Early retirement has become a popular financial goal. And well it should be.

Even if you never retire early, just knowing that you can is liberating!

And it may just be the strategy that frees you up to take on even bigger challenges in life.

That can happen when you reach the point where you no longer have to work for a living.

Can You Really Retire at 50?

Table of Contents

- Can You Really Retire at 50?

- Important Considerations if Retiring at 50 Is a Real Goal

- 7 Steps to Retire at 50

- Step 1: Start Saving EARLY!

- Step 2: Save More Than Everyone Else

- Step 3: Invest and Invest Aggressively

- Step 4: Maximize Your Retirement Savings

- Step 5: Set up a Roth IRA Conversion “Ladder”

- Step 6: Live Beneath Your Means

- Step 7: Stay Out of Debt

- Yes, You Can Retire at 50

- Retiring at 50 – The Ultimate Guide

- What Investments Should I Consider if I Want to Retire at 50?

- The Bottom Line – How to Retire at 50 in 7 Easy Steps

It’s a big bold claim – retire at 50? Yeah, sure. A lot of people out there dream of early retirement – who wouldn’t love to hang up the office keys and jump off the 9-5 train sooner rather than later?

But while it’s possible to retire at 50 and have plenty of time left in life to have new experiences, it takes careful planning and a will of steel.

You’ll need to carefully manage your budget, invest in efficient high-yielding assets, and review the numbers regularly so you can work towards retiring at a reasonable age without sacrificing your lifestyle along the way.

So if you’ve got ambition and self-discipline, maybe you really can retire at 50!

Important Considerations if Retiring at 50 Is a Real Goal

If you want to retire at 50, there are some important considerations to take into account.

For starters, you’ll need a good grasp of money. That means understanding the stock market, planning for debt and savings, and investing in yourself through education or entrepreneurial ventures.

Just as important is managing your health – after all, no one wants to retire only to have their retirement cut short! Make sure you’re exercising regularly and eating a balanced diet.

And lastly, it never hurts to start visualizing what you want your life post-retirement to look like. It could be travel, starting up a business from home, or simply spending more quality time with loved ones.

When I was working with retirees, I would often ask them to share what a perfect day would look like for them in retirement. It really helps paint a clear picture of your future expectations for the next chapter in your life.

Whatever it is that lights your fire in the present moment will be a huge influence for not only deciding when you’re ready for retirement but how you plan on approaching that retirement once it’s here.

Looks now look at the 7 steps needed to retire at 50..

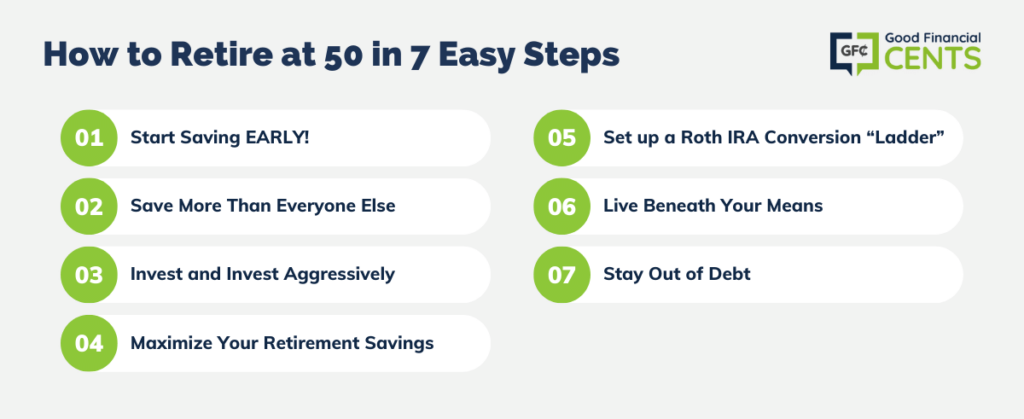

7 Steps to Retire at 50

2. Save More than Everyone Else

3. Invest and Invest Aggressively

4. Maximize Your Retirement Savings

5. Set up a Roth Conversion “Ladder”

There are all different ages that people want to retire at, and for most people, it’s probably something like as soon as possible! But let’s focus on how to retire at 50 since it’s a doable goal for a lot of people.

How can you make it happen?

Step 1: Start Saving EARLY!

If you’re 25 right now, then you should start saving to retire at 50 now – as in immediately. The best way to prove the point is with a couple of examples.

If you decide to put off saving to retire at 50 for another five years – when you are 30 – and you begin saving $10,000 per year, invested at an average annual rate of return of 7%, then by the time you’re 50 you will have $425,341.

But if instead, you decide to start saving right now – again, $10,000 per year, invested at an average annual rate of 7% – then by the time you are 50, you will have $656,227 saved.

That’s a difference of more than $230,000, just for beginning to save and invest five years sooner.

Step 2: Save More Than Everyone Else

It’s a common belief that you can retire just by saving 10% or 15% of your annual income. And that may be true, if you plan to retire at 55 or even 60, and have 35 or 40 years to save and invest money.

But if you’re serious about retiring at 50, you’re going to have to save more than anyone else. That might mean saving 20% of your income, or maybe 25% or even 30%.

Heck, if you’re much older than 25 or 30, you’ll have to save between 40% and 50% of your income if you hope to retire at 50.

What You Can Do Is Start Out Saving 20%.

But each time you get a pay raise or promotion with an even bigger pay raise, instead of spending the extra money, commit it to savings. After a few years of steady pay increases, you should be able to increase your savings rate to 30% or even more.

Saving such a large percentage of your income accomplishes two very important goals:

1. It obviously enables you to reach your savings goals faster

2. But just as important, it conditions you to living on less money than you earn

That second point will be really important when you actually do retire. The less money that you need to live on, the sooner and more effectively you’ll be able to retire.

Step 3: Invest and Invest Aggressively

I probably don’t have to tell you that you’re not going to be able to retire at 50 by investing in interest-bearing assets, like certificates of deposit. Interest rates of 1% per year or less just won’t cut it.

You’ll have to invest in stocks, and that’s where the great majority of your money will need to be invested at all times. The stock market has returned an average of between 9% and 11% over the past 90 years and that’s the kind of growth that you’ll need to tap into if you want to retire at 50.

Since you’re probably well under 50 now, you can afford to keep 80% to 90% of your savings invested in stocks. That’s the best way to get the kind of return on your investments that you’ll need to build the kind of portfolio you’ll need to make early retirement a reality.

All the rewards of aggressive investing come with some risk, so you want to make sure you invest with a solid platform.

Here are my top picks for all of you bold investors itching for early retirement:

- Ally Invest: With Ally Invest, you can opt for do-it-yourself investing or professional account management with Ally’s robo-advisor. Ally starts out by helping you establish your risk tolerance, where you can opt for “Aggressive growth” and put the majority of your investments into stocks.

Ally Invest offers some of the lowest trading fees on the market, 24/7 customer service, and professionally managed portfolios to meet your investment goals. Try Ally Invest today.

- Betterment: Betterment offers investors an alternative robo-advising experience, completely automating your investment experience. The software maximizes your returns with tax loss harvesting and helps you reach your specific retirement goals with RetireGuide.

The service automatically rebalances your portfolio to keep you on track to your goals. With a low annual management fee and no trade fees, you can start investing with Betterment easily.

- M1 Finance: Rather than assessing risk tolerance, M1 focuses on helping you target your investment goals and stay on track to reaching them. When you invest with M1 Finance, you can choose from 60 expertly designed investment “pies” made of up to 60 ETFs and stocks, or create your own.

M1 then manages your investments, rebalancing your account as needed. M1 gives you fee-free account management and trades, and requires low initial investments, making it a great choice for aggressively investing for early retirement.

Step 4: Maximize Your Retirement Savings

Taxes are one of the underestimated obstacles of early retirement planning. Not only do they reduce the income you have available for savings, but they also take a chunk out of your investment returns.

For example, if you earn 10% on your investments, but you’re in the 30% tax bracket, your net return is only 7%. That will slow your capital accumulation.

But there is a way around that problem, at least partially. You should maximize your tax-sheltered retirement contributions.

Not only will that reduce your taxable income from your job, but it will also shelter the investment earnings in your investment portfolio so that a 10% return will actually be a 10% return.

If your employer offers a 401(k) plan, you should make the maximum contribution you’re allowed to. That would be up to $24,500 per year. If your employer offers a matching contribution, that’s even better.

You should also plan to make contributions to a traditional IRA, even if those contributions won’t be tax deductible due to income limitations. The investment earnings in the account will still accumulate on a tax-deferred basis, and that’s what you want to happen.

Now there is a basic problem with retirement savings, at least in regard to early retirement. If you begin taking withdrawals from your retirement accounts before you reach age 59 ½ you will not only be subject to income taxes on the withdrawals but also the 10% early withdrawal penalty as well.

But there’s a way around that dilemma – it’s the Roth IRA.

Step 5: Set up a Roth IRA Conversion “Ladder”

You don’t have to contribute to a Roth IRA every year in order to get the benefits of the Roth IRA. You can set it up by doing a Roth conversion from other retirement accounts, such as a 401(k) plan and a traditional IRA.

(That’s another big reason why you should always max out your retirement savings, especially if you want to retire at 50).

Roth IRAs enable you to take tax-free withdrawals from the plan once you reach age 59 ½, and have been in the plan for at least five years.

How Does That Help You if You Want to Retire at 50?

Roth IRAs Have a Loophole. Contributions to a Roth can be withdrawn free from taxes and the early withdrawal penalty.

After all, since there were no tax savings going in, there was no tax liability going out.

(Taxes and penalties, however, do apply to the earnings from the account, however, the contribution withdrawal rules don’t require a pro-ration between contributions and earnings the way traditional IRA withdrawals do.)

That contribution withdrawal loophole makes the Roth IRA perfect for early retirement. You can make this happen by doing a series of annual Roth IRA conversions from your other retirement accounts.

Are you with me so far?

There is one difference between contribution withdrawals from a regular Roth IRA and a Roth conversion. Since you are not making direct contributions with Roth conversions, but rather converting balances from other accounts, the IRS has a five-year rule on early withdrawals.

Roth IRA 5 Year Rule

At least five years must pass between the time a balance is converted and it’s withdrawn from the account. If it’s withdrawn sooner, it’s still not subject to ordinary income tax, but it will be subject to the 10% early withdrawal penalty.

You can avoid this by making a series of annual conversions to a Roth IRA, in what is known as a Roth conversion ladder.

Basically, what you do is decide how much money you will need to live on when you retire, and then convert that amount each year for five years.

As long as you stay five years ahead, you will always have a sufficient amount of Roth funds to live on, and you can withdraw them free of both income taxes and penalties.

| EXAMPLE: Let’s assume that you need $40,000 per year in order to live on in retirement at age 50. You have several hundred thousand dollars in your 401(k) plan, so five years from now (in 2022), beginning at age 45 you start making annual conversions to your Roth IRA of $40,000. Once you turn 50 (in 2027), you can begin taking those withdrawals from the Roth IRA each year, free from taxes and penalties. |

To illustrate, your Roth conversion ladder will look like this 🙂

| YEAR | AGE | AMOUNT OF ROTH CONVERSION | AMOUNT OF ROTH WITHDRAWAL | SOURCE OF FUNDS WITHDRAWN |

| 2022 | 39 | 40,000 | 0 | N/A |

| 2023 | 40 | 40,000 | 0 | N/A |

| 2024 | 41 | 40,000 | 0 | N/A |

| 2025 | 42 | 40,000 | 0 | N/A |

| 2026 | 43 | 40,000 | 0 | N/A |

| 2027 | 44 | 40,000 | 40,000 | 2022 Conversion |

| 2028 | 45 | 40,000 | 40,000 | 2023 Conversion |

| 2029 | 46 | 40,000 | 40,000 | 2024 Conversion |

| 2030 | 47 | 40,000 | 40,000 | 2025 Conversion |

| 2031 | 48 | 40,000 | 40,000 | 2026 Conversion |

The Roth conversion ladder will enable you to make early withdrawals from your Roth account until you are 59 ½ and can begin making penalty-free withdrawals for your non-Roth retirement accounts. It will also prevent you from having to draw down non-retirement accounts.

There is one downside to the Roth conversion ladder, which is a problem with all forms of Roth conversions, and that’s that you will have to pay regular income tax on the number of retirement assets converted to a Roth IRA.

But that may be a price worth paying if it means you’ll be able to have a generous early retirement income to go with that early retirement.

Step 6: Live Beneath Your Means

One financial habit you’ll have to get into is to live beneath your means. That means that if you earn a dollar after taxes, you’ll have to live on say, 70 cents, and bank the rest.

That’s not an easy pattern to get into if you’ve never done it before, but it’s absolutely necessary. Unless you can master it then early retirement will be nothing more than a pipe dream.

In order to live beneath your means you’ll have to adopt a few strategies:

- Keep your basic living expenses low, especially your housing expense

- Drive an older car, one that isn’t expensive and doesn’t require you to go into debt

- Be proactive about finding bargains on whatever you buy – food, clothing, repairs, insurance, etc.

- Be conservative with entertainment, including and especially with vacations and traveling – early retirement planning and the good life don’t mix well

- Avoid eating out all the time – it’s a slow way to torpedo your long-term plans

Any money that isn’t going into living expenses is more money for savings.

Step 7: Stay Out of Debt

A word of warning about debt: it can undo everything you’re trying to accomplish in order to retire at 50.

It will do you little good if you reach 50 and have $500,000 saved, but $100,000 in debt of various types (it’s easier to get to that level than you think – just live the TV version of the suburban lifestyle and it’ll happen all by itself!).

Not only does debt weaken your net worth, but it also comes with monthly payments. And you’ll need as few of those as possible if you’re going to retire at 50.

Better yet, the goal should be to be debt-free entirely.

Debt not only raises the cost of living in retirement, but it will reduce the amount of income you’ll have to dedicate to savings between now and then.

Being debt-free should include your mortgage if you own your own home or plan to. Your early retirement plan should include a sub-plan to pay off your mortgage in time for your retirement date.

Nothing goes better with early retirement than a mortgage-free house!

Yes, You Can Retire at 50

As you can see, if you really want to retire at 50 you’ll have to adopt a multi-strategy plan to make it happen. It’s mostly about saving a lot of money and investing it well, but there are a lot of factors that will make that challenge more doable.

Make a plan now, and then stick to it religiously, and you’ll be able to retire at 50 – or any other age you choose.

Retiring at 50 – The Ultimate Guide

Retiring at 50 may sound intimidating, but it is a goal that many people can reach with the proper planning. To retire comfortably at 50, it is important to create a retirement plan that takes into account future financial obligations and then start investing early.

Setting realistic goals and analyzing investments on a regular basis can help ensure that you are on track for your retirement goals. Additionally, semi-retirement or “bridge jobs” can provide an option to continue working while still having time for leisure activities.

Review our list of side hustle ideas for options to supplement your income after retirement.

With these strategies, retirees can gain confidence in their ability to achieve financial independence at an earlier age.

What Investments Should I Consider if I Want to Retire at 50?

If you are planning to retire at 50, there are certain investments that you should consider. Long-term investments such as stocks, bonds, ETFs and annuities can provide a steady stream of income over time.

It is important to diversify your portfolio so that you don’t have all your money tied up in one investment.

Additionally, investing in real estate will increase your wealth over time (if you have the stomach for it). It’s also a MUST to have an emergency fund in case of unexpected expenses such as healthcare bills.

Are Annuities a Good Investment if I Want to Retire at 50?

Annuities are a viable investment option for those seeking to retire at 50. They provide a steady stream of income that generally continues even after retirement age.

Annuities can also be tailored to meet an individual’s needs, such as providing a set amount of money each month or lump sum payments at predetermined intervals.

However, the amount of money you get from the annuity is usually based on the amount of money you put into it and can vary depending on the type of annuity chosen.

Be also careful on the type of annuity you purchase. There are so many different annuity options that many investors get confused on which one is best for them.

The Bottom Line – How to Retire at 50 in 7 Easy Steps

The aspiration to retire at 50 is not a mere pipe dream but a feasible objective with the right blend of meticulous planning, disciplined saving, and astute investing.

The liberation that comes with the possibility of early retirement can spur individuals to embrace grander challenges in life.

The outlined 7-step strategy highlights the necessity of commencing savings at an early age, investing aggressively, and cleverly navigating tax shelters to amass a retirement corpus.

While maneuvering a Roth IRA conversion ladder could mitigate tax implications and penalty fees, living beneath one’s means emerges as an imperative practice to fast-track the journey towards a leisurely and financially secure retirement at 50.

The advent of reliable investment platforms like Ally Invest, Betterment, and M1 Finance further facilitates individuals in meticulously crafting and managing their investment portfolios toward achieving this coveted milestone.

Hi, Jeff. Found one of your other discussion threads and then found this one. I am a big fan of letting a Roth IRA do double-duty as retirement and savings (IF the person has sufficient discipline). So I like your suggestion. Good idea to contribute to one, even with just a few hundred dollars,

Ditto for Roth conversions, but would this help your Roth Conversion Ladder? I think the conversion rule requires five CALENDAR years. If I convert on 12/31/20, I can withdraw it on 1/1/2025. So I only have to wait ~4+ years instead of five. How does that sound?

Thanks again for the ideas.

This might seem obvious, but don’t get an alcohol habit later in life. It starts to happen.

Thanks for the great article. How would one deal with health insurance when retiring at 50? Would appreciate any tips on this.

Hi Aaron – That really is an issue. You can try going with a COBRA plan from your employer, but those are expensive and last only 18 months. If your spouse still works, you can stay on her plan, if she’s covered. You can also try a part-time job with health insurance, or look into a Christian health sharing ministry. If all else fails, look into the health insurance exchanges at healthcare.gov. Select the plan with the highest reasonable maximum out-of-pocket, making sure you have enough money in an emergency fund or HSA to cover the out-of-pocket. There are no easy options here, so I’d recommend looking into several to find the one that works best for you.