including interest.

Final Thoughts: First-Time Homebuyer Programs

First-time homebuyer programs play a vital role in facilitating homeownership amidst rising house prices. These programs offer crucial assistance in the form of down payment funds, ensuring accessibility to the housing market. Despite varying requirements, such as income limitations and homeownership history, these initiatives provide options for low- to moderate-income individuals.

Whether through mortgage loans, down payment assistance, or a combination of both, these programs offer pathways to owning a home. However, potential downsides include limited equity, residency constraints, and potential repayment obligations. Careful consideration of program terms and personal circumstances is essential for a successful homeownership journey.