It all started in July 2008, when my blog, Good Financial Cents, was born.

I’ve always had a passion for educating people on the basics of investing and financial planning, and I took that excitement to a whole new level with the creation of the blog.

I was fortunate in the sense that I had recently gone independent, and after some convincing, my new brokerage firm allowed me to start blogging.

What was unfortunate at the time was that I was a Series 7 Registered Representative, which basically meant that I could receive commissions off the sale of certain investment products.

Even though my Series 7 only accounted for a fraction of my overall business, I still fell under full regulation of FINRA (Financial Industry Regulatory).

What does that mean?

Being under full regulation of FINRA essentially means that to publish a blog post, video, or do anything on my site, everything had to be run through my compliance department first.

That meant I would write the article, fax the article along with the submission form to compliance, then wait for the e-mail approval to publish the article, which would take between three and seven business days, print off the approval to keep in our branch file, and then make any changes before publishing.

I had to get approval for every single article I published on my site. At the time that was over 800 articles!

Imagine trying to keep track of that. I promise you it’s not fun.

The process was a nightmare, but after almost a year of doing it this way, my assistant and I perfected the system to the best of our ability. Even at its highest efficiency, though, my assistant and I were spending five to ten hours a week just handling the compliance aspect – and that had nothing to do with actually writing the article, posting the article, polishing the article, and handling anything else on the back end of my website.

What made the blogging aspect even worse was that it was hard to have a voice. My blog articles always had to be “balanced,” and I was forbidden from making remarks such as

“I love the Roth IRA and I think it’s one of the greatest things ever created!”

Rather, I would have to say something like

“I encourage every investor to consider the Roth IRA as part of your investment plan”.

I sound like a freaking politician. Ugh!

Needless to say, running the blog was a time-consuming process when you add in the time to manage compliance issues!

For over two years, I was doing it this way, and strongly envious of my registered investment advisor counterparts who could post to their blog freely because they had dropped their Series 7 securities licenses.

I Ain’t Gonna Lie, I Was Jealous!

Not only was I jealous, I was frustrated. I’m the type of guy where if I wanna say something, I wanna say it. If I wanna do something, I wanna do it. I don’t wanna beg permission to speak. The whole time that I was running my blog this way, that’s what it felt like.

I had to get permission to say what I wanted to say. And that ain’t cool.

What sent me over the edge?

In addition to my blog being heavily monitored and regulated, so was my social media presence. That was Twitter, Facebook, LinkedIn, YouTube, and anything else in the social media space.

When I started on Twitter, I had to get my Twitter profile approved by compliance. It was approved, and in a conversation I had with my old compliance officer, she told me to

“Just be careful of what you tweet or post on Facebook. As long as you stay within the same guidelines as your blog you should be okay.”

I took her advice to heart, and for the next year plus, I was Tweeting and Facebooking up a storm!

In July 2010, my brokerage firm put out a notice that stated if advisors were going to be on Facebook and Twitter, everything must be pre-approved before being published.

I Read That and Literally Almost Puked.

That couldn’t be right, could it?

To require my Facebook status updates to get pre-approved?

Or if somebody were to message me on Twitter and I wanted to @reply them, I have to submit my response to my compliance department and wait for their approval before I could speak?

No, there’s no way that that’s how it could be, that’s insane!

Unfortunately, it may have been insane, but it was the reality. In a call with my new compliance officer, she revealed to me that my darkest fears were true: all social media communication would have to be pre-approved.

Trying to talk some sense to them, I presented them with the following scenario:

Let’s pretend that it’s Friday evening and that my family and I are going to Applebee’s for dinner, and I want to get on my Facebook page while I’m at dinner to say,

“At Applebee’s with the fam having a great time.”

The pre-approval requirement for social media communication would mean I would have to wait until Monday morning, the next business day, type up that exact Facebook update, fax it off to my compliance department, and then wait three to five business days for them to approve it, and then as long as they approved it – I could publish on my Facebook update about a week after the fact I went to Applebee’s with my family?

Her simple, one–word response was “Yes.”

I felt defeated.

Slightly Emotional

I can’t remember all the emotions that were going through my brain at that point in time, but I assure you none of them were good. I couldn’t believe it.

I wanted to argue. I wanted to yell and scream, but I knew it would get me nowhere. I knew this was a corporate decision and even though they felt they were doing the right thing for their advisors, from my point of view they were absolutely wrong.

*I guess I should say in their defense, they have now released an archiving program that does allow all social media updates to be archived, which then allows their advisors to not tweet or update Facebook without prior approval.

I should also mention at the time of this conversation, I was already doing that. I had already hired an archiving service, paying them $50 a month to archive all my social media content even though they never had advised me to do so, but I thought it would be a wise decision on my part to do it.

It’s Time

When I got off the phone with my compliance officer, I knew it was time. I knew there was no way I could operate in this capacity and still function and still be happy. I 1000% believe that social media and anything online is not just the way of the future, but it is the present – and if I want to continue to grow strategically, then I need to have the free reigns of a traditional entrepreneur. It was time to let loose and start my own RIA (Registered Investment Adviser).

I don’t want to bore you with the details about the research I started to figure out what my options were, but ultimately what needed to be done was to form my own registered investment advisory firm (Which I did: Alliance Wealth Management, LLC). I needed to drop my Series 7, eliminating my ability to earn another commission ever again.

As I mentioned earlier, almost 90% of my business was already fee-based, but I did have a percentage of income that came through commissions that could only be earned if I had a Series 7. In the financial industry, we call this a “trail.”

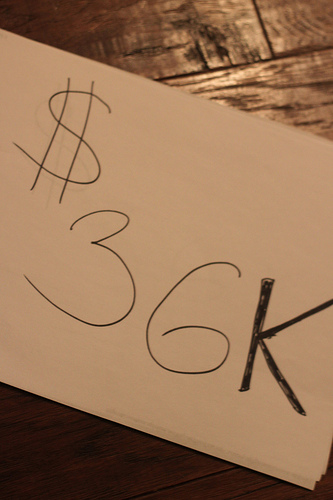

Kiss $36k Goodbye

Based on the trials I was receiving, I was getting ready to give up approximately $36,000 a year gross revenues by making the switch. Before you start thinking I’m a multimillionaire and $36,000 doesn’t mean a lot to me, I assure you it does.

I’ve been building my business for over ten years, and to give up that amount of income just for the sake of getting on Facebook and Twitter was a tough pill to swallow. As you can imagine, it was an even harder pill for my wife to swallow!

It’s not a decision I made overnight, but it’s one that weighed on my heart heavily. I’ve always believed if you have the potential or the capabilities to do what you love, to do what you’re passionate about, to be able to wake up in the morning and go do what your dream is, then you have to go after it.

I knew I would be losing out on a significant amount of income, but I also knew that with the freedom that I’d have forming my own RIA, not only to market my financial planning business but to derive additional income from my blog, I would eventually make up for it.

Was I 100% sure? Absolutely not.

Did I 100% believe in myself? I absolutely do.

So, I pulled the trigger.

I finally made the decision in January of 2011 to just go for it. I knew in my heart it was what I needed to do. To make this transition, I wanted to be sure that I didn’t just give up on the clients I had worked with for years and the relationships I had established just for the sake of my dream. I wanted to make sure that my clients would be taken care of when I made this leap.

The clients I had through the trial part of my business were moved to one of my former partners, who works in the same building as me.

I felt good about this decision and knew this person would take good care of these clients so that I could focus on building my business the way I wanted to.

At the end of the day it was all about freedom. And now have full control of my destiny, and I wouldn’t have it any other way 🙂

Have you ever make a bold step to follow your dream? How big of a chance was it? What finally prompted you to make the move?

I am about to drop my Series 7 as well. What are the compliance requirements for advertising, blogging, etc for an RIA? Are you saying there’s no requirement other than archiving?

Mike

Great article Jeff. I currently hold my series 7 and I plan on taking my series 66 exam in November. The one area I see where I am restricted that is hard for me is that as a personal finance blogger I am not able to make money from affiliate advertising. This hurts. I can not have any income generated from a click-through advertisement. It’s frustrating reading about how much income other bloggers are making through affiliates and I can’t. I have contemplated giving up my licenses, but to be honest I don’t know if I am ready to take that plunge..financially. This gives me hope. Thanks for the article!

Hi Kumiko – I understand your frustration. But you have to weigh out the benefits to you for having the license, versus the ups and downs of blogging income. It takes a lot of effort and even the investment of money to make a real money making blog. And what complicates it is that not all blogs are money makers. That’s why you really have to weigh out if the rewards will be worth the risks.

Jeff, your info is awesome, as well as your delivery with blog and podcast. You are up to date on all the latest new media communications!

Two quick questions…

One, are the blogging/social media constraints still in effect if you blog about non-financial topics (sports)?

Two, as a ten year sales professional almost 40yrs old, I’ve had conflicting advice about jumping into a financial advisor role with a big firm. Some say you have to have big money friends to start or you’re done. Others say you can network to success. Any thoughts?

@Rick I could have blogged about anything other than investments so as long as I didn’t represent the fact I was a financial advisor on the site. But I’ve also heard that many firms don’t want their advisors blogging about anything because of potential risk to their firm.

The big firms don’t care how you get business but you have to produce, period. If you don’t meet certain minimums they’ll end reducing your payout so that it makes it that much difficult to survive.

Hi Jeff…

I agree awesome blog. Keep up the great work & wish you all the best in your practice.

I just want to elaborate on Rick’s first point and ask you — how about blogging about investment advice anonymously or under an alias whilst maintaining the series 7? Would that be a possibility?

I mean I realize the exposure one can get from blogging as a Financial advisor will decrease this way… but by being in compliance with FINRA ($36,000 doesn’t hurt?) and being unbiased about your advice can make one kill two birds with one stone…would that work?

Cheers!

This is a main reason why I stopped my interview with a major company a few weeks ago. They told me I’d have to shut down my blog and stop social media. I almost laughed at the guy, ok I did snicker a bit.

It took you a long time to get established in order to set up your RIA, is there another route besides going though big companies and FINRA?

@ Brent

You can always try to get hired by a larger independent firm, but they often have a structure that resembles much like a law firm; you’re not really building your business, you’re building the firms.

Other than that, there are companies like Primerica and WFG that offer a way in. The only downside is that those companies focus more insurance products initially.

Wow, I had no idea Series 7 bloggers have to go through this. I would have quit too.

I actually just wrote the disclaimer on my own site. It basically says, “my thoughts SHOULD be considered financial advice, and if you plan to sue me or hold me to any regulations because I’m not ‘certified,’ then bring it on.”

Hi Jeff – You’ve got a great blog packed full of great content. I’m an FA with a large wirehouse and don’t have the ability to use social media and blogs as educational and marketing channels and I can say I’m definitely jealous. Can you elaborate more on why dropping your Series 7 and just being an RIA allowed you greater freedom to use social media? Thank you again for the great blog, I’m in the business and I still learn stuff.

@AaronPottichen Thanks for stopping by Aaron. I’d be happy to elaborate. Now that I don’t have the Series 7 and no broker/dealer actually holds my license, they are no longer responsible for me. Essentially, I am responsible, compliance wise, for all my social media efforts now. I archive everything to be compliant as an RIA just as some of the the B/D’s are starting to do. Hope that helps!

@jeffrose@AaronPottichen Coming from the wirehouse world, that just seems to good to be true, but it makes sense. It gives me something to think about. Thank you for the quick reply.

Thanks for sharing it

Fantastic story, thank you! That would have been very frustrating to submit everything! I started my first business in 2002, I gave up my salary from the corporate world. Yet am forever grateful as I also gave up all the politics, endless hours and being at someone else’s whim. Scary yes – worth the freedom – yes!

What a fantastic story — I’m SO happy that you made the decision that you did. Your own personal freedom — to express yourself, to live and speak (and Tweet) the way you want, is worth more than $36K. You’ll make that back in no time, AND you’re free!

Congratulations on taking the plunge, Jeff. I’m about to enter into the same compliance quagmire myself, so am totally with you on all this being quite ridiculous at times.

Congratulations for the great post you have here for us…This is really inspiring…

It’s crazy that people would sensor your Facebook and Twitter updates. I don’t think I would be able to take much of that either. It takes a lot of courage to make the decision you did, and your story is inspirational. Thanks for sharing and for being so brave.

LOVE THIS MAN!!! Way to pour your heart and passion into it! We all got yo back! 😉

Good stuff Jeff! If 10% = $36,000, at least you are making over $300,000 still right? If so, I would totally go solo and get my freedom back!

Best, Sam

Hi Jeff,

I don’t blame you, I would hate having so much boundaries placed around me before I could do something. As far as giving up $36k, I am with you. $36k is $36K and I want to keep as much of my money as possible.

Good decision Jeff. If you haven’t already, you’ll make that $36K back in no time.

Love the story Jeff. It’s really neat to see all the thought that went into the decision and seeing it all play out as things became stricter and stricter. I think ultimately, you made the right decision since you’re doing what you’re most passionate about now, with still plenty of potential when it comes to making up for that $36k!

Jeff, you will do fine! Your content is always awesome and the information you bring is top-notch.

Thanks for showing us all that we don’t have to sit back and live by others rules. Follow your passion and make your life real!

Great decision, Jeff. If you haven’t already, you’ll make that $36K back in no time. Freedom!!!

Wow, very powerful story. I don’t know what my response would be if I were in that situation. This is a testament of the drive and determination you have to do what is both right for you as well as the clients that were affected by your decision. Job well done!

Jeff, I hear you, and understand completely. I gave up a very stable (and good paying) job in the corporate world to pursue my business. It’s tough leaving money on the table, especially when it comes with stability, good hours, and benefits. But I was able to make up the difference by concentrating on growing my business during those hours. Your situation is very similar. You are leaving money on the table, but you have the opportunity to add other revenue streams in the place of what you had to give up. The freedom of that makes it worth it in the end!

Congrats on making the decision to follow your dreams! Best wishes with your new ventures.

You answered one of my questions about non-anonymous financial advisor-bloggers…I always wondered how anyone got away with anything they said!

Does your E&O know you have a blog? does it matter? Would it be prudent to tell them?