“Bitcoin is the hardest asset you can own in the 21st century….“

“What I can do with Bitcoin is similar to what I can do with a piece of real estate….“

“Bitcoin has all the positive attributes of real estate with none of the flaws…..“

The above were a few quotes from a good friend of mine who I’ve always viewed as a real estate expert.

For as long as I’ve known him he’s been determined to become the most successful real investor. He’s always adapting his business to reflect market conditions and always staying one step ahead of the curve.

So I was a bit surprised when he contacted me after he saw some of my videos on cryptocurrency. But not as surprised after I sent him a text after Bitcoin pulled back last fall and got this response:

There was so much good information he shared on cryptocurrency and Bitcoin that it made me look at it much differently. I was already excited about the crypto space but his views made me THAT much more ecstatic.

What really fascinated me was how he looked at Bitcoin as having all the pros of real estate without many of the cons. And that’s what I want to tackle in this article: Bitcoin Vs. Real Estate – Which is the Better Investment?

Table of Contents

Why Bitcoin Is a Better Investment Than Real Estate

The best way to make the point is to compare Bitcoin and real estate side-by-side, analyzing the advantages and disadvantages of each.

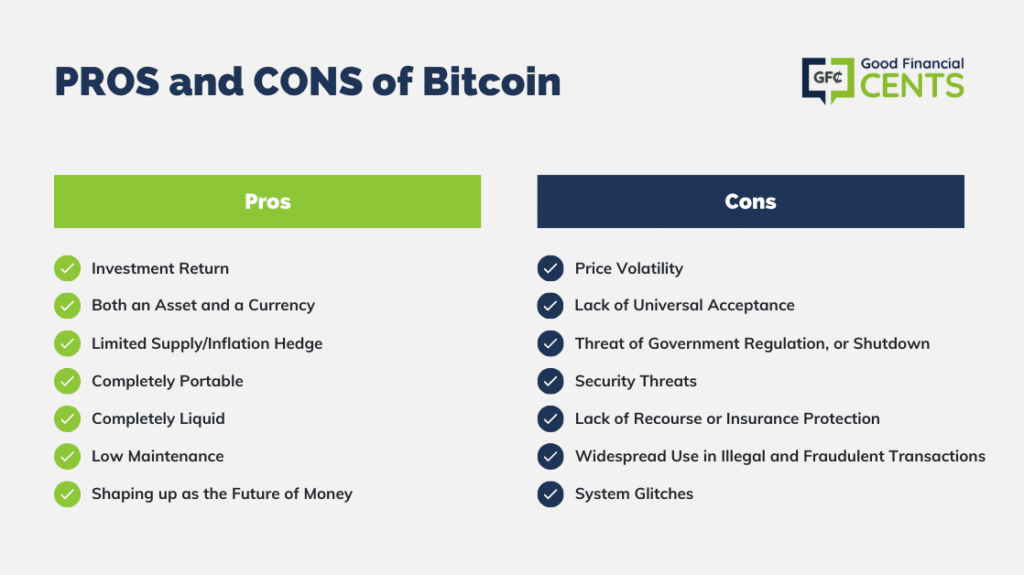

The Case for Bitcoin – Pros

In the next two sections, I want to present the pros and cons of both Bitcoin and real estate. But ultimately, I believe the Bitcoin pros outweigh its cons and even eclipse the pros of real estate.

1. Let’s Start With Investment Return

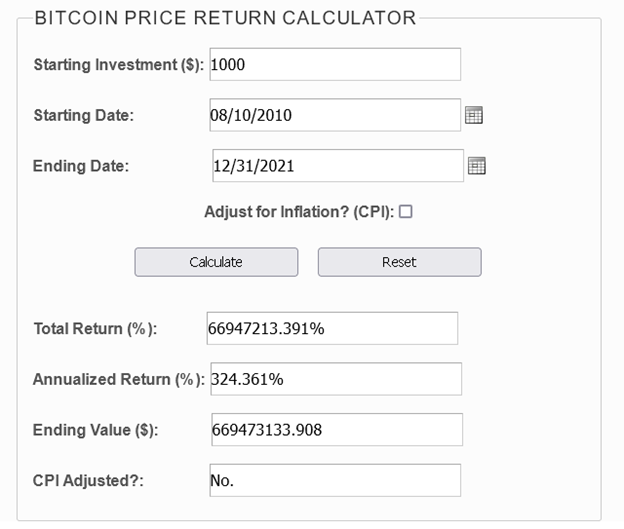

I’m listing this as the first pro because it’s the most obvious advantage. The return on Bitcoin since 2010 has been nothing short of mind-boggling.

According to calculations run on dqydj.com, Bitcoin has had a total return of 39 million percent between August 10, 2010, and September 20, 2023.

That works out to be almost 267% annually. 😳

There isn’t another investment or asset class that’s come close in such a short space of time.

2. Bitcoin Is Both an Asset and a Currency

There’s little doubt Bitcoin’s primary attraction over the past decade has been its investment performance. Numbers like those above are impossible to argue against.

But Bitcoin is also a currency. It can be used to buy and sell products and services with both merchants and individuals. Even though the price of a single coin is far too high for most transactions, Bitcoin is divisible. It’s available in smaller denominations, referred to as Satoshi.

There are 100 million Satoshi per one Bitcoin. The rough conversion into dollars is about 10 Satoshi to one penny, and 1000 Satoshi to $1. Bitcoin may be too expensive to use for everyday transactions, but Satoshi may be just right. Meanwhile, the number of merchants accepting Bitcoin and other cryptocurrencies has been growing steadily. A recent article on Inc.com reported that one-third of US small businesses now accept cryptocurrencies as payment.

3. Limited Supply/Inflation Hedge

We’re going to go into this a little deeper later in this article, from my podcast interview with a friend I refer to as The Crypto Guy. But this is an important quality because it largely explains why Bitcoin is an outstanding inflation hedge.

When Bitcoin was first launched, it was programmed with an absolute limit of 21 million coins. That gives a limited supply, and while the limit has yet to be reached, the price may continue rocketing higher once it does.

Compare that with the U.S. dollar, which can be printed in unlimited quantity by the Federal Reserve. That printing capability, which, accelerated by the coronavirus pandemic, is the reason we have inflation.

Dollars can be printed in unlimited quantities, but Bitcoin will never exceed 21 million coins. That’s a guarantee that Bitcoin will continue to outpace inflation.

4. Bitcoin Is Completely Portable

This is another feature that makes it suitable as money. But it’s also an advantage over real estate.

Real estate is not portable at all. If you decide to move to another state or country, you’ll need to liquidate your real estate holdings before you move. You can’t bring it with you.

Bitcoin acts just like electronic money. You can move to another state, or even another country, and still have access to your crypto.

5. Bitcoin Is Completely Liquid

This is yet another quality that makes it suitable as money. You can easily liquidate Bitcoin, even in a matter of minutes. You can use it to buy goods or services, convert it into another crypto, or even into fiat currencies, like the dollar or the euro.

That also makes it easy to speculate on price swings. You can sell out of a Bitcoin position just as quickly and easily as you can buy in.

You can’t do any of that with real estate.

6. Bitcoin Is Low Maintenance

Unlike real estate, you don’t have to invest time, effort, or money in maintaining it. And you’ll never get a phone call in the middle of the night from an angry tenant.

“Bitcoin has been the best-performing asset of the last decade, regardless of where the Bitcoin holder is in the world,” according to Ian Kane, CEO, and founder of Unbanked.com, a company that connects individuals and organizations with the financial benefits of the blockchain. “The same cannot be said for real estate. Bitcoin is similar to real estate in the fact that it’s an inflation hedge. However, there is no upkeep on BTC—you don’t have to worry about real estate taxes, cutting the grass, fixing the roof, etc. You only have to buy your BTC and hold it to let it do its thing. You can even earn interest on your BTC.”

Ian Kane, CEO of Unbanked.com

7. Bitcoin Is Shaping up as the Future of Money

Most people believe money is a fixed commodity. It’s not. It’s been evolving for centuries. Up until a couple of hundred years ago, people largely used barter to transact business. Mostly that involved trading commodities. Two farmers might have traded 10 bushels of wheat for 20 gallons of milk.

For thousands of years, gold and silver have served as money, each recognized because it’s valuable, rare, and widely accepted. But gold and silver gave way to paper money in the early 20th century, and paper money has largely been replaced by electronic transfers and plastic cards.

Cryptocurrency is increasingly being seen as the next evolution of money, with Bitcoin being the leader in the space.

If that’s true, it’ll just be a question of time before the money we’ve been using all our lives is replaced by crypto.

Changes in technology are affecting everything in the world. That includes money, which may be going through a historic transition right before our eyes.

The Case Against Bitcoin – Cons

As an investor in crypto, I’ll be the first to admit there are a few negatives. But we also have to factor in that crypto is a new and evolving technology. It’s very likely some or all of these disadvantages will be addressed.

1. Price Volatility

The same price volatility that’s creating crypto millionaires has the real potential to undo crypto’s primary mission, which is to act as a medium of exchange—money.

My guess is that volatility probably has more to do with the novelty of crypto than anything else. As a new asset class coming onto the scene, investors are flocking into crypto, especially Bitcoin.

Eventually, that should settle down. As crypto continues to gain acceptance as money, its price movements are likely to become more predictable. But even when it does, it’s likely to see big price swings in response to major events, like economic booms and busts, war, political instability, pandemics, and energy/commodity shortages.

2. Lack of Universal Acceptance

Even though crypto is rapidly gaining acceptance among merchants and individuals, there are still major areas of the economy that don’t recognize it.

For example, you still can’t transact business at your bank with crypto. You also can’t pay your taxes, or buy gasoline or groceries. And neither insurance companies nor utility companies accept payments in crypto.

That said, I think this is an issue that is already working itself out right before our eyes.

3. The Threat of Government Regulation, or Shutdown

This has been a concern of crypto investors from the very beginning. But I believe the threat of a crypto shutdown is unlikely, despite the ban by China last year.

And, as it turns out, regulation may not be such a bad thing.

“As 2021 comes to a close, the 117th Congress has introduced 35 bills in 2021 focused on cryptocurrency and blockchain policy,” reported Forbes contributor Jason Brett in December. “As the Infrastructure Investment and Jobs Act (H.R. 3684) made headlines with language on crypto tax reporting that is now law, the surprising reaction from the crypto lobby showed that this industry was likely here to stay.”

I highlighted the last sentence because it’s evidence the crypto industry accepts that regulation is inevitable. But that’s hardly a bad thing. After all, both real estate and the stock market are regulated, and that hasn’t stopped investors from making money in both asset classes for generations.

4. Security Threats

The cryptosystem faces many of the same threats all other financial networks do, including the banking system. Systems can be hacked, and there’s always the possibility of some sort of mechanical meltdown.

There are also security threats at the individual level. For example, crypto investors have been known to lose their security codes or digital wallets.

But like every other new system or network put in place, it’s likely most of these bugs will be worked out. They will not be eliminated completely, just as is the case with other systems. But it’s likely the threats will be reduced to a small level that is no longer considered a threat to the entire system.

5. Lack of Recourse or Insurance Protection

This may be the single biggest con keeping more investors out of crypto. Bank assets are covered by FDIC insurance, while brokerage accounts are protected by SIPC. No such blanket protections are currently available to crypto investors.

But all that can change as crypto gains greater acceptance and becomes a mainstream asset. If enough people are invested in any asset, governments will inevitably set up some sort of safety net.

There is already evidence of progress on this front. One major crypto exchange, Gemini, is both regulated by the New York State Department of Financial Services and offers private insurance coverage for crypto you hold on the exchange. It’s likely other crypto exchanges will follow the same path if only to be in a better position to compete.

6. Widespread Use in Illegal and Fraudulent Transactions

Who hasn’t gotten one of those shadowy emails demanding payment in Bitcoin? This probably owes to the fact that crypto is unregulated and has famously been reported as being completely anonymous. We can also suppose any time an asset becomes particularly valuable, it also becomes a prime target for criminal activity.

But the anonymity factor may be overrated. Last June, the FBI successfully recovered $2.3 million in Bitcoin from a ransomware extortion scheme. They did it using an old-fashioned and time-tested method of following the money.

Ultimately, crypto may not be the playground for illegal activity that many suppose it to be.

7. System Glitches

There’s been a fear of system glitches from the very beginning. Maybe some unforeseen technical problem takes down the entire system, wiping out billions of dollars of cryptocurrencies.

Though there have been some such glitches over the past 13 years, each has been resolved. What may be more remarkable is that we have yet to experience a crypto system collapse while crypto is in its infancy and most vulnerable to those outcomes.

The Case for Real Estate – Pros

As you might guess, I’m a big fan of crypto. But that doesn’t mean I think real estate is a bad investment. Quite the opposite, it’s an excellent investment.

In fact, a majority of millionaires have made their wealth due to their real estate investments.

90% of all millionaires become so through owning real estate.

I just don’t think it’s as good as crypto, and I believe that will continue to be the case in the future.

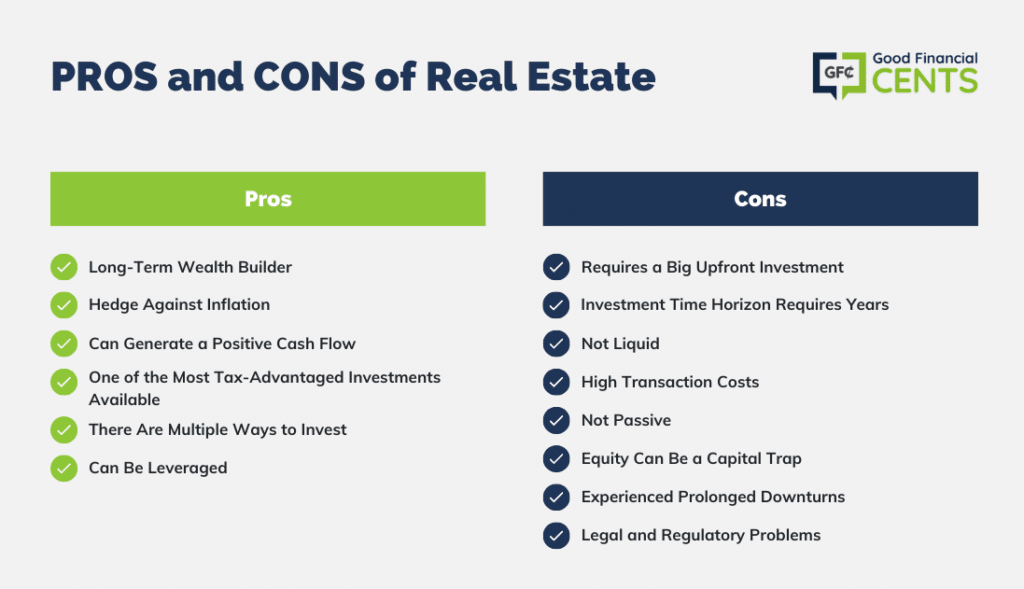

1. Real Estate Is a Long-Term Wealth Builder

It can be hard to figure out what investment returns will be on real estate since there are so many different ways to invest. You can invest in residential rental property, commercial property, fix-and-flip deals, or just own your own home.

According to the National Association of Real Estate Investment Trusts (NAREIT), the average annual return on all types of real estate has been 11.8% for the last 40 years. That’s very close to the average annual rate of return on stocks. With returns like that, real estate has proven to be one of the best long-term, all-weather investments.

With an average return that high, a $25,000 investment in real estate today could grow to $220,910 in 20 years. That’s a near 10-fold increase in your investment. It doesn’t come close to matching the performance of Bitcoin over the last decade, but it comes out looking good compared with every other investment.

2. Real Estate Is a Hedge Against Inflation

Considering that inflation has averaged about 3% per year over the past 30 years, the 11.51% average return on real estate has investors well ahead of that spiral.

3. Real Estate Can Generate a Positive Cash Flow

Of course, I’m referring to rental real estate. Whether you invest in residential or commercial real estate, rental income can produce a positive cash flow. Real estate investment trusts pay out net rental income to investors through quarterly distributions.

In that way, real estate can produce a steady income while its price is increasing for an eventual windfall on sale.

4. It’s One of the Most Tax-Advantaged Investments Available

As a real estate investor, you’ll have the benefit of claiming depreciation expense against the property. Since depreciation is a paper expense, your net rental income will be at least partially tax-deferred.

Meanwhile, you get the benefit of a lower long-term capital gains tax rate when you sell your property after several years. That will lower your tax rate on the profit on sale to between 0% and 20%. And that’s a lot lower than the ordinary income tax rates, which range between 10% and 37%.

5. There Are Multiple Ways to Invest in Real Estate

As I said earlier, you can invest in real estate by purchasing your own home, buying rental property, or starting a fix-and-flip business. But more passive ways to invest in real estate, the kind you can hold in an investment portfolio, are real estate investment trusts and real estate crowdfunding platforms.

Real estate investment trusts, or REITs, are like mutual funds that hold commercial properties rather than stocks or bonds. You’ll buy shares in a fund on major stock exchanges, just as you would with a mutual fund or an exchange-traded fund. REITs pay dividends that can include both net rental income and capital appreciation.

Real estate crowdfunding platforms are more specialized ways of participating in real estate investing. A platform like Fundrise can provide investments based on income, growth, or a combination of both.

6. Real Estate Can Be Leveraged

I save this pro for last, since it can also be a con, but you can purchase an owner-occupied primary residence with as little as 3% down. That’s a $9,000 investment in a $300,000 home.

Investment property usually requires a larger down payment, typically 20%. Still, you can purchase a $300,000 investment property with $60,000 down and borrow the rest. Since your investment returns will be based on the $300,000 purchase price, they’ll be a lot higher based on your $60,000 investment.

For example, let’s say you sell the property in five years for $400,000. After the sale, you’ll have earned a $100,000 profit on your $60,000 investment. That’s a return of 167% in five years.

That said, leverage does have a dark side. If property values drop, as they did during the last recession, leverage works in the opposite direction. The wave of foreclosures that hit during the recession was largely due to people owing more on their homes than they were worth.

The Case Against Real Estate – Cons

1. Requires a Big Upfront Investment

You can invest in Bitcoin with as little as $100 (or less) through most crypto exchanges and investment brokers. Real estate will require a large upfront down payment, especially if you purchase an investment property.

The high initial investment required to purchase a single property can make it difficult to diversify across several.

2. The Investment Time Horizon Requires Years

While you can conceivably make big profits on Bitcoin in a matter of days, you generally have to wait at least five years for investment real estate to pay off. That will give you the time needed for you to gradually increase the rents, while the property value increases.

3. Real Estate Is Not Liquid

Even in the strongest real estate markets, it can take months to sell a piece of property. It can be an even bigger problem with commercial property since each is unique.

In the meantime, the only way to get cash out of real estate is to borrow against it. There are limits to how much you can borrow, and while you may get the cash you need, you’ll also be creating an ongoing liability.

4. High Transaction Costs

Between real estate commissions, transfer taxes, seller pay closing costs, and other expenses, it can cost up to 10% of the property’s sale price to sell a residential home. The percentage may be even higher for commercial property. That will take a big chunk out of your profit, and also limit your ability to sell the property quickly.

5. Real Estate Investing Is Not Passive

Despite all the get-rich-quick-in-real estate-without-doing-anything books and programs, real estate investing is not passive (except for REITs and real estate crowdfunding).

When you own investment property, whether residential or commercial, you’ll need to find tenants, collect rents, replace tenants when they leave, make repairs when needed, periodically renovate, and cover the cost of lawn maintenance, snow removal, and even certain utility costs.

Many of those same costs apply to your primary residence.

By contrast, Bitcoin has no such ongoing maintenance expenses.

6. Real Estate Equity Can Be a Capital Trap

This is a combination of a large down payment requirement and the number of years it will take to realize a profit. In the meantime, your money will not be available for other purposes. That includes making other investments, like buying additional properties or investing in other asset classes.

7. Real Estate Has Experienced Prolonged Downturns

There’s no doubt real estate increases in value over the long term. But there have been times when property values went down. The most recent example was the Great Recession a few years ago. Property values crashed, real estate became illiquid, and millions of people lost their homes in foreclosure.

This is something similar to the big price drops experienced by crypto. But while crypto collapses can reverse in a matter of weeks, real estate declines tend to last for several years.

As the saying goes, “Markets can stay irrational longer than you can stay solvent.”

That’s a bigger problem with real estate than it is with other investments.

8. Legal and Regulatory Problems

This is a potential problem with investment real estate. If someone is injured on a property you own, they’ll pursue compensation against you. Even if you have property insurance, it may not be sufficient to cover the amount of a claim. The claim may also relate to an event that’s not covered by your policy. Either situation could lead to a lawsuit against you personally.

On the regulatory side, local governments can pass laws that affect landlords. Rent control is one example. But we had a more general episode during the COVID-19 pandemic when thousands of municipalities declared moratoriums. Those enabled tenants to stop making rent payments, while the landlords were still responsible for paying for the cost of the property.

A Former Real Estate Investor Goes All in on Bitcoin

This is a good time for me to confess that I was not an early adopter when it came to crypto. It would be much closer to the truth to say that I was an early crypto skeptic. That’s changed, and now I’m all in.

Part of my epiphany was a podcast interview I did with the former real estate investor who switched gears into crypto during the COVID pandemic in 2020. You can listen to the podcast at GFC S2 Ep. 102 – Real Estate Investor Sells 90% of His Business to Do Crypto – Here’s Why. Before the interview, I had been dabbling in crypto. But after—let’s just say the light went on for real.

The person I interviewed, who I call simply The Crypto Guy, was a real estate agent I met when I sold my first home back in 2008. He absolutely blew me away with his knowledge of real estate. You see, he wasn’t just a real estate agent, but an investor as well. Mostly, he flipped properties and short-term rentals. We’re talking about 40 flips per year!

The Crypto Guy was cruising along on real estate easy street, working just two days per week. That is, until the pandemic hit.

As the pandemic shutdown gripped the economy, Crypto Guy reevaluated his real estate empire and began repositioning his portfolio. Mostly that meant selling off the majority of his properties.

Crypto Guy was experiencing problems unique to anyone working in the fix-and-flip side of real estate. That included fast rising cost of materials and a chronic shortage of contractors, both of which are critical to that type of investing. Then there was the issue with the ban on tenant evictions.

It’s easy enough to see why Crypto Guy felt the need to rethink the business he was so successful in.

Why the Crypto Guy Moved Into Bitcoin

It’s a funny thing about a crisis; it can cause you to rethink everything you thought you knew. And that’s what happened with The Crypto Guy.

He engaged in a deep study of cryptocurrencies. After spending about 50 hours studying the digital asset, he knew what his next move would be.

You can listen to the podcast to get the full line of Crypto Guy’s reasons for turning to crypto, but here’s a summary of the highlights:

- He felt both real estate and stocks were in a bubble.

- Sensed that inflation was not transitory and needed an investment that would provide a long-term response.

- Bitcoin has been the best performing investment of the past few years.

- Bitcoin can be leveraged, just like real estate, but was easier to liquidate—it could be sold with a single keystroke.

- Crypto earns interest—over 6% per year. That was way better than the 0.0-something being paid by the banks in cash.

“Bitcoin is a new asset and very volatile,” The Crypto Guy told me. “Price volatility is where the profit is. I’m happy when the price drops because that means I can buy more.”

Is Crypto a Fad?

Even though I was already investing in crypto myself, I had to ask the question that’s on a lot of crypto investors’ minds: Is crypto a fad?

Crypto Guy doesn’t think so. “The major currencies of the world are ‘fiat money’, and none of the 700 or so that have existed in history ever lasted. The U.S. dollar is one of the latest versions. But it’s backed by the promise of the government, and nothing else.”

“Crypto is evolving into another form of money, and its acceptance is increasing. Meanwhile, the Federal Reserve has painted itself into a box on the money supply. They can’t stop printing money, which lowers its value. Inflation is simply too much money in the system, with not enough places to go. The CPI is being reported as 6%, but I think it’s more like 14%–15%.”

Crypto Guy also pointed out that Bitcoin has now been around for 13 years and is still here despite being banned by China.

Crypto Guy believes Bitcoin is always going to outpace inflation because it’s limited to just 21 million coins, while the Federal Reserve can literally print an unlimited number of dollars. He sees Bitcoin as Gold 2.0, and as a transition that will ultimately change the way people transact business.

“Everything is being digitized,” Crypto Guy said. “Think music, maps, and payment systems, among others. Millennials live their lives on their phones, so this is a natural transaction for the younger generations. When your parents were on a long trip, they took the latest version of the Rand McNally Road Atlas with them. Today, most people rely on their smartphones.”

He had me on the road atlas point. And like everyone else, I’ve seen what the investment returns have been on Bitcoin and other cryptos.

I think this interview is where I experienced my conversion from crypto dabbler to crypto investor.

Final Thoughts on Bitcoin vs Real Estate: Why Bitcoin (Crypto) Is a Better Investment

Bitcoin prevails as a superior investment over real estate due to its unmatched liquidity, accessibility, transparency, and security. With minimal capital requirements and round-the-clock availability, Bitcoin caters to a wider investor base. Its blockchain technology ensures transparent, fraud-resistant transactions. While real estate holds its merits, Bitcoin’s potential for rapid growth and adaptability in the digital age make it an enticing choice for those seeking to diversify their portfolios and capitalize on the evolving financial landscape.

I saved my coins on this fake exchanger platform. I trusted them with my coins, thinking it would be safe with them but it wasn’t. I woke up one day and found out all my bitcoin had been transferred out. I never gave permission for this, I never gave my recovery phrase for this and I never gave any passwords for this. I contacted them and they did nothing to help. They refused to give me an explanation of what happened and why. It took a long time before I could be able to hold them responsible for what they did. It is a pattern of theirs to lure you in to trust their platform with you thinking your coins are safe with their exchanger, they deny you all these. Thanks for the support of minerrobbertt @ g mailcom who took matter into their hands to help adjudicate and resolve the matter, I got back my funds and they got blacklisted as far as I am concerned. I advise you to do same