In How to Calculate Your True Net Worth, I covered the basics of net worth and how to calculate it. But there’s actually more than one type of net worth.

In that article, we covered what might be best described as total net worth, which is really something of an exaggeration. A much more accurate definition is liquid net worth.

It follows the same general calculation methodology for total net worth but takes into account transaction costs and other factors involved in converting non-liquid assets to actual cash.

For that reason, liquid net worth is lower than the total net worth.

Let’s look at why that is.

Table of Contents

Why Liquid Net Worth Matters

It can feel good to quote total net worth because it’s really an optimized number. You’re taking the gross value of your assets and then subtracting your liabilities, which leaves you with a maximum net worth.

Liquid net worth matters because it better reflects the amount of money you have available if you need to liquidate your assets in short order.

As I pointed out in How to Calculate Your True Net Worth, total net worth uses the following calculation:

But unless your assets are held in very liquid form, your liquid net worth is really your true net worth. That’s because it will take all liquidation costs into consideration.

If you had to liquidate your entire estate to pay for an emergency expense, your liquid net worth is all that would really matter.

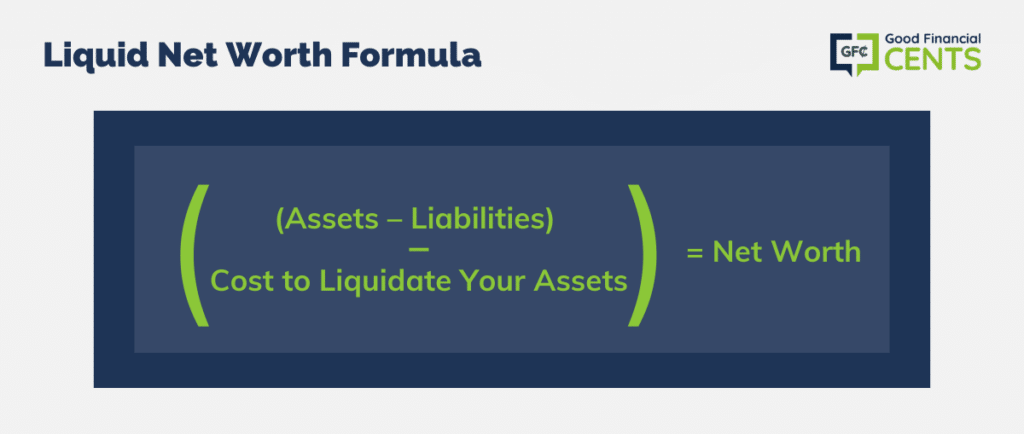

The calculation for liquid net worth looks like this:

The cost to liquidate your assets is the basic difference between total net worth and liquid net worth.

Total Net Worth vs. Liquid Net Worth

If the gross value of your assets is $500,000, and you have $300,000 in liabilities of all types, your total net worth will be $200,000. But your liquid net worth will be something less.

For example, let’s say you needed to liquidate all your assets to pay for a major medical procedure, to help a family member in need, or to start a new business.

Since the liquidation would have to happen fairly quickly, you also might not get full market value for the assets you’re liquidating.

In that situation, you might sell your house for 10% less than fair market value to generate a quick sale. You might do the same thing with the sale of a second car or a vacation home.

In the case of selling real estate, you’ll also have to deduct transaction costs. The same would be true if you’re selling financial assets like stocks or bonds.

Transaction costs will always figure into the liquidation of any non-cash assets. And the degree to which you may have to discount an asset for a fast sale will depend on how quickly it needs to be sold.

If in liquidating your $500,000 in total assets, you have to discount them by $50,000 and then incur $30,000 in liquidation costs, your total assets would be reduced to $420,000. After subtracting $300,000 in liabilities, your liquid net worth will be $120,000.

That’s $80,000 less than your total net worth, but it represents your actual net worth.

For what it’s worth if you’re applying for a loan with a bank, they’ll likely accept your total net worth as the actual number. But in a situation where you actually need to liquidate your assets to raise cash, liquid net worth will be the real number.

Need a Loan? Click here to Check Your Rate in Seconds.

Factors That Affect Liquid Net Worth

These factors will be different for everyone, based on the composition of their holdings.

For example, if most of your assets are in real estate or retirement savings, your liquid net worth will be a lot lower than someone who has the majority of their assets in cash and cash equivalents.

There are liquidation factors unique to each asset class.

True Liquid Assets

These include cash and cash equivalents. Examples are:

- Cash on hand

- Checking and savings accounts

- Money market accounts

- Certificates of deposit (CDs)

Since there are generally no fees or market value considerations with any of these assets, they won’t be reduced upon liquidation.

However, in the case of CDs, you’ll normally pay a small prepayment penalty if you liquidate the certificate before the stated term is over.

Retirement Plans

The contribution retirement plans make to liquid net worth might be the most misunderstood of all personal assets.

Most people assume if they have $200,000 in a 401(k) plan, that makes a full $200,000 contribution to their net worth.

That’s never true, at least not in the case of liquid net worth.

The reason is income taxes. Retirement plans are tax-deferred, but not tax-free. If you have to liquidate your 401(k) plan today, you’ll have to pay ordinary income tax on the amount withdrawn.

And if you’re under 59 ½, you’ll also have to pay a 10% early withdrawal penalty in most cases.

If your combined state and federal income tax marginal tax rates are 20%, you’ll pay 30% of the amount of the plan upon liquidation (including the 10% penalty). That tax bite will reduce a $200,000 plan down to $140,000.

There may also be liquidation charges, payable to the plan administrator, as well as commissions on the sale of assets held in the plan. That could potentially shave a few thousand dollars more off the value of your plan.

The only limited exception is a Roth IRA, and then only if you are at least 59 ½ and have participated in the plan for at least five years.

If you meet those qualifications, and you liquidate the entire plan, no tax or penalty will be required. You would get the full $200,000 in the plan.

Of course, if you’re under 59 ½, you’d have to pay ordinary income tax and the 10% early withdrawal penalty on the investment earnings portion of your Roth IRA.

Real Estate

When it comes to going liquid, real estate is probably the most complicated asset of all. Even in a strong housing market, it can take weeks to sell a house. But in a slow market, it can take months.

Exactly how much it can be sold for will depend upon how quickly you want to sell. If you need to sell right away, you’ll have to cut the price it below the prevailing market value.

If the house has a fair market value of $300,000, but you need to sell quickly, you might have to drop the price down to 280,000, or even $270,000.

Of course, if you’re prepared to wait as long as it takes to sell, you’ll likely get the full market value.

Real Estate Transactions Costs

But apart from market factors, there are also transaction costs. Those can be steep.

A traditional real estate agent will charge a 6% commission to sell a home. You can easily get a service that will sell it for substantially less, but the services they provide may be greatly reduced. If you need a quick sale, that may not help your cause.

But even apart from a real estate sales commission, there are other costs. You can generally figure you’ll need to pay between 1% and 2% in closing costs.

Those may involve an attorney fee, any transaction taxes in your state, or other fees charged to sellers in your market.

Depending on the real estate market in your area, you may also need to pay seller paid closing costs for the buyer. Paying the buyer’s closing costs is a valuable inducement to get prospective buyers to make an offer on your home. That’s the good part.

The downside is that you’ll actually have to pay those closing costs. That could be another 2% or 3% of the sale price of your home.

Altogether, transaction costs to sell your home may approach 10%. If you’re looking to calculate liquid net worth, you should deduct that from the fair market value of your home – even if you don’t plan to sell in the near future.

Business Interests

Including business equity in your net worth is tricky. Under the best of circumstances, valuing a business is an inexact science, and no better than an estimate. Under the worst of circumstances, it may be impossible to come up with a reasonable number.

Apart from the difficulty in valuing a business, you also have to make a reasonable guess on the salability of the business. Simply put, some businesses are easier to sell than others.

And if a business is too closely associated with you personally, like if I were trying to sell “Jeff Rose, Inc.”, the business may not have much market value at all. In that case, I am the business, so it may not have much value without me.

Most people just guess at the value of their businesses. But if you want a more accurate number, you’ll need to periodically have the business appraised by an industry expert. And even that is likely to produce nothing more than a ballpark.

Converting a business to cash is also problematic. If it’s your primary source of income, selling it may not even be practical.

And even if you do sell it, it can be anyone’s guess how long that will take. You’ll also need to subtract any business debts from the value of the business.

For most people who are self-employed, it’s best to completely exclude business equity from liquid net worth.

“Furnishings and Trinkets”

Most people overvalue their personal possessions because they assign valuations based on retail costs. But if you had to convert them to cash, the retail value would be completely irrelevant.

All that matters is what they could be sold for. That will depend on finding a willing buyer.

As a general rule, your personal possessions are probably not worth more than 10% to 20% of their retail value. Exceptions would be certain jewelry items or artwork, for which there are established markets.

You also have to consider the impact selling personal possessions will have on your lifestyle. It may be that you can’t sell any more than half your personal possessions and only those that are least essential to your daily life.

On balance, $50,000 in furnishings and trinkets may have a cash sale value of no more than $5,000 to $10,000. And that will be even lower since you probably can’t sell them all.

An Example of How to Calculate Liquid Net Worth

Let’s do a quick example to demonstrate the difference between total net worth and liquid net worth.

The total value of your assets is $600,000, and your liabilities are $300,000. That gives you a total net worth of $300,000.

But to determine liquid net worth, let’s look at each asset individually:

- Primary Residence: The fair market value is $400,000, with an outstanding mortgage balance of $250,000. To sell the house quickly, you might drop the value to $380,000.

If it sells at that price, there will be another 10%, or $38,000, in transaction costs. After paying off the mortgage, the net cash from selling your house will be $92,000.

- Cars: You have two vehicles with a fair market value of $50,000. (You should verify the value with Kelley Blue Book or another respected auto valuation service.)

There are outstanding loans of $30,000, making the net value of your cars upon sale $20,000.

- Retirement Savings: The total value is $100,000. You’d have to pay 30% in taxes and penalties plus 1% in transaction costs to fully liquidate the plan.

That drops it to $69,000. But you also have a 401(k) loan of $10,000 against the plan. Since that would have to be paid back upon liquidation, the cash value of your retirement plan is $59,000.

- Furniture and Trinkets: You assign a value to these based on a retail cost of $50,000. But upon sale, they only bring $10,000.

But since you also have $10,000 in credit card debt – largely used to purchase those possessions – the net cash value of your furniture and trinkets is zero.

Based on all the factors above, your liquid net worth looks like this:

- Primary Residence: $92,000

- Cars: $20,000

- Retirement Savings: $59,000

- Furniture and Trinkets: $0

- Total liquid net worth: $171,000

Breakdown of Liquid Net Worth and Assets

| Asset Type | Current Value | Outstanding Loan | Net Value |

|---|---|---|---|

| Primary Residence | $400,000 | $250,000 | $92,000 |

| Cars | $50,000 | $30,000 | $20,000 |

| Retirement Savings | $100,000 | $10,000 | $59,000 |

| Furniture and Trinkets | $50,000 | $10,000 | $0 |

| Total Assets | $600,000 | — | $171,000 |

| Liabilities | $300,000 | — | — |

| Liquid Net Worth | — | — | $171,000 |

Final Thoughts on Liquid Net Worth

As you can see from the example above, there’s a big difference between total net worth and liquid net worth.

In the example, we started out with a total net worth of $300,000. But after deducting for marketing factors, taxes, and transaction costs, we ended up at $171,000.

That’s a difference of $129,000, which is a long way from pocket change and rounding errors.

Your total net worth isn’t completely irrelevant, it’s just not as accurate as you may want to believe. In either case, it helps to know both your total and liquid net worth.

The moral of the story is that liquid net worth is closer to your true net worth. And that makes a strong case for saving and investing even more money than you think you should.

After melting down everything you have and paying off all liabilities, you’re probably worth less than you think. And a lot less at that.