A major decision in retirement planning is whether to make pre-tax or Roth (after-tax) 401k contributions. Pre-tax contributions go into your retirement account with money that has not been taxed, and then taxes will be paid when the funds are withdrawn in retirement.

With Roth contributions, taxes will be taken from the money prior to placing it in the plan, but it can then be withdrawn tax-free once you retire.

Making the correct decision depends on a few factors, such as your current and expected future income levels, how much of an earning potential you have left before you retire, and also how close you are to retirement age.

When considering all aspects of these two types of contributions it could result in potentially thousands more dollars during retirement, so it’s important to take the time to research each option thoroughly.

Pre-tax and Roth (after-tax) contributions are two different types of contributions that can be made to retirement accounts such as 401(k)s and IRAs.

Pre-tax Contributions:

The advantage of pre-tax contributions is that they lower your taxable income in the current year, which can reduce the amount of taxes you owe.

Roth (after-tax) Contributions:

The advantage of Roth contributions is that the money in the account grows tax-free, and withdrawals in retirement are also tax-free.

Both pre-tax and Roth contributions have their advantages and disadvantages, and the choice between them will depend on your personal financial situation and goals.

Factors to consider include your current tax bracket, your expected tax bracket in retirement, and whether you prefer to pay taxes now or later.

401(k) and Roth 401(k) Contribution Limits

| YEAR | 401(k) MAXIMUM | CATCH-UP CONTRIBUTION | MAXIMUM ALLOCATION |

|---|---|---|---|

| 2024 | $24,500 | $8,000 | $69,000 |

| 2023 | $22,500 | $7,500 | $66,000 |

| 2022 | $20,500 | $6,500 | $61,000 |

| 2021 | $19,500 | $6,500 | $58,000 |

| 2020 | $19,500 | $6,500 | $57,000 |

| 2019 | $19,000 | $6,000 | $56,000 |

Table of Contents

- What Factors Do You Need to Consider to Choose After-Tax vs Pre-tax?

- What Are the Tax Advantages of an Investor Contributing Pre-tax or Roth Contributions to Their 401K if They Are 35 Years Old and Making $100,000 per Year?

- Assuming the Money in the 401K Would Grow at 8% Compounded Annually, What Would the Tax Benefit Be After 30 Years?

- Pros and Cons of Pre-Tax 401k vs Roth Contributions

- The Bottom Line on Pre-tax vs After-Tax Contributions

What Factors Do You Need to Consider to Choose After-Tax vs Pre-tax?

When deciding between after-tax and pre-tax options, there are a few factors to consider.

First, you need to consider your current tax bracket. If you’re in a higher tax bracket, then it might make more sense financially to choose the pre-tax option as it provides additional tax benefits due to being taxed at a lower rate.

Second, if you expect your income or tax rate to increase in the future, then investing in pre-tax accounts may be beneficial since they can defer taxes until withdrawal time when your tax rate is likely higher.

Third, it’s important to think about what type of investments you plan to make and how long you’re willing to wait before withdrawing funds from those investments.

Some investments and retirement accounts have restrictions on when the funds can be withdrawn and penalties for early withdrawals so it’s important to consider these factors as well.

Finally, if you plan to use the invested money for short-term needs such as an emergency fund or home repairs, then after-tax options may be more suitable since they don’t require waiting for certain periods of time before being able to access the funds.

What Are the Tax Advantages of an Investor Contributing Pre-tax or Roth Contributions to Their 401K if They Are 35 Years Old and Making $100,000 per Year?

If an investor is 35 years old and making $100,000 per year, the tax advantages of pre-tax and Roth contributions to their 401(k) will depend on their current tax bracket and their expected tax bracket in retirement.

Pre-tax Contributions:

If an investor is in the 24% tax bracket and contributes $18,000 to their 401(k), their taxable income will be reduced by $18,000, which would result in a tax savings of $4,320.

Roth Contributions:

For example, if an investor contributes $18,000 to a Roth 401(k) account and their income tax rate is 24% this year, they will pay $4,320 in taxes on that $18,000 but if they are in a higher tax bracket in retirement, they will not pay taxes on the withdrawals.

It’s important to note that the above examples are based on current tax laws and tax rates could change in the future and an investor should consult with a tax advisor to understand the tax implications of their contribution decisions.

Additionally, it’s always a good idea to consult with a financial advisor to determine which option is best for you and the best way to balance the tax savings and tax-free withdrawals in retirement.

Assuming the Money in the 401K Would Grow at 8% Compounded Annually, What Would the Tax Benefit Be After 30 Years?

Assuming the money in the 401(k) would grow at 8% compounded annually, the tax benefit of pre-tax and Roth contributions would be different after 30 years.

Pre-tax Contributions:

However, withdrawals from the 401(k) in retirement would be taxed as ordinary income, at the investor’s tax rate at that time. Over 30 years, the account would grow to $3,382,958, but the full amount will be subject to income tax upon withdrawal.

Roth Contributions:

Over 30 years, the account would grow to $3,382,958, and the entire amount would be available to the investor tax-free upon withdrawal.

It’s important to note that these examples assume that the investor continues to contribute the same amount every year and that tax laws and tax rates will remain the same over the next 30 years.

It’s always a good idea to consult with a tax advisor or financial advisor to understand the tax implications of contributions and withdrawals, as well as the best way to balance the tax savings and tax-free withdrawals in retirement.

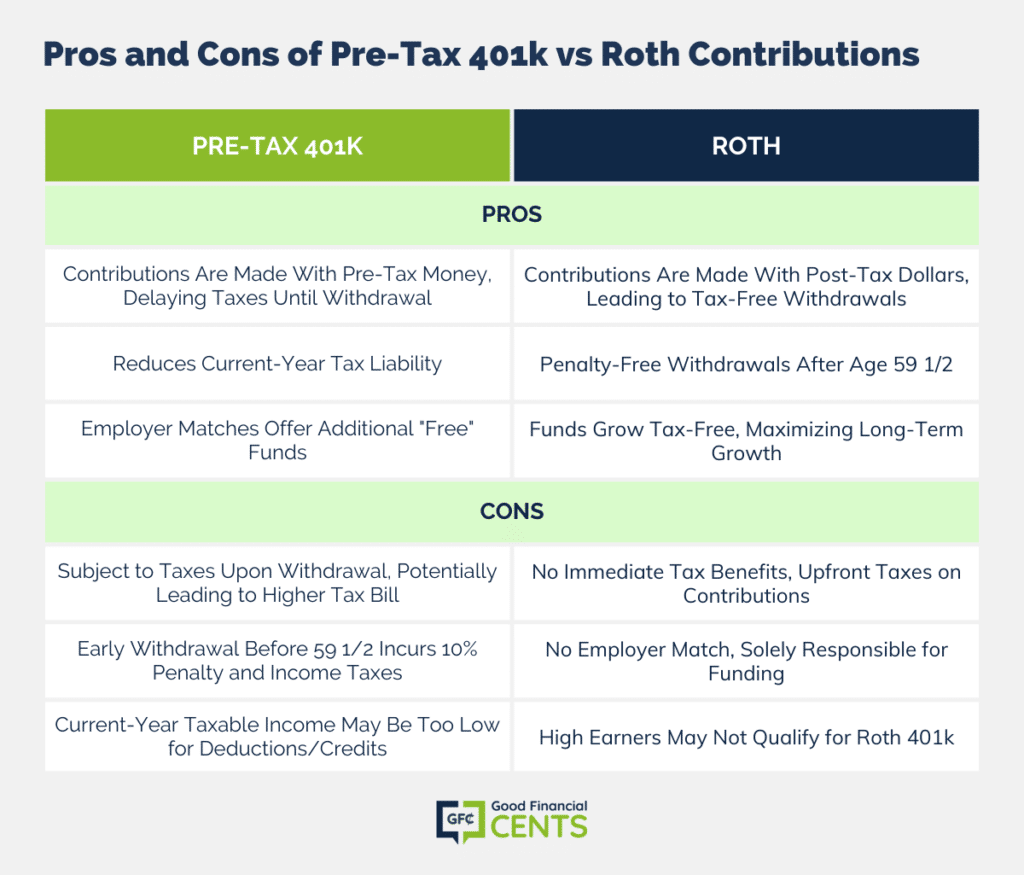

Pros and Cons of Pre-Tax 401k vs Roth Contributions

Pros of Pre-Tax 401k Contributions:

- Contributions are made with pre-tax money, meaning you do not pay taxes on your contributions until you make withdrawals.

- This can reduce your overall tax liability in the current year.

- The employer usually matches a certain percentage of employee contributions, so it is essentially free money that should be taken advantage of.

Cons of Pre-Tax 401k Contributions:

- The money is subject to taxes when withdrawn, which may result in an unexpectedly high tax bill at retirement.

- Withdrawing funds before age 59 1/2 comes with a 10% penalty fee as well as income taxes.

- Your taxable income for the current year might be too low to take full advantage of all available deductions and credits.

Pros of Roth 401k Contributions:

- Contributions are made with post-tax dollars, so there are no taxes due at withdrawal or retirement.

- Withdrawals can be taken out penalty-free after age 59 1/2.

- Funds grow tax-free over time, allowing for maximum long-term growth.

Cons of Roth 401k Contributions:

• You don’t get any immediate tax benefits since you are paying taxes upfront on your contributions.

• There is usually no employer match on contributions, so it’s up to you alone to fund the account.

• In some cases, if you make too much money or have too large a contribution amount, you may not qualify for the Roth 401k option at all.

The Bottom Line on Pre-tax vs After-Tax Contributions

Pre-tax vs. Roth (after-tax) contributions are an important distinction to make when you are planning for retirement.

Pre-tax contributions give you a tax break now, but you will pay taxes on the withdrawals later. Roth contributions require that you pay taxes on the contribution now, but your future withdrawals will be tax-free.

Both types of contributions have their own advantages and disadvantages based on your individual financial situation. It is important to understand both options so you can make the most of your retirement savings.

Consult with a financial planner if you need more guidance on which type of contribution will work best for you.