Me: “Who helped you select the funds in your 401(k)?“

Client: “Ummm…..I just picked a few options really quick.“

Me: “How much time did you spend researching what you picked?“

Client: “I didn’t.”

Me: <sigh>

This sort of exchange happens more often than it should. What most investors don’t realize is that at some point, your 401(k) will most likely be the largest income-producing asset you own.

Sure your home could be worth more, but; the last time I checked your home doesn’t send you a monthly check when you retire.

There are several reasons why 401(k)s make sense for so many people. But the primary reason you should take advantage of your 401(k) is that once it’s set up there’s nothing much left to do (except the occasional review as I’ll discuss).

Your 401(k) can be automatically funded using your earnings at your job – you won’t have to remember to make contributions.

Table of Contents

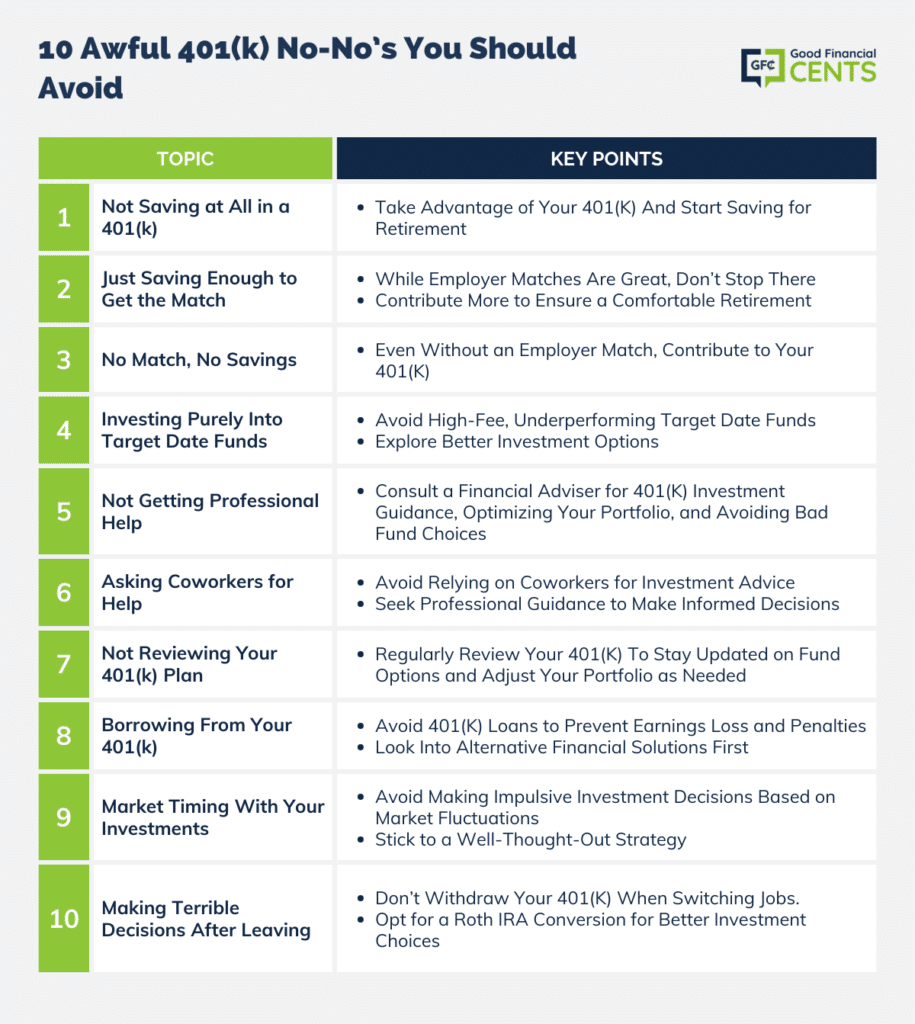

- 1. Not Saving at All in a 401(k)

- 2. Just Saving Enough to Get the Match

- 3. No Match, No Savings

- 4. Investing Purely Into Target Date Funds

- 5. Not Getting Professional Help Choosing Your 401(k) Investments

- 6. Asking Your Coworkers for Help Choosing Your 401(k) Investment Options

- 7. Not Reviewing Your 401(k) Plan Consistently

- 8. Borrowing From Your 401(k)

- 9. Market Timing With Your 401(k) Investments

- 10. Making Terrible 401(k) Decisions When You Leave Your Job

- Bottom Line: 10 Major 401(k) Mistakes to Avoid

However, there are some 401(k) no-nos I think you should avoid. And the sad part is that many people make these mistakes…don’t become one of them.

1. Not Saving at All in a 401(k)

If you have a 401(k) available to you and you haven’t taken advantage of it . . . why not? Again, once you have it set up, there’s not much left to do.

Investing within a 401(k) will help you automatically save for retirement without hardly thinking about it. Before you even have access to your spending money from your paycheck, your 401(k) contribution will be made. Easy peasy.

You need to start investing for retirement. Unless, of course, you like the idea of living on Social Security payments alone (that’s a scary prospect). Even if you’re wealthy, why not save even more for the future?

2. Just Saving Enough to Get the Match

Some employers offer a match up to a certain percentage of your contributions into a 401(k). This is a fantastic benefit you should certainly use – but you shouldn’t stop there.

Chances are you should invest more money into your retirement than what your employer will match in your 401(k). It would be a good idea to research how much money you need to retire and consistently contribute to that amount.

3. No Match, No Savings

Employers are not required to match your 401(k) contributions. If your employer isn’t matching your contributions, should you just skip investing in your 401(k)?

No. Of course not!

Remember, the 401(k) is a great way to automatically make contributions toward retirement. Take advantage of this super easy way to invest your money. It’s still worth it.

4. Investing Purely Into Target Date Funds

To put it lightly, I rather dislike target date funds. Many times, you’ll find target date funds as options within your 401(k).

Target date funds are funds that usually have a year at the end of the name – the year you might like to retire. The idea is that you choose a target date fund that targets the year you’d like to retire, invest in that fund, and watch that portfolio shift from an aggressive strategy to a conservative strategy.

This sounds dandy, but the problem is that the mutual funds within these target-date funds are usually pretty cruddy. How so? Here are two downsides you’ll often see:

- High fees – The mutual funds just have outrageously high fees that are going to take money from you that you could have used to invest.

- Weak performance – The mutual funds do pretty poorly when compared to other mutual funds or market benchmarks.

Taylor Tepper, a contributor for Forbes.com, writes the pros and cons of target funds:

Target date funds offer a simplified investment approach that automatically rebalances asset allocation as investors age, making them especially appealing for younger workers and those seeking ease and diversification.

However, concerns arise from their one-size-fits-all approach, potential higher fees, and a tendency to become overly conservative as investors near retirement.

5. Not Getting Professional Help Choosing Your 401(k) Investments

Okay, so if you’re supposed to pick the investments in your 401(k), how do you know which ones to choose? It’s best to hire a professional.

A good financial adviser can drill down into the specifics of the investments within your 401(k) point out ways to improve your portfolio – and show you which funds you should avoid like the plague.

Don’t go it alone. Get good help and you’ll save more and earn more.

6. Asking Your Coworkers for Help Choosing Your 401(k) Investment Options

I can assure you that most of your coworkers haven’t given much thought to the funds within their 401(k). Get professional help, not the off-the-cuff recommendations of those who don’t live and breathe investments on a day-to-day basis.

Unfortunately, you might find yourself pressured to choose investments within your 401(k) during work when you need to be working, not making decisions about your long-term future.

Instead, spend some free time after work to sit down with a financial adviser who knows their stuff.

7. Not Reviewing Your 401(k) Plan Consistently

While the 401(k) plan is a great way to ensure contributions are made by having them come directly out of your paycheck, that doesn’t mean you can sit back, relax, and forget about your 401(k) altogether.

Should new funds become available within your 401(k), you’ll want to know about them and consider them as potentially better options for your investments. You’ll also want to consider the volatility of your investment mix as you get closer to retirement.

8. Borrowing From Your 401(k)

Borrowing from your 401(k) is definitely a no-no. I say this for two reasons:

- You’ll make less money – Money not invested is money that’s not earning money. Taking money out of your 401(k) defeats the whole reason you put it in there in the first place!

- You might find yourself paying extra penalties and taxes – If you don’t have enough money to pay back your 401(k) loan in time, your unpaid balance will be considered a distribution. That means you’ll be looking at a 10% penalty in addition to higher income taxes.

Erik Brotman, a contributor for Forbes.com, writes:

Borrowing from a 401(k) may seem appealing due to low interest rates and easy access, but it can lead to significant opportunity costs, tax implications, and lost growth potential for retirement savings.

Unless in an absolute emergency, it’s advised to explore other financial options to avoid derailing long-term retirement plans.

9. Market Timing With Your 401(k) Investments

Your 401(k) is a great long-term investment vehicle – but not something you should play around with as the market fluctuates.

Find the right funds with the help of a professional, and reevaluate your funds from time to time, but whatever you do don’t let your emotions dictate your investment decisions.

10. Making Terrible 401(k) Decisions When You Leave Your Job

When you leave your job, whatever you do, don’t cash out your 401(k). Remember those penalties and tax implications if you take a 401(k) loan and don’t pay it back? Well, the same applies here.

However, I would encourage you to consider a Roth IRA conversion with your 401(k) after you leave your job.

Not only will that open up many more investment options than your old employer gave you, but throughout the process, you’ll learn a great deal about how investments work. Note, however, that while it’s worth considering, it’s not always the right thing to do.

Talk with a financial adviser to determine if a Roth IRA conversion is right for you.

401(k)s are a wonderful investment choice as long as you avoid all these no-nos. Do your research, invest with intentionality, and you’ll be just fine.

Bottom Line: 10 Major 401(k) Mistakes to Avoid

Consistent and smart 401(k) investing is crucial for a secure retirement. Neglecting to utilize it, contributing only to employer matches, and avoiding professional guidance can limit growth potential. Target date funds may offer simplicity but often come with higher fees and one-size-fits-all drawbacks.

Regular reviews, resisting borrowing, and staying clear of market timing ensure steady growth. When transitioning jobs, avoid cashing out and contemplate a Roth IRA conversion, but seek expert advice. Ensure you navigate your 401(k) journey wisely, keeping these pitfalls in mind to optimize returns.

This post originally appeared on Forbes.com.

I need to know if it has been 8/9 years since I’ve work , can I draw from it for housing ? I’ve been without a resresidence. Almost the entire time with zero income at this time. Please help me.

Sincerely Geneva Goodman

Hi Geneva – You can take the money but you’ll have to pay ordinary income tax on the withdrawal, plus a 10% penalty if it’s a 401k. The homebuyer exemption only applies to IRAs.

Hi Jeff,

What’s your opinion on investing in your 401(k) when you’re facing quite a bit of debt? Do you prefer your clients go down to the match, hold off all together, or take it case by case?

@ Chris I typically tell people to start investing even if they have debt. For some people that have excessive debt, contributing the max to get the match might be too much. In those cases, I advise they invest something; 1%, 2%, etc.

The logic is they’ll get some experience/exposure to investing and start to learn how it works. By the time they pay off a good chunk of their debt they’ll be able to invest more money with more knowledge and understanding.

As an attorney, it’s very uncommon to ever get an employer match. I never have! That said, I continue to use a 401k (even while I’m paying down my student loan debt)!

I do think borrowing from your 401K can be advantageous in certain situations. I had accumulated some credit card debt. I decided to borrow and pay off that high interest debt. I repaid myself back in six months. While it’s true that your money is not earning money when you remove it, the 401k earns money in the long run so paying it back in a short time frame is key.

i work directly with our 401k program with my company and it is amazing the amount of people who don’t take full advantage. We offer the opportunity to meet with our plan advisors to better understand the offerings and very few take the opportunity. Some don’t even contribute to the match, which only requires 5%.

We just continue to work on education to try and make sure everyone knows how important contributing is to their future.