The U.S. Bureau of Labor Statistics estimates that Americans change jobs about 10 times between the ages of 18 and 42.

If job changers had a 401(k) account at just half of those positions, it would represent a significant money management challenge: multiple redundant investment portfolios and a mountain of account statements and investment documentation to sort through.

One flexible solution to simplify the task is to consolidate assets under a single account umbrella via a 401(k) rollover to an IRA.

Offered by many financial institutions, the rollover IRA can help you streamline your investments into a unified asset allocation plan.

REMEMBER:

If you enjoyed this article, be sure to check out:

How to Rollover Your 401k Into a Roth IRA

Consolidate Retirement Assets With a Super IRA

How to Do an In-Service 401k Distribution While You’re Still Working

Table of Contents

401(k) to Rollover IRAs Offer a Wide Range of Benefits

As compared with employer-sponsored retirement accounts, a rollover IRA can provide a broader range of investment choices and greater flexibility for distribution planning.

Consider the following benefits rollover IRAs offer over employer-sponsored plans:

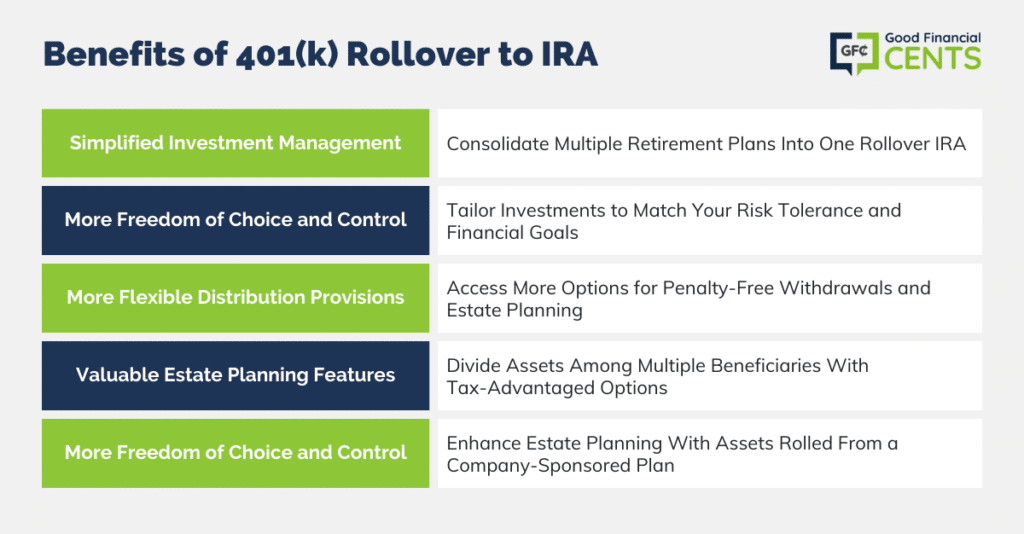

- Simplified Investment Management. You can use a single rollover IRA to consolidate assets from more than one retirement plan.

For example, if you still have money in several different retirement plans sponsored by several different employers, you can transfer all of those assets into one convenient rollover IRA.

- More Freedom of Choice and Control. Using a rollover IRA to manage retirement assets after leaving a job or retiring is a strategy that’s available to everyone.

Depending on the financial institution that provides the rollover IRA, you could have a wide array of investment choices at your disposal to help meet your unique financial goals.

As the IRA account owner, you develop the precise mix of investments that best reflects your own personal risk tolerance, investment philosophy, and financial goals.

- More Flexible Distribution Provisions. While Internal Revenue Service distribution rules for IRAs generally require IRA account holders to wait until age 59½ to make penalty-free withdrawals, there are a variety of provisions to address special circumstances.

These provisions are often broader and easier to exploit than employer plan 401(k) hardship withdrawal rules.

- Valuable Estate Planning Features. IRAs are more useful in estate planning than employer-sponsored plans. IRA assets can generally be divided among multiple beneficiaries, each of whom can make use of planning structures such as the stretch IRA concept to maintain tax-advantaged investment management during their lifetimes.

In addition, IRS rules now allow individuals to roll assets from a company-sponsored retirement account into a Roth IRA, further enhancing the estate planning aspects of an IRA rollover.

By comparison, beneficiary distributions from employer-sponsored plans are generally taken in lump sums as cash payments.

Efficient Rollovers Require Careful Planning

There are two ways to execute a 401(k) Rollover to an IRA — directly or indirectly. It’s important you understand the difference between the two because there could be some tax consequences and additional hurdles if you aren’t careful.

With a direct rollover, the financial institution that runs your former employer’s retirement plan simply transfers the money straight into your new rollover IRA. There are no taxes, penalties, or deadlines for you to worry about.

With an indirect rollover, you personally receive money from your old plan and assume responsibility for depositing that money from the 401(k) into a rollover IRA.

In this instance, you would receive a check representing the value of the assets in your former employer’s plan minus a mandatory 20% federal tax withholding. You can avoid paying taxes and any penalties on an indirect rollover if you deposit the money into a new rollover account within 60 days.

You’ll still have to pay the 20% withholding tax and potential penalties out of your own pocket, but the withholding tax will be credited when you file your regular income tax, and any excess amount will be refunded to you.

If you owe more than 20%, you’ll need to come up with an additional payment when you file your tax return.

Potential Downsides of IRA Rollovers

While there are many advantages to consolidated IRA rollovers, there are some potential drawbacks to keep in mind.

Assets greater than $1 million in an IRA may be taken to satisfy your debts in certain personal bankruptcy scenarios. Assets in an employer-sponsored plan cannot be readily taken in many circumstances.

Also, with a traditional IRA rollover, you must begin taking distributions by April 1 of the year after you reach 72 (73 if you reach age 72 after Dec. 31, 2022) whether or not you continue working, but employer-sponsored plans do not require distributions if you continue working past that age.

The Bottom Line – Consolidate Retirement Accounts With a 401(k) Rollover to IRA

Consolidating retirement assets through a 401(k) rollover to an IRA emerges as a prudent step in managing multiple retirement accounts, particularly as American workers navigate through different jobs during their career span.

A rollover IRA not only simplifies investment management but provides a broader spectrum of investment choices, a higher degree of control over asset allocation, more flexible distribution provisions, and enhanced estate planning features.

While direct rollovers are straightforward, indirect rollovers necessitate careful adherence to rules to avoid tax penalties.

Despite the highlighted benefits, individuals with substantial assets must weigh the potential drawbacks concerning asset protection in personal bankruptcy scenarios.

Given the intricate laws governing retirement assets and taxation, consulting a seasoned financial advisor is advised to tailor a strategy fitting one’s unique financial circumstances and retirement goals.