If you’ve never applied for a mortgage before, you may be surprised to learn it’s a more complex process than, say, applying for a credit card or even an auto loan. From application to closing, the process can take 30 days or more.

Table of Contents

This is why it’s so important to get approved for a home loan, especially if you’re looking to purchase a new home. That approval – commonly known as a pre-approval – will greatly improve the chances of getting the home you want when you want it. In fact, many real estate agents and home sellers won’t even consider a contract offer without a preapproval letter.

Key Takeaways

- A prequalification is a quote by any mortgage lender based entirely on your income, debt, and credit score inputs. It is not verified by the lender and does not affect your credit score.

- A preapproval occurs when a mortgage lender verifies the information provided on the application and offers the buyer a potential deal. They do this by requesting supporting documentation from you, as well as by pulling your credit reports.

- While you can use your local bank or credit union as the lender for your home, you have many options available at your disposal and it always helps to shop around for the best lender.

Pre-approval vs Prequalification

This is an area of some confusion for home loan applicants, especially those looking to purchase a home. Preapproval and prequalification are sometimes used interchangeably, which may cause a consumer to believe they’re simply two names for the same process. It isn’t.

Prequalification

Prequalification is where you contact the mortgage lender, or supply information on their website, mostly as a way to get a loan quote. You’ll provide general information, including your income, estimated credit score, debts, and current house payment. You’ll also provide the loan amount requested. If the prequalification is a purchase you’ll also need to provide the purchase price of the home and the amount of your anticipated down payment.

Based on that information, the lender will determine if you are qualified for the loan amount you are requesting.

More than anything else, a prequalification is simply a summary estimation of the loan amount you may qualify for, and the approximate rate which you can expect to pay.

But since none of the information you supply has been verified by the lender, the prequalification is based entirely on your representations. It should never be interpreted as a guarantee of ultimate approval by the lender. For that reason, prequalification letters are not well received by real estate agents and property sellers.

Pre-approval

A pre-approval works much the same way as a prequalification, except that it represents a lender’s approval of the loan amount you are applying for.

During the pre-approval application process, you’ll provide similar information as you would for prequalification. But you will be required to supply documentation relating to your employment, income, assets, and even certain debts.

The lender will then make a formal underwriting review of your application and supporting documentation, and issue a pre-approval. The approval will be subject to the selection of a property to purchase, a sales contract on the same, and any customary closing conditions.

Basically, a pre-approval means the lender has approved you for the loan requested based on your employment, income, and asset information. They’ll also pull a full credit report and credit score. Some lenders will even allow you to lock in an interest rate for a certain number of days while you search for a home. If it’s a refinance, you can close shortly after the pre-approval is issued.

The formal nature of a pre-approval is the reason why pre-approval letters are warmly welcomed by both real estate agents and property sellers.

How to Get Preapproved for a Home Loan

Getting pre-approved for a home loan starts with choosing a lender. Even though you’re only at the preapproval stage, you’ll want to be sure to apply with a company you are very likely to get your final loan from. That’s because once you have pre-approval, the home buying or refinancing process moves very quickly. Ideally, you’ll want to get a preapproval, choose a home (or refinance your current home) as quickly as possible.

Where to Get Preapproved for a Home Loan

Four of the top home loan sources in the industry are Quicken Loans, Rocket Mortgage, Veterans United, and Credible – but each for a different reason.

Quicken Loans is the largest retail mortgage lender in the country and provides most loan types. However, Quicken Loans are made primarily through Rocket Mortgage. That’s the online version of Quicken Loans, although they are the same company.

Rocket Mortgage is well known for fast approvals and an entirely online process where you can upload any required documentation to speed up the process. What’s more, they can often obtain verification of employment and assets directly with employers and institutions, minimizing the need on your part to supply any documents at all.

Veterans United is the leading VA mortgage lender in the country, providing more VA loans than any other company. That’s largely because it’s an extremely veteran-friendly company. They employ former senior enlisted members of each branch of the US military in advisory capacities to make sure their loan programs will provide the best product for veterans and active-duty military personnel.

If you’re buying a home, you can also work with Veterans United Realty, which is a network of real estate agents who specialize in working with veterans. They’re well acquainted with the nuances of the VA mortgage process.

Credible is a good source for a home loan if you’re mostly shopping for a lender. That’s because Credible is an online home loan marketplace, where a single application will get you quotes from multiple lenders. You can choose the program and lender that looks best to you, and then make an application directly with that lender. That will save you time and effort shopping for lenders on individual websites.

The Home Loan Approval/Pre-approval Process

During the home loan approval or pre-approval process, the lender will be looking at four personal financial categories: employment, income, credit, and assets.

Employment

What the Lender Will Look For:

The lender will look to verify your employment history of at least two years, though exceptions will be made for recent graduates or discharged members of the military. Though the employment should be continuous, lenders will accept a change of jobs as long as income has remained the same or is increasing. Short periods of unemployment are also acceptable on a case-by-case basis.

The same is true if you’re self-employed. You will need to be in business for a minimum of two years, with a history of stable or increasing earnings.

What Documentation You May Need to Provide:

The lender will usually send your employer what’s known as a verification of employment request, or perform a verbal verification directly from your employer. They’ll request your date of hire, your position, your income level, and the likelihood of continued employment.

If you’re self-employed, the lender may request either a business license or a letter from your CPA or tax preparer confirming you have been in business for a minimum of two years. If you’ve been self-employed for less than two years, the lender may not accept your income. An exception may be made if you’ve been in business for more than one year, and you’re in the same business you were in when you held a job.

Income

What the Lender Will Look For:

The lender will look for your verifiable income level, the stability of the income, then determine if the income will be sufficient to support the requested loan, as well as any other recurring debts you have.

The sufficiency of income is determined by your debt-to-income ratio, commonly known as a DTI. Basic permissible DTI ratios are 28/36 – the amount of the new house payment shouldn’t exceed 28% of your stable monthly income, while the amount of your new house payment plus other recurring debts should not exceed 36%.

That said, lenders will frequently exceed these ratios if you have strong compensating factors. These include excellent credit, a down payment of at least 20%, additional income not used to qualify for the loan, or a large number of assets after closing.

Your new house payment will consist of the principal and interest on the new loan, and monthly allocations for real estate taxes, homeowner’s insurance, private mortgage insurance (if required), and homeowner’s association dues (if required).

Other recurring debts will include monthly payments for credit cards, car loans, student loans, and child support or alimony.

What Documentation You May Need to Provide:

The most common documentation requested for income includes your most recent pay stub, W-2s for the past one or two years, and fully completed tax returns if you have non-salary income, such as commissions, bonuses, or rental real estate income.

If you’re self-employed, expect to provide fully completed income tax returns for the most recent two years. If you’re more than three months into the new year, the lender may request a year-to-date profit and loss statement, though this has become rare in recent years.

Credit

What the Lender Will Look For:

The lender will want to know you have acceptable credit. This is generally determined by your credit score. On conventional mortgages, you’ll be required to have a minimum credit score of 620. However, FHA mortgages accept credit scores as low as 580. If you’re applying for a jumbo mortgage (typically a loan amount in excess of $1,149,825), the minimum credit score will be at least 680 and can be much higher.

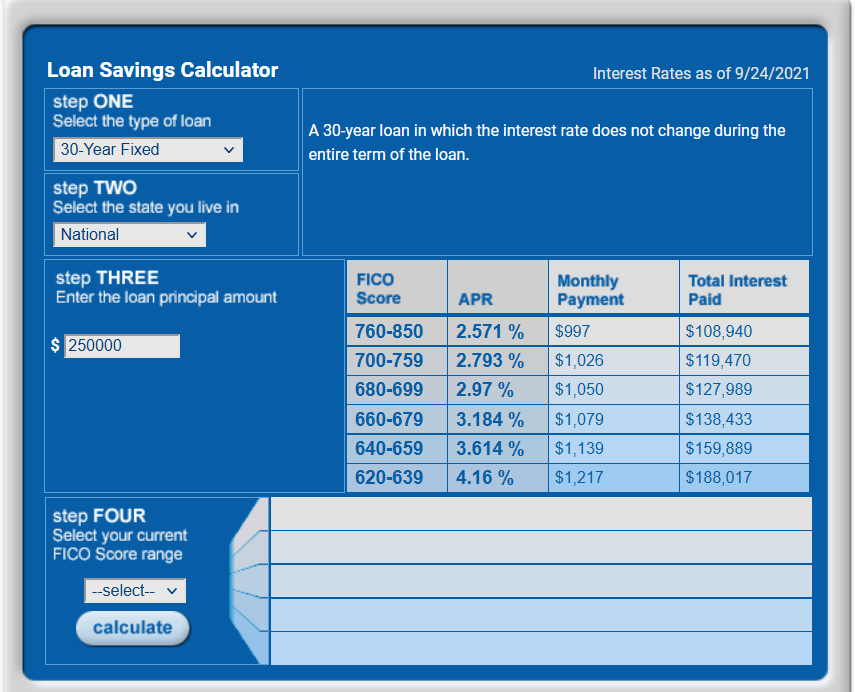

Using a conventional mortgage as an example, the myFICO.com Loan Savings Calculator shows the difference in the rate you’ll pay based on different credit scores.

Notice with a credit score of 760 or above, the interest rate is 2.571%, but goes as high as 4.16%, with a credit score below 640. That can make a difference in your monthly payment of $220. That makes a strong case for doing everything possible to improve your credit score before applying for a home loan.

But you should know that credit score alone is not the sole basis for determining loan approval. Lenders also look at credit quality, which includes major derogatory credit report entries, like bankruptcy and foreclosure.

If you have a bankruptcy, you’ll generally need to wait at least 2 to 4 years after discharge to apply for a loan. Foreclosures require at least seven years. However, the waiting periods will be reduced if either event was caused by extenuating circumstances, though additional borrowing limits may apply.

What Documentation You May Need to Provide:

When you provide your name, address, and Social Security number on the application, the lender will use that information to run a credit report on you, and any other borrowers applying for the loan. You do not, and should not, need to supply a credit report yourself.

The lender may ask for additional information if there are any concerns about your credit. For example, expect to provide a full explanation for major derogatory information, like bankruptcy, foreclosure, large charge-offs, or late payments of 60 days or more. The lender may also request documentation supporting your explanation.

Take both the explanation and documentation requests seriously. If the lender requests these, they’re looking for justification to approve your loan – not to decline you.

Assets

What the Lender Will Look For:

The lender may not request proof of assets if you are doing a refinance unless funds will be needed to close on the loan.

On new home purchases, the lender will want to know that you have sufficient funds to make the down payment, as well as cover any required closing costs and escrows.

If some of the funds for closing are coming from a gift from a family member or a friend with whom you have a family-type relationship, the lender will request a gift letter from the donor, as well as verification of the assets from which the gift funds will come. The lender will also request evidence of the transfer of the gift funds from the donor into your account.

The seller will be permitted to pay closing costs if it’s customary in your market area and if it doesn’t exceed 6% of the new loan amount.

What Documentation You May Need To Provide:

The easiest way to verify your assets is by providing the two most recent monthly statements for bank accounts, investment accounts, or retirement accounts you plan to use to cover the down payment and/or closing costs and escrows. If it’s more convenient, the lender may also send the financial institution a request for verification of assets, which will be completed by employees of that institution, and returned to the lender.

Once You Select a Property

If you are purchasing a home, you can begin making offers as soon as you have a pre-approval letter issued by the lender. Once you find a property,

you’ll need to provide the lender with a fully executed sales contract on the home, detailing all the terms and contingencies of the sale.

The lender may also request that you provide evidence of any deposit you have made on the home, especially if it is more than $500 or $1,000.

Final Thoughts on How to Get Approved for a Home Loan

Applying for a home loan is a complex process that involves multiple stages from application to closing, taking around 30 days or more. Securing a pre-approval, commonly known as pre-approval, is vital when seeking to purchase a new home. Real estate agents and sellers often require a preapproval letter before considering contract offers.

Prequalification and preapproval differ: prequalification estimates loan amount based on your data, while preapproval involves verification of data and issuing a formal approval. Key categories considered are employment, income, credit, and assets. To secure a home loan, choose a reliable lender, and know your financial status. Quicken Loans, Rocket Mortgage, Veterans United, and Credible are popular options.