The following guest post is from Martin of Studenomics. Today, Martin officially launches Next Round’s On Me, where it makes good financial sense to start saving in your 20s so that your older self will thank you.

I graduated college with zero debt and plenty of stories that I’m never going to forget.

That’s a statement I’m very proud of. Now that I’m 27 and a few years removed from school, I constantly thank my younger self for surviving college financially and finding ways to make money in college.

I’m so grateful that I don’t have to worry about making payments on my debt because life’s too short to be broke, and I likely would’ve never gotten involved with personal finance blogging.

Before you dismiss this article by assuming that I’m some dork who missed out on life, you’re incorrect.

I never missed any parties I wanted to attend, I always had a girlfriend in college, and I certainly didn’t stay in playing video games.

I was probably too wild for my own good. The one thing I had going for me was that I was stubborn.

I was determined that I would finish college with no debt so that I could party in my 20s and live life on my own terms.

I came from a poor immigrant family and I never was a fan of the idea of owing money (especially over $20k!).

Table of Contents

How Did I Graduate College With Zero Debt?

It wasn’t easy. I chugged many cups of coffee and almost had a few nervous breakdowns. I even lost a girlfriend and some friends in the process.

I attended a community college first and then I went off to a bigger university in Toronto. I wasn’t much of a scholar to be fully honest. I enrolled in a community college after high school to get my parents off my case.

They had my relatives, family friends, and even neighbors pester me about going to college. So I enrolled just to appease everyone.

The problem was that I was a greedy kid. I didn’t want to spend any time in school. I wanted to work and make money. I didn’t care if the jobs would pay less because I wanted to see my bank account grow.

Then it happened…

When I started the business management program, I actually got into it. I found myself staying after class to ask questions. I was doing well on exams and actually picking up the material.

In high school, I never cared for any of the math or finance courses. I found them to be boring. Now I was the guy who stayed after class to solve additional problems.

The three years flew by in community college. I transferred my credits to Ryerson University in Toronto. I was there for two more years. Three years in community college and two years in university. I earned a community college diploma and a BComm degree.

So technically the process of earning my degree took me a bit longer, but I was able to save money by taking courses at the community college level for much cheaper.

The other hidden benefit was that I used the three years of community college to work like an animal, start blogging, and save up. The workload in community college was lighter and the scheduling was very flexible.

I also appreciated the smaller classrooms because the huge lecture halls would’ve been too intimidating for me at that point.

What Was My Financial Assistance Situation Like?

I was lucky because college in Canada was a lot cheaper. I know that some of my American readers have spent a fortune on college (literally hundreds of thousands).

As a senior in high school, you normally assume that you need student loans. In your teens, you sign your life away pretty much because you’re going to be in debt by tens of thousands of dollars.

The worst part is that you don’t even care in high school. You just sign because you think that college will be worth it. You don’t question anything. You sign the student loan forms and move on with your day.

I never applied for any student loans. I took advantage of free money in the form of scholarships.

Looking back, I wish that I had taken more time to fill out those essays and forms. The forms that I did fill out, helped me receive financial assistance. I had a friend who was a complete whiz with scholarships. She would apply for three scholarships a day and would get back all kinds of free money.

A simple essay could land you free money. Why wasn’t I smarter back then?

I was extremely lucky because my parents also helped me out when they could. They couldn’t give me a free ride, but free rent, free food, and free laundry were pretty sweet.

My parents really wanted me to attend college because I’m the oldest brother and because nobody from my family had graduated from school since my parents were struggling immigrants from Poland.

How Did I Save Money as a Broke College Student?

I saved a lot of money by living at home. I didn’t have to worry about paying bills to survive.

I’ve thanked my parents for this by throwing surprise parties and even sending them to the Bahamas one year. This was huge. I would’ve been buried in debt if I moved away for college.

To save money and pay for tuition, I always held a job in college. I worked construction, started blogging, and even found work on campus (exam invigilator, those guys who catch you cheating!).

I firmly believe that all students should work because it helps you meet people, make money, and figure out how to manage your time so that you’re not on Facebook all day.

Was working in college easy?

Not at all. I often questioned myself and my stubbornness. Some days I was running on fumes and the only thing that kept me going was knowing that I would be debt-free at the end of this journey.

As I mentioned above, I was forced to manage my time ruthlessly and I did rely on coffee a bit too much. I tried to work at least 20 hours a week. I was able to work on the weekends and evenings (depending on how my schedule worked out).

Was working in college worth it?

100%.

If your program is too intense for work, you can always work during the summer months like mad!

You need to be realistic with yourself as a 19-year-old. I thought that I would have no time to study and work. Then I soon figured out that priorities and coffee would trump all. So from 2006-2009, I didn’t watch any shows.

Don’t ask me about anything from pop culture from that time period. The only show that I followed was The Office because it was on Thursdays after class.

If You’re a Student About to Attend College, My Advice to You Is…

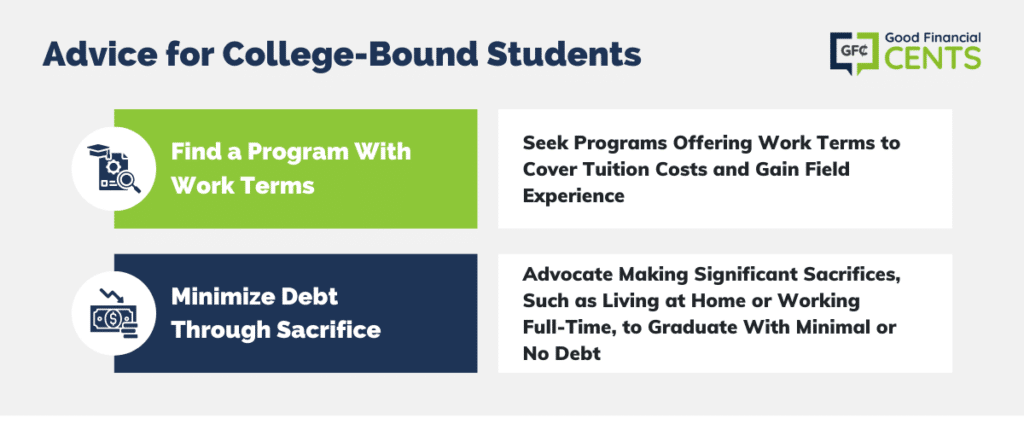

1. Find a Program That Offers Work Terms

Work terms will help you pay for your tuition while you earn experience in your field. My cousin wasn’t the hardest worker in the world and he never held a part-time job.

However, his engineering program forced him to work many work terms. He was fortunate enough to find jobs that would pay him well during these terms.

He would rack up the shifts at work and save up by living like a student. Then when he finished the work term he would have enough money to survive the next semester at college.

How could you go wrong? Experience and money.

2. Earn Your Degree With as Little Debt as Possible by Sacrificing in One Way

Make one huge sacrifice. You could love at home or attempt to work full-time hours.

You have to be ready to do whatever it takes to graduate with zero debt. Your 30-year-old self is depending on you.

Walk to school. Eat cans of tuna. Live at home.

I was the biggest party animal in high school, but I knew that I had to stay in sometimes on a weekend to work or study for an exam. I didn’t want to be in debt. I didn’t want my grades to suffer because falling behind on your GPA costs you money.

Was it worth it?

I promise you that the parties are way better in your mid-to-late-20s. I never had to rush to find a job nor was I stuck making payments on debt that I regretted picking up.

With all of that being said, I did miss out on the growing-up phase of college. I was smart enough to move out after college because I could afford to buy a rental property/residence, but I missed out on the college experience.

I never got to live in a dorm room, worry about finding a place in town, and the stress of dealing with roommates partying full-time.

Was the sacrifice worth it?

For me it was. I didn’t want to be in debt until my 30s like some of my older friends were. That wasn’t the way I wanted to live life.

Realistically, this advice won’t apply to everyone. Not everyone lives in a big city. Not everyone has a supporting family. Not everyone wants to stay at home. Not everyone’s willing to make a major sacrifice when they’re young. I get that. This article is for those of you who want a better life.

I guarantee that you can apply at least one tip from this article to ensure that you graduate college either debt-free or with minimum debt.

Your 27-year-old self will thank you because there’s nothing like backpacking through Europe while your friends are forced to apply for crappy jobs out of necessity.

So instead of figuring out how to get a student loan without a cosigner, go try to figure out how to not get a student loan at all!

Check out Martin’s book Next Round’s On Me, where it makes good financial sense to start saving in your 20s so that your older self will thank you

Final Thoughts – How to Hack College and Graduate With ZERO Debt

Martin’s journey is a testament to the power of strategic financial decisions, hard work, and perseverance.

While your path may differ, the principles of minimizing debt, seeking opportunities for income and experience, managing your time wisely, and making financial sacrifices are universally applicable.

By adopting these strategies, you can pave the way for a more secure financial future and ensure that your older self will indeed thank you.

This article was a great read! I wish I had been able to graduate college without any debt. Unfortunately, no one I knew had ever heard the terms zero debt and college in the same sentence. It has just become an ordinary thing to have extreme amounts of debt for college. No one thinks twice about it. Hopefully more people are exposed to articles like this!

I wish I had read this post many years ago. 😉 I remember actually being on the right track in high school and putting every ounce of effort I could into seeking out scholarships for a period of time. I should have continued doing so, but after a while, I got discouraged and fell into the “I’ll just take out loans, that’s what most people do” trap and now I’m paying for it.

Wow. This post was just wow and so inspirational. As a married woman with a toddler of my own, I know how difficult it is to pay those monthly bills and if you have debt knocking on the door, then life can get pretty tough at times. But this post has allowed me to see that a few sacrifices at that age can go a long way in ensuring that you are debt free and financially stable at a time when you need it the most (like when you have a family to look for). Great advice, will definitely share it with family and friends who still have college to go too.

I worked FULL TIME during college. It was hard, but it was clearly worth it. Stayed at home with my folks, took advantage of any help they provided, studied and also got a great job during college and didn’t have to worry about finding one after graduating. I worked in that industry for 10 years and then founded my own small web design business.

I love your story Ramona. It’s funny how the decade flies by. I can’t believe that I started college ten years ago. I’m glad to see what you followed a similar path. Did you struggle with living with the folks? At times, I wanted to snap!

My folks are amazing and have always been like this. Sure, there were small struggles, as I was trying to act more adult there, but they always were supportive and we usually got along very well. It did help a lot though to have them around, since I could focus only on work and study, while they took care of everything else.

As someone who graduated with $206,000 of student loan debt, I love this post. While I’m down to $134,000 it’s still overwhelming and I have a long road ahead. I encourage anyone starting this journey to take out as little debt as possible – it’s really not worth massive debt.

Sorry to hear about your debt. If you have a plan, you’re going to get out one day. I’m available if you have any questions.

Very solid advice here. Finances in college are a huge challenge nowadays, but there’s a lot of good tips like this to get through with little or no debt if you work hard. Thanks for sharing.

The beauty of the Internet is that you can find anything out within minutes.

I also managed to get creative with the financial aid area. I went to a good school on one of their satellite campuses and commuted. I worked full time 35+ hours a week AND took 14 credit hours towards my bachelors degree. I managed to never have any student debt.

However, where I went wrong was later. I was on top of the world, got married, had a baby, bought a house all by the time I was 25. I also racked up a lot of debt that way. Add in my divorce and I’m still working on paying off the debt. Ugh! SO, I never really had party years. I did have a social life in college in between all of the work. I must have never slept. Oh and in my defense I have a Biology degree, not one in finance so while I did make poor money decisions it wasn’t compounded with the knowledge from business degree courses. I had to learn everything myself, the hard way and after the fact.

You’ve already lived more than most. Good luck with the divorce and everything. The good news is that you can start fresh.

Love this post! I also graduated with zero debt, and you’re right on with suggesting that others who want to do the same need to make one big sacrifice. It’s well worth it to have no loans weighing you down as you try and start your life on your own in the real world.

Well said. That one huge sacrifice will pay off huge in the future. Sure, it sucks in the moment, but it feels amazing to be debt free later on.