Have you recently filed for bankruptcy?

Are you feeling defeated and thinking there is no way you will ever be able to repair your credit?

Recovering from bankruptcy can be challenging both financially and emotionally, but it can be done.

Witnessing both of my parents file for bankruptcy, I’ve seen the struggles that ensue afterward firsthand.

Rebuilding your credit is not easy and can be very challenging.

If you want to improve your credit score, you need to know where you’re starting at. If you don’t know where you’re starting you won’t know how to get to the finish line. Getting your credit score is free and easy, there is nothing to stop you from doing it today.

Start By Checking Your Credit Report >>>

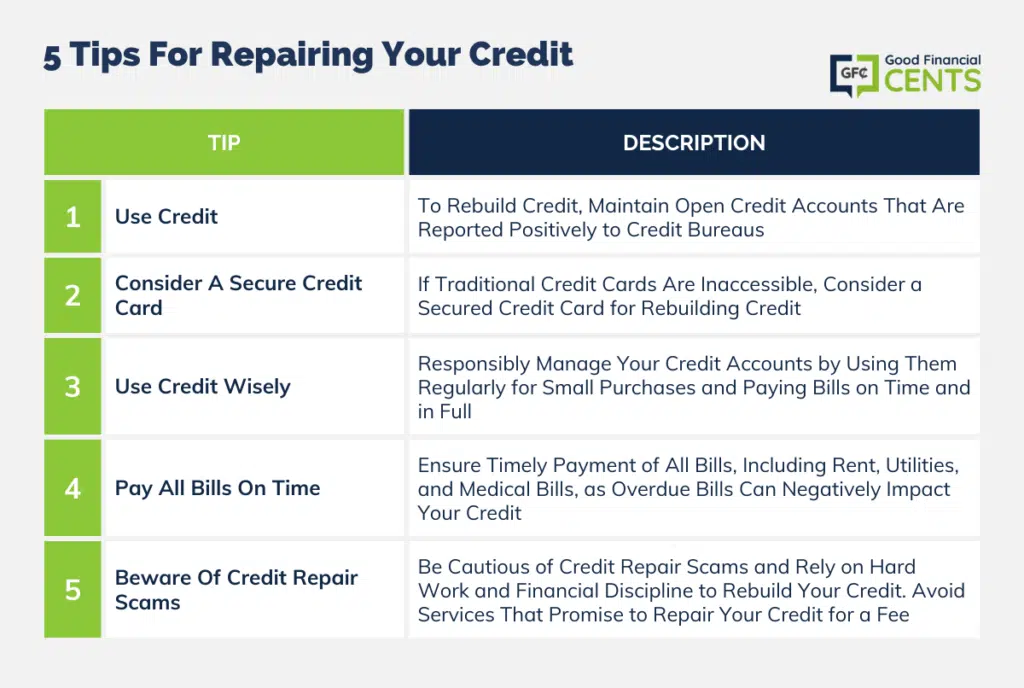

Tips for Repairing Your Credit

If you are willing and able to put in the hard work, become financially disciplined, and know you will need to be in it for the long haul, then you can repair your credit and move to live a financially stable life.

Here is a look at what you will need to do.

1. Use Credit

While many people after bankruptcy may be tempted to switch to just using cash, while smart in some ways, this will not rebuild your credit.

In order for your credit to improve you need to have some type of open credit account or accounts that are being reported to the credit bureaus in good standings each month.

In order to improve your score, you must prove to the credit bureaus that you can manage your accounts.

The only problem is that sometimes it’s hard to get approved. Or if you do get approved, your interest rate is going to be astronomical. I can remember seeing the rates of some of my dad’s cards after his bankruptcy and some were in the high 20% range. Ouch!

Another option is getting a secured credit card. Read below how obtaining a secured card might help.

2. Consider a Secure Credit Card

While you will need to have open active accounts in order to improve your credit, you will find it extremely difficult and more than likely impossible to be approved for a traditional credit card or receive any other loan. Your best bet is probably going to be to get a secured credit card or an offer for those who are specifically made for people with bad credit.

Secured cards require a deposit to open and offer very low limits, but at the same time can be a great tool to start rebuilding your credit. Just be aware that some secure cards do not report to the three major credit bureaus and in order to improve your credit you will need to find one that does report each month.

A previous intern of mine didn’t have “bad credit” per se, he just had no credit history. In some cases, having no credit history is just as bad as having filed for bankruptcy. His credit score was a pathetic 621 and because of it was denied by two banks in trying to open a credit card.

His solution? He opened a secured credit card, used it, and made payments on time. The result was a credit score that raised over 100 points in just 5 months.

3. Use Credit Wisely

As already stated, you will need to have open active credit accounts in order to rebuild your credit, but more importantly, you will need to use these accounts wisely.

First, you will want to make sure that any credit accounts you have are always active. If you have a secure credit card, for example, make sure you use it each and every month to make small purchases that you can truly afford.

You then will need to make sure you are paying your bill every single month, on time and in full. This shows to the credit bureaus that you are being responsible with your accounts and your credit score will start to rebound.

Also, as soon as your credit improves enough to apply for and receive a traditional credit card you should apply for one and switch to using the unsecured card, as this will also help to improve your score.

4. Pay All Bills on Time

You will also want to make sure that you are paying all other bills in full and on time as well. This might include your rent, utility bill, medical bills, etc. Many times these overdue bills are reported to the credit bureaus and you will want to avoid that.

Paying your bills on time probably seems like a pretty simple tip, but it’s one of the most important.

If you want to ensure you don’t miss a payment, take some simple steps, like putting your bills on auto-draft or creating several reminders. Circle it on your calendar. Put notes on your fridge. Set alarms on your smartphone. Do whatever it takes to make sure you pay it on time.

5. Beware of Credit Repair Scams

Finally, you need to know that there is no other way to rebuild your credit other than with hard work and financial discipline. Do not fall for scammers who will try to tell you they can repair your credit for a fee. There are reputable companies like Lexington Law Firm that will help rebuild your credit, but even they have a cost.

A guest post by Damon Day outlined the 10 debt settlement scams to avoid.

It Takes Time, But It’s Worth It

Going through bankruptcy can be hard, both financially and emotionally. It’s not easy to recover from it, and it’s not going to happen overnight. It’s going to take a while. In some cases, it could take A LONG while, but don’t let that discourage you.

It will take a lot of diligence, but it’s well worth the work. Having a good credit score can save you thousands of dollars on interest rates and secure better loans.

Have you had to rebuild your credit after bankruptcy? What challenges did you face in doing so?

Great advice! As a financial professional, I am often consulted by post-bankruptcy consumers looking to rebuild their credit. Many people are tempted like you said to give up and just use cash. Your advice on how to rebuild credit is so vital for post-bankruptcy consumers. Rebuilding credit isn’t as hard as many people think it is. Getting credit cards and paying them off in a timely manner is key to rebuilding credit.

Hey Jeff,

Found your website over at Pat Flyn’s Site (Smart Passive Income) and decided I would stop by and say hello. After checking some of your post here, I can see that you are doing a fantastic job providing quality content for your audience. Keep up the Good work and feel free to stop my blog when you have some time.

Best of luck in your online business.

…..

Casey Gentles