Have you ever considered buying a vacation property for a short-term rental? I think it’s a pretty common idea. And in a perfect world, it could combine the best of leisure and investing in one property.

I recently received a question from a reader who is considering taking the plunge:

“My wife and I are in our mid-50s, debt-free, and own our home. We would like to have a place that our family and kids could use while we explore future retirement areas near the vacation home.

Most traditional planners and CPAs advise against it, but we’re curious what the Wealth Hacker view is.” – Thanks, Steve

Steve hasn’t asked specifically about the rental potential of the property. But since it’s a common outcome, I decided to include it in the pros and cons of buying a vacation property for short-term rentals. I’ll be addressing Steve’s direct questions as well as the short-term rental aspect.

I’ll start by covering the pros, and then move on to the cons. My hope is that by presenting both, I’ll not only answer Steve’s question but also provide valuable information for other readers considering a vacation home purchase.

Table of Contents

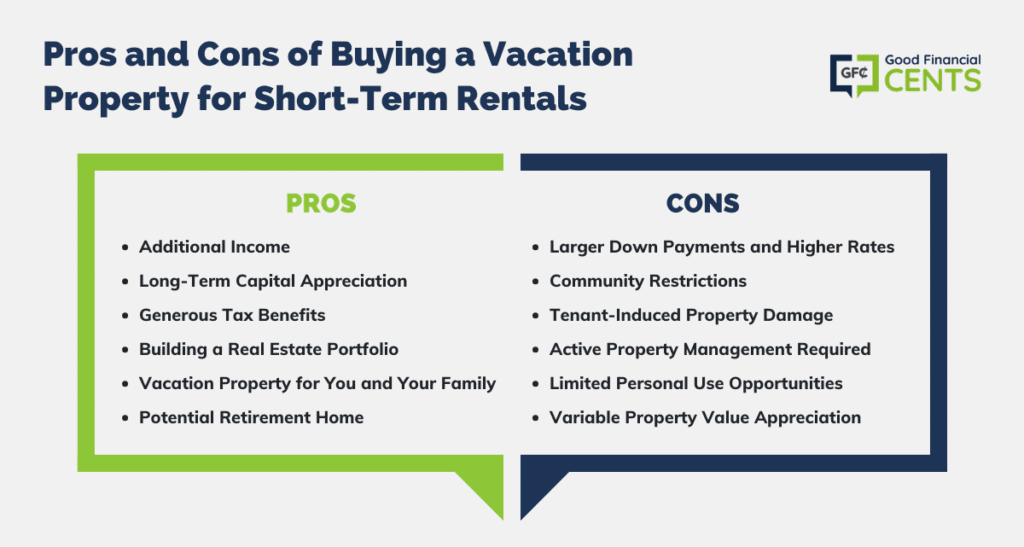

Pros of Buying a Vacation Property for Short-Term Rentals

Without a doubt, there are real advantages to buying a vacation property for short-term rental. But before we get into those, I first want to be clear that we’re talking about these benefits as they relate to vacation property.

Put another way, a vacation property isn’t an investment property, so the benefits will be different.

While an investment property is strictly a money-making venture, a vacation property is something of a hybrid. Much like the house you live in, a vacation property provides personal benefits but has the potential to produce financial gains at the same time.

With that said, let’s move on to the pros of owning a vacation property.

1. You Can Generate Additional Income

If you buy a vacation property strictly for personal use, it’ll add an expense to your budget, and a major one at that. But by renting it out at least part of the time, you can generate some income from the property.

For example, let’s say the payment on your vacation is $1,500 per month. By renting it out one week out of each month, also at $1,500, you’ll cover the cost of keeping the home. But if you rent it out for more than one week each month, the property will generate positive cash flow.

You can also get creative here. You can rent the house out during certain times of the year and keep it strictly for personal use the rest of the year.

Maybe you choose to rent the house out “in season” only. That might mean earning $2,500 per week for the 12 weeks of the peak season. That arrangement will cover the monthly carrying costs for the entire year while producing a $12,000 profit.

Meanwhile, you’ll have the benefit of enjoying your home 40 weeks out of each year. In that way, the house will be an investment property 12 weeks out of the year and a vacation home for the other 40.

2. You Can Earn Long-Term Capital Appreciation

Most people find the house they live in to be one of the best investments they ever made. Even if you don’t view your primary residence as an investment but rather as your home, it can work in both directions.

The house you buy for $400,000 and live in for 20 years may be worth twice as much in the end. That’s a financial win-win of the best kind!

The same thing can happen with a vacation home. You might buy the property for $200,000, then it doubles to $400,000 twenty years later. Along the way, you’ll have enjoyed spending your vacations in the home while also renting it out to generate income.

This is where it’s important to understand the leverage advantage that real estate provides.

Unlike most other investments, real estate is typically purchased primarily using borrowed money. That magnifies your investment returns by a lot.

If you purchased a $200,000 vacation property with a 20% down payment of $40,000 and the value doubled to $400,000, you’ll really be earning a $200,000 profit on a $40,000 investment. That’s a 500% gain in 20 years!

At the same time, your 30-year mortgage will be paid down to about $98,000. The combination of price appreciation and mortgage amortization will increase your net equity to $298,000. That’s an amazing return on an investment of $40,000.

And remember, you’ll also get the benefit of enjoying the property as a vacation home.

3. You Can Enjoy Generous Tax Benefits

Since your vacation home will be generating income, you’ll also be able to write off any expenses paid in connection with earning that revenue.

Let’s say you rent out the home 25% of the year. The IRS will allow you to deduct about 25% of the carrying costs of the property against the income it generates.

Expenses you can write off include mortgage interest, real estate taxes, property insurance, homeowner’s association dues, property maintenance, utility expenses, cleaning costs, supplies (for tenants), and management fees if you hire an outside service to manage the process.

Another expense is depreciation. The IRS will allow you to depreciate the value of the home (not including the land value) over roughly 30 years. Since depreciation is what’s known as a paper expense, it will reduce your tax liability without costing you any money.

Of course, you can only apply depreciation to the business use of the home. If that’s 25%, you’ll only be able to depreciate 25% of the value of the house.

Speaking of income taxes, when you decide to sell the home, you’ll get the benefit of long-term capital gains tax rates.

If your taxable income is $100,000, you’ll be in the 22% tax bracket for federal income tax purposes. But since the sale of the vacation home will be a long-term capital gain, you’ll pay only 15% on that gain.

4. You’ll Be Building a Real Estate Portfolio

One of the most common and valuable pieces of advice when it comes to investing is diversification. That’s about spreading your money over several investments. It not only minimizes potential losses from any single investment, but it will also give you access to more investment opportunities.

Because of the high cost of property, it can be difficult to diversify with real estate. But if you already own a primary residence and buy a vacation home, you’ll be diversifying your real estate portfolio across two properties.

If property values rise over the long term, as they usually do, you’ll get the benefit of capital gains on two properties rather than one.

5. You’ll Have a Vacation Property for You and Your Family – Paid for by Your Tenants!

I touched on an example of this earlier, renting out the home part of the year to cover the entire cost of owning it. Even if you don’t make a profit from the rentals, the revenue it generates will give you a cost-free vacation property.

Think about the thousands of dollars you’ll save each year by staying at hotels or renting out someone else’s vacation property. Then multiply those savings by 20 or 30 years.

The benefit could easily be worth well over $100,000. While that may not be a direct investment, it will free up plenty of cash to make other investments.

6. The Vacation Property Could Become Your Retirement Home

This benefit may not be so obvious because it isn’t financial. But it can be every bit as important. In fact, this gets to the meat of Steve’s question.

The vacation home you buy for a short-term rental can also serve as your retirement rehearsal. It’ll give you a chance to spend an extended amount of time in the vacation home. During that time, you can decide if the property will be the right retirement home for you.

Making a geographic move for retirement can be more stressful and disruptive than you anticipate.

But if you already live in the retirement destination for at least part of the year, you’ll already know the new community.

And even if you decide against using your vacation home as your retirement home, it can help you decide if the area it’s located in is the right one for you. If it is, you can sell your vacation home and reap the profit, then buy another home in the area.

You’ll already know the lay of the land as well as local property values. That’ll remove a lot of the risk that comes with making a major move.

Cons of Buying a Vacation Property for Short-term Rentals

Even though there are a lot of benefits to buying a vacation property for short-term rental, there are an equal number of cons. Before taking the plunge, it’s important to know what those negatives are and to be prepared upfront.

1. Vacation Homes Require Larger Down Payments and Have Higher Interest Rates

You’ve got to love those low down payment, low-interest-rate mortgages you see advertised all the time.

Newsflash:

Let’s start with the down payment requirement. Lenders permit a down payment of as low as 3% on a primary residence. If you’re eligible for a VA loan, you can get 100% financing – or 0 down payment.

But if you’re purchasing the vacation property, the minimum down payment requirement is 10%. Lenders may require a larger down payment if you have tighter qualifications. That can include higher debt ratios and lower credit scores.

Even if you can get a vacation home with a 10% down payment, you’ll be required to pay private mortgage insurance (PMI). That can increase your monthly payment substantially. If you’re buying a vacation property, you should plan on making a 20% down payment to minimize the payment.

Interest rates will also be higher. If the best rate available on a primary residence is 4%, expect to pay 4.5% for a loan on a vacation home.

You should also know that mortgage qualification will be more difficult with a vacation property. Since it’s considered to be a luxury purchase, lenders will look for a large down payment, a low debt-to-income ratio, and good or excellent credit.

One other point about qualification – you won’t be able to use rental income on a vacation home to qualify for the mortgage.

If you even indicate your intention to rent out the property, the lender will reclassify the home as an investment property. They’ll require a minimum down payment of 20% and charge an even higher interest rate.

2. Not All Communities Welcome Short-Term Rentals!

If you plan to buy a vacation home that you’ll rent out, even on a short-term basis, you’ll need to do your homework. Not all communities welcome short-term rentals. They prohibit them under transient use restrictions.

Find out if the community where your intended vacation property is located has such restrictions. If so, the short-term rental idea will be a non-starter.

Some condominiums also prohibit short-term rentals. It’s not usually the case in condominiums located in or near resort areas. But the restrictions vary from one condominium to another.

You’ll need to find out in advance if there are any restrictions in a neighborhood. Even though the condominium is in a perfect vacation location, that particular neighborhood may have been built specifically for owner-occupants, not short-term tenants.

Just as important, there is a restriction on short-term rentals with mortgage lenders.

If a property is used for short-term rentals, it can be classified as a condotel. That’s a hybrid of the words “condominium” and “hotel.” It refers to a condominium that will essentially be used as a hotel.

While these are popular in resort areas, they’re a no-go with traditional mortgage lenders. Since they’re viewed as commercial properties, you’ll need to get a commercial mortgage to purchase one.

That’ll mean an even larger down payment and a higher interest rate. The loan may also include more restrictive terms, like a variable-rate mortgage with a term of only 10 years.

3. Tenants Can Damage the Property

Whenever you have tenants on a property, there’s always the possibility of damage. It’s even more likely with short-term rentals. Like a hotel room, you’ll have a revolving door of tenants using the property over the course of a year.

Not all tenants are entirely responsible. You can collect a deposit to cover potential damage, but you may need to take legal action if the damage exceeds the deposit and the tenant refuses to pay.

Even if no single tenant does any real damage, having a dozen or more renters on the property each year for several years will require more maintenance and repair work than you’re probably doing on your primary residence.

That will translate into money out-of-pocket and time and effort on your part.

This is a good time to bring up homeowners’ insurance. To save money, you might be tempted to get a standard homeowner’s insurance policy on your vacation home. That’s a bad idea! Really bad!!!

A standard homeowner’s policy will cover only damage to the property from normal use by you, your family, and your guests.

If the property is damaged by a tenant, the insurance company won’t pay the claim. They may even terminate your policy for misrepresenting its intended use.

You’ll need to get a special policy acknowledging the use of the property for short-term rentals. It’ll be more expensive than a standard homeowner’s insurance policy. But if you don’t have it and your property is damaged or destroyed by a tenant, you’ll have no coverage under a standard policy.

4. Managing a Vacation Property Is Not a Passive Activity!

Don’t count on your vacation property being pure fun in the sun if you use it for short-term rentals. I’ve already covered the requirements for regular cleaning, repairs, and maintenance. But that’s just the start.

You’ll also need to market the property to keep it rented. That will mean advertising the property, screening tenants, and handling the paperwork for each rental. You’ll also need to inspect the property after each rental to keep track of which tenant may have damaged the home.

To put it mildly, managing a vacation property with short-term rentals is a part-time job. The word “vacation” can quickly become overwhelmed by the reality that you’re running a business out of your second home. Yup, that’s what’s really happening.

There are management companies that will handle this for you. But if you go this route, expect to pay a fee of between 10% and 20% of the rental income on the property.

5. You Won’t Be Able to Use the Vacation Property Any Time You Want

There’s an inherent conflict with using a vacation property for short-term rentals. It’s likely you’ll want to be using the home at the very times of the year that will generate the most tenants and the highest rents.

So you buy a beach house with the idea of spending a few weeks enjoying it during the peak of summer. But each week you’re using the home, you’ll be missing out on the highest rents of the year.

The problem is even bigger with resort properties. For example, a beach location will be most popular during the summer months. A house in a ski resort will be in high demand during winter. That kind of property may only have rental value during peak season.

If you like to go to the beach in the summer or ski during winter, you may not get that chance – not if you want to maximize your income on the property.

You might have it rented out during peak seasons, leaving you to enjoy it only in the off-season. That will maximize the investment return. But it’ll be done at the cost of compromising its vacation value.

6. The Property May Not Rise in Value

Property appreciation is not uniform across all markets. While it may be common in metropolitan markets, it’s less certain in resort areas. It’s possible a vacation property won’t rise in value at all and may even decline.

Resort properties are often in remote locations. They’re not suitable for year-round occupancy because there are few employment opportunities or other services that will appeal to permanent residents.

In resort areas that depend on the tourist trade, property values can fall if tourism slows. The decline can be even more dramatic if the area is also overbuilt.

That’s common during years of heavy tourist traffic. But if that comes to an end, builders are stuck with unsold inventory, and property values fall throughout the community. The best example of this is what happened to property values in Miami during the last recession.

That doesn’t mean values are doomed to fall in the resort area or that they’ll never come back. But if you’re buying a vacation home for income purposes, it’s a risk you need to be aware of from the start.

The Bottom Line: The Pros and Cons of Buying a Vacation Property for Short-Term Rentals

I hope that answers your question, Steve. If you’re looking to buy a vacation home mainly for personal use, the financial angle may not be as important.

But if you’re interested in buying a vacation property for short-term rental, you’ll need to think of it as a business. The information in this response will help you do just that.

Also, if you would like to start investing but are unsure of whether to invest in real estate or index funds, read my post on Real Estate vs Index Funds.

OK readers, if you have a financial question you’d like me to answer, just drop me a line at Ask Jeff a Question @ GoodFinancialCents®.