You know that your credit score is one of the most important bits of financial information about you.

Where you fall on the credit score scale is often considered to be a way of determining what kind of person you are when it comes to managing your money.

Lenders – and plenty of others – use your position on the credit score scale to make decisions about how they will treat you in regard to money matters.

The only problem is that many of us don’t know our credit score. (But we should because it is easy to get our score on sites like freecreditreport.com).

And when you head to one of those websites to get your “free credit score,” it’s really not free, and it’s not your real credit score; it probably makes you pretty frustrated.

I found this out the hard way when I was trying to find my real FICO® Score.

If you’re just as confused as I was, here’s a quick look at determining your credit score scale.

What Is the Credit Score Scale?

Table of Contents

When most of us think of credit scoring, we think of the FICO® Score, put out by the Fair Isaac Corporation.

This credit score ranges between 300 and 850, with 300 representing the lowest possible credit score.

There are also industry-specific FICO variations:

- FICO® Auto Score: 250-900

- FICO® Bankcard Score: 250-900

- FICO® Mortgage Score: 300-850

The point of the credit score scale is to allow lenders and other financial service providers (like insurance agents) to immediately ascertain whether or not you are a credit risk.

If you have a low credit score, then service providers, like cell phone companies – and even a potential employer – might make assumptions that your level of financial responsibility is low and that you might prove irresponsible in other areas as well.

Clearly, lenders view a low credit score as something that increases the chance that they won’t be repaid the money they lend.

FICO® uses the following formula breakdown to determine your position on the credit score scale:

- 35% – Payment History on Loans and Credit Cards

- 30% – Current Outstanding Debt and Credit Utilization Ratio

- 15% – Length of Your Credit History

- 10% – Recent Credit Inquiries

- 10% – The Types of Debt/Credit You Have

Even though lenders see your credit score as a big piece of the puzzle, they may also look at other items – such as your income and your employment history – when making a decision.

However, it is important to realize that the FICO score is not the only credit score available.

Other companies use variations of FICO’s formula to create their own scores and some that have created their own credit score scale altogether. However, for the most part, you are likely to run into some version of credit scoring that uses a model similar to the FICO® Score.

(Non-FICO® Scores are commonly referred to as FAKO scores, but they can have some use, which I’ll explain in a moment.)

All Credit Scores Are Not Created Equal: FICO® vs FAKO Scores

FICO®

Your FICO® Score is the one that everyone wants to know: home mortgage lenders, the car loan officer at your credit union, and even your car insurance company look at some variation of your FICO® Score. Unfortunately, you have to purchase access to your FICO® Score from myFICO unless you apply for a loan and can get the lender to tell you what your score was.

For this reason, we can say that your FICO score is your real credit score – the only one that will count for lending purposes.

FICO scoring is used by each of the three credit repositories – Experian, Equifax, and TransUnion – though each has an internal “brand name” for its own version. There are no significant differences between each of the three versions, if there are any differences in all.

Though there can be substantial differences in credit scores from each of the three repositories, this usually owes either to timing differences in the reporting of information by individual creditors or the fact that creditors may not report to all three repositories.

Are you still confused? It only gets worse from here!

FAKO

FAKO refers to any credit scores that are not FICO.

Vantage Scores are among the most popular FAKO scores. They represent a partnership among the three credit bureaus and include:

- TransRisk from TransUnion (scored on a 300 to 850 point scale),

- Score Card from Equifax (280 to 850), and

- ScorexPLUS from Equifax (330 to 830)

While the scores generally track actual FICO scores, they won’t be an exact match. However, having access to these scores will at least enable you to have a general idea of what is going on with your FICO scores. Significant increases or declines in your

Vantage Scores can tip you off that you are either heading in the right direction or that you have some credit issues you need to take care of.

Other FAKO scores

The explosion in “free credit score” providers has increased the number of options based primarily on FAKO variants. Though subscribing to these services will enable you to see the ups and downs in your scores, it is important to understand that these are not the credit scores used by lenders.

Not only are the scores not real, but they’re not necessarily free either. Most of them will enable you to get your score on a regular basis if you subscribe to their service.

Examples include FreeCreditReport.com, CreditKarma.com, and CreditSesame.com.

Each uses a different scoring source, which may even be legitimate. For example, FreeCreditReport’s credit score comes from Experian. Though that may be only one of the three credit repositories lenders use, the score you will get will be accurate – at least as far as Experian goes. You can also get your free credit score directly from experian.com.

Once again, if you’re concerned with the relative level of your credit score, any of these FAKO sources can help you stay on top of that. Just remember that whatever credit score you get from these sources is unlikely to be your actual credit score for borrowing purposes.

The Danger of Relying on FAKO Credit Scores

There is a general consensus that the scores you get from FAKO sources are calculated on the high side. They tend to be higher than what your actual FICO scores are – sometimes as much as 100 points higher. This can create serious problems if you are about to apply for a loan based on your knowledge of an FAKO credit score.

Let’s say the lender requires a minimum score of 680 in order to make a loan. Armed with your FAKO score of 720, you may go into the application confidently, reasoning that you have excellent credit. But when the lender pulls your actual FICO score, it comes back at 655.

Is it possible that FAKO credit scores might be intentionally inflated in an attempt to draw more consumers to free credit score schemes? As the saying goes, you’ll win more bees with honey than with vinegar. Maybe the extra 30 to 100 points that FAKO scores typically have is the “honey” of free credit score offers. I’m just sayin’…

What Is a Good Credit Score Range?

For the most part, a good FICO® Score depends on the current market conditions. Prior to the financial crisis, a 680 was considered good enough to get a good interest rate on many loans. Now, many lenders want to see a score of at least 720 to offer you the best deal.

| ACCORDING TO FICO® | ||

|---|---|---|

| Excellent | 800+ | Well Above Average and an Exceptional Borrower. |

| Very Good | 740-799 | Above Average and Very Dependable Borrower. |

| Good | 670-739 | Average Borrower (Hint: Sweet Spot Is 720+ for Most Loans) |

| Fair | 580-669 | Below Average Borrower |

| Poor | <580 | Well Below Average and a Risky Borrower |

Some won’t have a problem with you when you have a score of between 620 and 700, but you probably won’t be offered the best terms. If you score between 650 and 699, you are considered to be in the fair to good range. Generally, though, a credit score below 600 is considered quite poor.

A good credit score can mean more than just a good interest rate on a loan: it can also lead to lower insurance premiums and the ability to qualify to move into a better rental.

A good FAKO credit score varies based on the score you are using. Each score has its own scale, which can make comparing it to a FICO® Score challenging. It still holds true that the higher the number, the better your score is. Most of the FAKO credit scores will show you their version of your credit score on a scale in order to show where you fall in the range of poor to excellent credit.

If you’re wondering what all those “credit numbers” mean, that’s okay. Most people don’t understand what FICO scores ACTUALLY mean. At first, I had problems deciphering those numbers and determining what my true FICO score was, but it’s easier than you might assume.

How to Monitor Your Credit Score

So I’ve convinced you that keeping track of this number is important? Great!

I bet you’re thinking: “But wait . . . what exactly is the best way to track my credit?“

Don’t worry. I’m going to make this as easy as possible for you.

Resource #1: MyFico

MyFico is a really nice resource for someone looking to get both their credit score and reports. For $19.95, they will give you your credit report and real Fico score. This is a monthly subscription with no contract, so you will need to cancel within the first month in order to not be charged an additional $19.95.

If you decide to keep the service, then you will receive credit monitoring and $1 million in identity theft insurance.

Resource #2: FreeCreditReport.com

Getting a copy of your credit report used to be difficult. Now, it is as easy as a few clicks of your browser. I go into in-depth details in my review of FreeCreditReport.com.

This is just your credit report. When you log in, you won’t be able to see your full credit score. However, this is a great starting point because you can look for errors or unfamiliar accounts that might indicate identity theft.

Note: You get one free report from each bureau every year. You do not – and should not – have to get all three free reports at the same time. The best strategy is to check only one report from one bureau every four months. You can check TransUnion today, Experian in four months, and Equifax in eight months. This gives you a very basic version of credit monitoring. And don’t worry; the bureaus are required to talk to each other if something happens on your report, so you’ll have updated information no matter which bureau you are pulling from.

Resource #3: Companies That Monitor FAKO Scores for You

With so many popular FAKO credit scores out there, it can be difficult to keep tabs on them. Yet having a snapshot of the ups and downs of your credit report – even if it isn’t a FICO® Score that a lender will look at – is a good thing.

My two favorite companies to track my scores are Credit Karma and Credit Sesame. Each company will track a credit score for you absolutely free. Unlike other websites that say they are “free” but hit you with monthly membership fees, Credit Karma and Credit Sesame are both absolutely free. (They make money in other ways, like offering you a better deal on your mortgage or credit card.)

Here’s a quick comparison of the two:

- Both are FREE

- Credit Karma offers access to three different scores: TransUnion’s TransRisk, VantageScore®, and an auto insurer score. Scores can be updated daily.

- Credit Sesame offers access to Experian’s Scorex PLUS(SM) credit score and updates monthly.

Either company is a great place to start, but Credit Karma seems to have more options. Whichever route you go, being able to keep track of the ups and downs of your credit score is a smart financial move. (Or better yet, use both services since they are free and track two different versions of your score each month.)

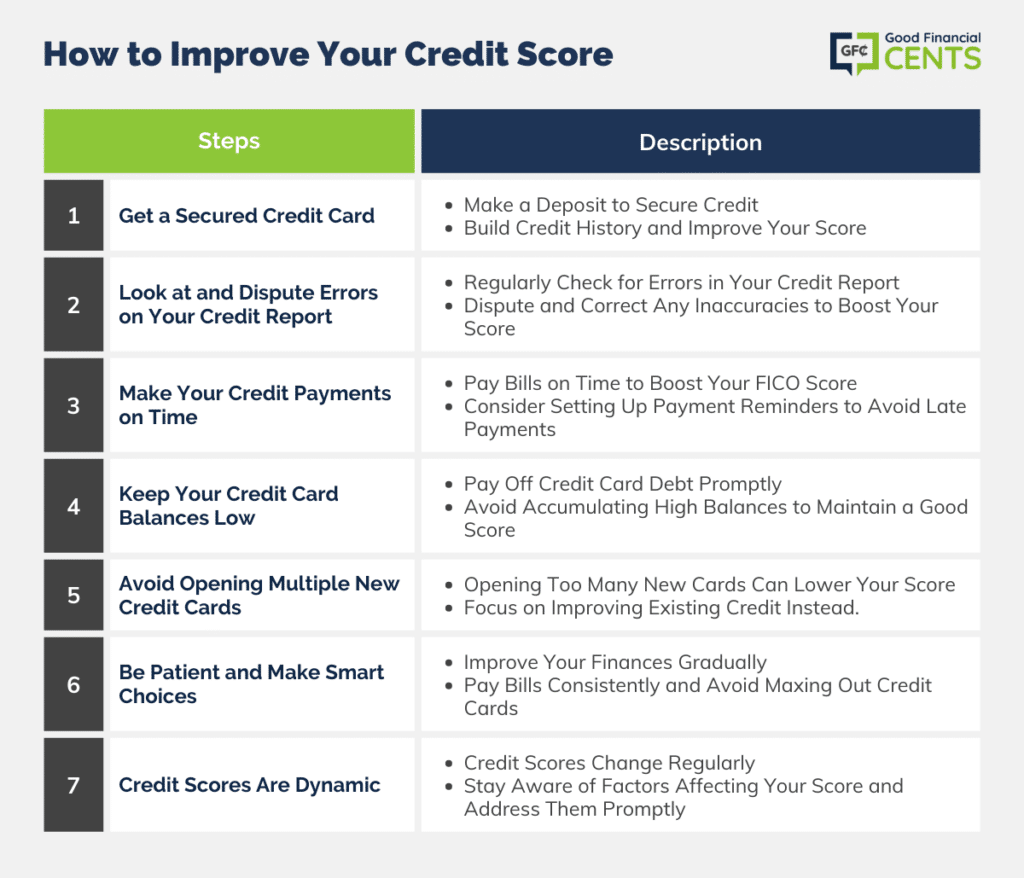

How to Improve Your Credit Score

Okay, if you just checked your credit score and discovered that it stinks, don’t worry . . . there’s hope!

There are a lot of ways you can improve your credit score, and I’m going to show you what works. So don’t freak out. Please.

I would recommend that you make a checklist from this list of tips and systematically check them off as you complete them. Don’t leave anything out. All of these tips may help your situation, so raise your chances of improving your credit score and try them all.

Let’s begin!

1. Get a Secured Credit Card.

A previous intern of mine, Kevin, once had absolutely no clue what his credit score was and had a few lessons to learn.

One of those lessons was that with bad credit, it’s really difficult to get a credit card. In fact, none of the banks he applied with for a credit card allowed him to have one.

But then he got a tip. He was told to get a secured credit card.

A secured credit card has terms that favor the lender much more than the borrower, but the results were astounding.

Kevin, in an article he wrote for GoodFinancialCents.com, explained that secured credit cards are like traditional credit cards, except you have to make a deposit. That deposit is usually the same as your credit limit.

Whoa. Wait a minute. Isn’t that money you can just spend?

No, it’s money that is on deposit should you default on the secured credit card. Now the “secured” part makes sense, doesn’t it?

There are some other details regarding secured credit cards, but for the most part, it’s a great way to build up your credit history – and thus help your credit score.

Using this method and making other smart choices, Kevin showed us how it’s possible to raise a credit score by over 110 points in less than five months.

2. Look At and Dispute Errors on Your Credit Report.

Remember how I showed you how you can look up your credit report earlier in the article? I showed you because it’s important to regularly check your credit report for errors.

These errors can actually be disputed with the credit bureau, so if you do find an error, take advantage of the opportunity to have them correct it.

Sometimes, it’s these errors that are lowering credit scores, so resolving these errors may lead to a better credit score. However, errors are probably not as common as you might hope if you have a poor credit score, so while it’s good to check for errors, don’t give your hopes up thinking this is the best solution for you.

3. Make Your Credit Payments on Time.

This is a huge part of your credit score. Remember, I said above that payment history has to do with 35% of your FICO® Score, so make sure you always pay on time.

How do you do that? Well, there are a couple of techniques.

YouNeedABudget.com believes you should “age your money.” A practical way to do this is to spend this month’s income next month (or spend last month’s income this month, either way).

How can this help you? Well . . . .

If you’ve ever been in a situation where you can’t pay a bill because you didn’t have the money available to you yet (let’s say you get paid on the 15th, but the bill comes on the 12th), you can probably immediately see how this will help you.

By having a money buffer (spending your income much later than you receive it), you’ll be able to make your credit payments when they are due.

But there’s another reason why people don’t make their credit payments: they simply forget!

That’s why it’s a good idea to set up a reminder system to ensure you can’t forget about the bills you have to pay. Do you really think you can remember all of those bills? Of course not! Make sure to have a system in place that works for you.

If you still can’t make your credit payments on time, talk with your creditors to see if you can work out a deal. Perhaps you can lower your payments. Perhaps you can change the payment date. Try whatever you reasonably can to work out a deal so you can start paying on time and transition into good standing with the institutions.

4. Keep Your Credit Card Balances on the Down Low. Literally.

If you have a lot of outstanding debt, that can negatively affect your credit score. Besides, it’s pretty stressful anyway!

One way to keep your credit card balances low is to pay off your debt in a timely manner. Don’t rack up credit card debt. Make sure when you spend money with a credit card, you can actually pay it off at the end of your billing cycle.

Are you taking notes? You should be!

Listen, credit card debt – especially credit card debt that has gotten out of control – can feel pretty crushing. If you’re going to use credit cards, use them responsibly (yes, sort of like alcohol).

Also, I have a lot of articles regarding getting out of debt. Find a few articles relevant to your situation and make a determined effort to reduce your debt as much as possible.

5. Don’t Increase Your Available Credit by Opening a Bunch of New Cards.

You might think to yourself: “You know, if I open up some new cards, I might be able to increase my available credit – thus making what I owe look like peanuts.”

Yeah, it’s a clever idea, but it can actually backfire and lower your credit score. Tricks like these are normally accounted for in the calculation, so thinking that you can fool your way through the system is a bad idea.

6. Be Smart and Take Things Slow and Steady.

Yeah, there are some pretty fast ways to raise your credit score. But you know what? The best strategy is to just make smart choices and take things slow and steady.

By improving your finances as a whole and making sure you don’t entirely avoid the use of credit, you can get – and maintain – a great credit score.

You see, you need to approach the problem of your poor credit score from a long-term perspective. You might not have the stellar results that Kevin, my former intern, achieved. That’s okay!

Let’s do a quick review of FICO® Score factors that matter (and how they are weighted) . . . .

These make up the majority of the factors. So, as you can see, these are largely linked to behaving properly with credit – paying properly and not maxing out your credit cards (for example).

The length of your credit history (15%) is something you really can’t do anything about (unless you don’t have a credit history yet and need to start one). Recent credit inquiries might be something you can affect going forward, but it’s not a huge part of your FICO® Score (at 10%). And, the types of debt/credit you have count for a measly 10% as well.

There are a lot of consumers who are worried about checking their credit score because of the damage it does to their score. When you’re checking your score, it’s not going to hurt your score; it’s the difference between a hard pull and a soft pull.

7. Remember, Credit Scores Are a Moving Target

This point alone makes a compelling reason for staying on top of your credit scores on a regular basis. Your credit score is not a fixed number – it actually changes continuously. It can change day by day, or it could even sit in one place for a month or more. It can rise 20 points one week but fall 80 points the following week.

How does that happen?

Your credit score is a composite calculation of your credit payment history, the amount of debt you have outstanding, the number of credit lines you owe money on, public records information, the type of loans that you have, and even new credit lines you applied for. (Contrary to popular belief, it does not factor in information such as occupation, income, home value, or investment assets owned.)

Each of these items changes on an ongoing basis. For example, if you go to Best Buy and purchase a widescreen TV for $1,000 on your Visa card, the amount of money that you owe will increase. That may drop your credit score a few points.

If you had a late payment on the same Visa card 25 months ago and have had a clean payment history since, your scores may go up a few points because that delinquency is now over 24 months old.

These are just two of the examples of factors that will cause your credit scores to change so quickly and for no reasons, you can ever figure out.

One factor I get frequently asked about is medical bills and how they impact a credit score. If you’ve ever ended up in the ER, you know those bills are massive. It can take a while to chisel them down, but how are they impacting your score until you knock them out? Here is the confusing answer: it depends.

If you have a good credit score today, that does not mean that your score is chiseled in stone. A good credit score today simply means that you have a good credit score today. Tomorrow, next week, next month or next year could bring big changes!

The next time someone asks you, “What’s your credit score?” instead of blurting out the last score you saw, just say, I don’t know – I’ll have to get back with you.”

That will be the most honest answer you can give.

Concluding Thoughts

Where you fall on the credit score scale matters in a few ways.

However, if you have a poor credit score, please don’t let that get you down.

Remember that there is a lot more to financial health than where you land on the credit score scale. While having a good credit score allows you to sign up for more services and get better discounts, it’s not the end of the world if your credit score stinks.

Think about it. You can still buy things. You can still work hard for your money. You can still function in society. While there may be some financial obstacles to overcome with a poor credit score, it’s not going to destroy you.

Let’s highlight two of the key takeaways from this article:

- Monitor Your Credit Report and Score – This will help you understand how you’re doing with your credit score over time, and it will allow you to spot credit report errors so you can correct them (try out MyFico for the most accurate option or spend less money with Credit Karma or Credit Sesame).

- Work to Improve Your Credit Score – You don’t have to settle for a poor credit score. Remember to focus on making your payments on time and try out a secured credit card.

By monitoring and improving your credit score, you’ll discover better access to credit. It’s not always an easy road, but it’s worthwhile. Which steps are you going to take today to get on a better path? Take them!

Great article with facts that can help anyone understand and increase their credit score. Being in good standing on a single loan or credit card is a great start too; but if you’re looking to improve your credit, you’ll need to diversify your profile. Having a mixture of credit cards, student loans, installment loans (i.e. a car loan, personal loan, mortgage, etc.) may help you boost your score. The key is to have different forms of credit that are all in good standing. With that said, opening up 12 new credit cards or getting a loan that you can’t afford is not the trick. For a higher score, you should have a combination of the various forms of credit and debt listed above paired with a history of successful payments!

need experian boost phone number

The lowest I’ve ever seen my score was 819 and the highest was 830. I find it ironic to have such a high score when I have been debt free for 20 years and will never ever borrow again. Just using credit cards for travel and groceries and paying the balance in full is all that you need to stay above 800.

Sounds simple enough but most Americans live paycheck to paycheck, hand to mouth, and need to use their credit cards for auto repairs and medical emergencies. Many use credit cards to pay medical debt, which is the leading cause of bankruptcy. It’s easy to pay for groceries and pay it in full if you have ways and means. Travel? That’s a fantasy for most of us whose wages remain stagnant and haven’t seen a raise in years while the cost of housing, food, transportation and health care skyrockets. Let’s get real. When people get layoffs, they rely on their credit cards to make their car payments and other obligations. We don’t realize how many middle class people, or what’s left of them, are struggling to make ends meet and relying on credit cards to do so.