Investing well is about balancing risk and reward. The unprecedented challenges facing the world economy have many savers looking to reduce their exposure to risky investments and move towards those with lower risk.

While it’s true that the amount of return you can get depends on how much risk (and losses) you are willing to accept, great investors make their living by balancing these forces.

While we can’t decide for you how much risk you are willing to take, we have structured this guide to give you a range of options based on zero, low, or medium risk for long-term investments.

Table of Contents

- The Top 15 Best Low-Risk Investments With The Highest Returns:

- Where To Start – Low-Risk Investing

- My Favorite Low-Risk Investment Right Now

- Long-Risk Investments That Require Zero Risk-Taking

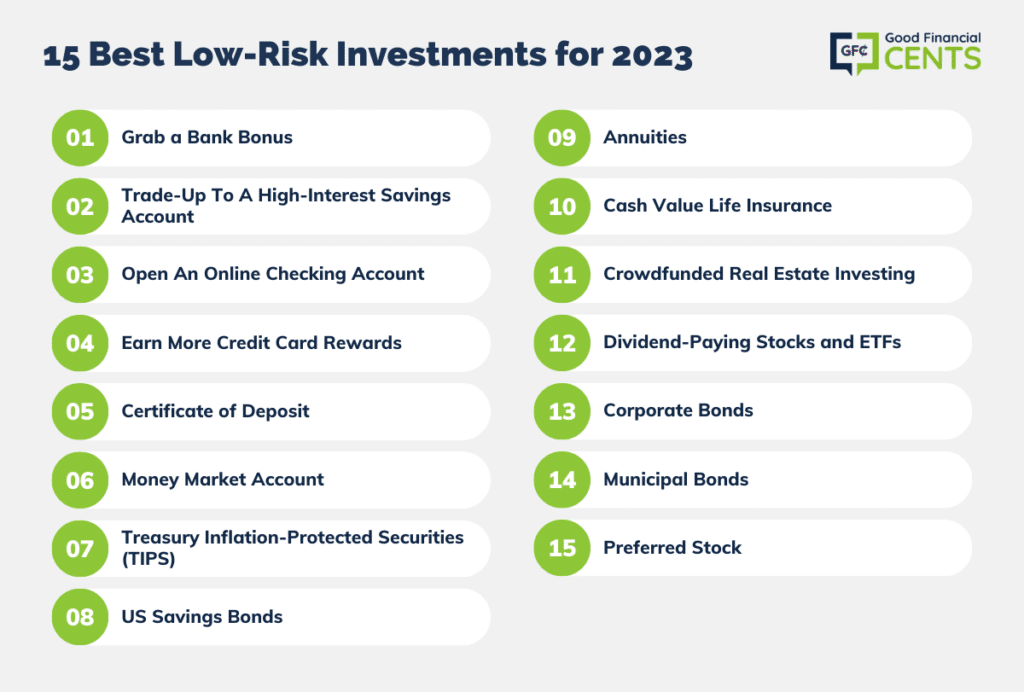

- 1. Grab a Bank Bonus

- 2. Trade-Up To A High-Interest Savings Account

- 5.26%

- varies

- 3. Open An Online Checking Account

- 4. Earn More Credit Card Rewards

- Best Low-Risk Investment Options

- 5. Certificate of Deposit

- 6. Money Market Account

- 7. Treasury Inflation-Protected Securities (TIPS)

- 8. US Savings Bonds

- 9. Annuities

- 10. Cash Value Life Insurance

- Medium Risk Investment Options

- 11. Crowdfunded Real Estate Investing

- 12. Dividend-Paying Stocks and ETFs

- 13. Corporate Bonds

- 14. Municipal Bonds

- 15. Preferred Stock

- The Bottom Line on Low Risk Investments in June 2026

- FAQs on Low to Medium-Risk Investments

Some of these options like picking up a bonus for switching banks, or getting into a higher-yield savings account carry zero risk. Other options could take some additional learning or planning on your part.

The Top 15 Best Low-Risk Investments With The Highest Returns:

|

Zero Risk Investments Seriously, this is free money. |

|

| Low-Risk Investments Still secure, minimal downside. |

|

|

Medium Risk Investments Losses can occur from time to time. |

|

Where To Start – Low-Risk Investing

For anyone looking to start investing, I recommend just getting started small because nothing leads to learning faster than action. The easiest way to get started investing in a whole host of asset classes is through a “robo-advisor“.

My personal favorite is M1 Finance because it’s low-cost and dead simple to use. They offer individual stocks, ETFs and give you the ability to build your own custom portfolios.

My Favorite Low-Risk Investment Right Now

Fractional Real Estate

One of the historically lowest risk/highest return asset classes is real estate. The problem has always been that it’s really hard to get started with small amounts of money.

In recent years, great platforms like Fundrise have popped up and “democratized” access to real estate investments. This advancement makes real estate a very viable option for people looking for alternatives to the stock market.

With Fundrise, you can get started with a well-diversified portfolio of commercial and multi-family real estate with as little as $10.

| I’ve been investing with Fundrise since 2018. Disclosure: when you sign up with my link, I earn a commission. All opinions are my own. |

Long-Risk Investments That Require Zero Risk-Taking

Ok, maybe these aren’t actual investments, but consider them smart money moves to make more money and optimize your finances at a baseline.

1. Grab a Bank Bonus

If you have some extra money you won’t need for a while, you can occasionally earn some free cash with a bank bonus from one of the nation’s best banks. Most banks will offer a bonus as an incentive for you to sign up, and these bonuses can be worth several hundred dollars on their own.

Bank bonuses are sometimes regional, however, and can depend on the local banks in your area and the products they offer.

In exchange for your bank bonus, you may have to set up a direct deposit to your new account or use a bank-issued debit card for a certain number of transactions within the first few months.

READ BEFORE YOU SIGN

Just remember to read through all the fine print to learn about any fees that might be levied and how you can avoid them.

By jumping through these hoops, you can usually earn a few hundred dollars for your efforts. Best of all, you won’t have to worry about losing a single cent of your deposit. And if you decide not to keep the account for the long haul, you can always close it once you earn the bonus and meet all of the bank’s requirements.

2. Trade-Up To A High-Interest Savings Account

If you’re looking for a risk-free way to earn some interest on your money, a high-yield savings account might be your answer. With these accounts, you’ll earn a nominal amount of interest just for keeping your money on deposit.

Other than opening your account and depositing your money, this strategy requires almost no effort on your part, either. The best high yield savings accounts offer competitive interest rates without charging any fees. Currently the highest savings rate goes to:

5.26%

Interest Rate

varies

Min. Initial Deposit

3. Open An Online Checking Account

Just like high-yield savings accounts, online checking accounts let you earn small amounts of interest on the money you deposit. If you’re going to park your money in the bank anyway, you could surely appreciate earning some interest along the way. Best of all, many online checking accounts charge zero or minimal fees to get started.

When looking for an online checking account that actually lets you earn interest, look for a bank with excellent customer service, a user-friendly online interface, and competitive interest rates.

If you want the utmost flexibility, it’s also important to seek out an account that doesn’t impose account minimums or deposit requirements. And if you want to withdraw money frequently, you’ll want to make sure you have access to local, no-fee ATMs as well.

4. Earn More Credit Card Rewards

Credit cards are not the devil. We all spend money, and when used properly, a credit card can help you earn cashback on your spending. By picking up a cash-back credit card, you earn “points” that translate into real money.

In reality, the “rewards” you earn with some of the top cards are far more lucrative than anything you might earn with a Certificate of Deposit or online savings account.

With credit cards I currently earn:

- 5% Back on Cable, Internet, Cell Service, and at Amazon and Target

- 3% Back on Dining and Travel

- 6% Back at the Grocery Store

- 2% Back on Gas

Here’s how these offers work:

Let’s say you picked up a Chase Sapphire Preferred® card and put your regular spending on it to earn the signup bonus. Once you spent $4,000 on your card in 90 days, you would earn 60,000 points worth $750 in travel ($600 in gift cards or cashback). If you spent that $4,000 on bills you would normally pay like groceries, daycare, or utilities, and paid your card off right away, this is the closest thing to “free money” you’ll ever find!

If you want to learn more about the easy money you can score with credit card rewards, check out our guide on the best cash-back credit cards.

Best Low-Risk Investment Options

These investment options carry a very small amount of risk overall. In turn, you won’t expect to make as much, but your money should be relatively safe and still earn yields.

5. Certificate of Deposit

No matter how hard you look, you won’t find an investment more boring than a Certificate of Deposit. With a Certificate of Deposit (CD), you deposit your money for a specific length of time in exchange for a guaranteed return no matter what happens to the interest rates during that time period.

Be sure and buy your CD with an FDIC-insured financial institution (up to $250k is insured). The longer the duration of the CD, the more interest the financial institution will pay.

For a quick low-risk turnaround, I recommend a CIT Bank 11-month No Penalty CD at 4.15%.

6. Money Market Account

A money market account is a mutual fund created for people who don’t want to lose any of the principal of their investment. The fund also tries to pay out a little bit of interest as well to make parking your cash with the fund worthwhile. The fund’s goal is to maintain a Net Asset Value (NAV) of $1 per share.

These funds aren’t foolproof, but they do come with a strong pedigree in protecting the underlying value of your cash.

It is possible for the NAV to drop below $1, but it is rare. You can park cash in a money market fund using a great broker like TD Ameritrade, Ally Invest, and E*TRADE or with the same banks that offer high-interest savings accounts.

While you may not earn a lot of interest on your investment, you won’t have to worry about losing vast amounts of your principal or the day-to-day fluctuations in the market.

7. Treasury Inflation-Protected Securities (TIPS)

The US Treasury has several types of bond investments for you to choose from.

One of the lowest risks is called Treasury Inflation Protection Securities, or TIPS. These bonds come with two methods of growth. The first is a fixed interest rate that doesn’t change for the length of the bond. The second is built-in inflation protection that is guaranteed by the government.

For example, you might invest in TIPS today which only comes with a 0.35% interest rate. That’s less than the certificate of deposit rates and even basic online savings accounts.

That isn’t very enticing until you realize that, if inflation grows 2% per year for the length of the bond, then your investment value will grow with that inflation and give you a much higher return on your investment.

TIPS can be purchased individually or you can invest in a mutual fund that, in turn, invests in a basket of TIPS. The latter option makes managing your investments easier while the former gives you the ability to pick and choose with specific TIPS you want.

Want to protect your portfolio from inflation? Purchase TIPS through a great broker like:

- TD Ameritrade

- Ally Invest

8. US Savings Bonds

US Savings Bonds are similar to Treasury Inflation-Protected Securities because they are also backed by the United States Federal government. The likelihood of default on this debt is microscopic which makes them a very stable investment.

There are two main types of US Savings Bonds: Series I and Series EE.

Series I bonds consist of two components: a fixed interest rate return and an adjustable inflation-linked return. They are somewhat similar to TIPS because they have the inflation adjustment as part of the total return. (You can see the current rates on Series I Bonds here)

The fixed rate never changes, but the inflation return rate is adjusted every 6 months and can also be negative (which would bring your total return down, not up).

Series EE bonds just have a fixed rate of interest that is added to the bond automatically at the end of each month (so you don’t have to worry about reinvesting for compounding purposes).

Rates are very low right now, but there is an interesting facet to EE bonds: the Treasury guarantees the bond will double in value if held to maturity (which is 20 years).

That equates to approximately a 3.5% return on your investment. If you don’t hold to maturity you will only get the stated interest rate of the bond minus any early withdrawal fees.

Another bonus to look into: if you use EE bonds to pay for education, you might be able to exclude some or all of the interest earned from your taxes.

Looking to purchase some Series I or Series EE Bonds? You can do that directly through TreasuryDirect.gov.

9. Annuities

Annuities are a point of contention for some investors because shady financial advisors have over-promoted them to individuals where the annuity wasn’t the right product for their financial goals.

They don’t have to be scary things; annuities can be a good option for certain investors who need help stabilizing their portfolio over a long period of time.

If you’re in the market for an annuity, however, be aware of the risks and talk with a good financial advisor first.

Annuities are complex financial instruments with lots of catches built into the contract. Before you sign on the dotted line, it’s important to understand your annuity inside and out.

There are several types of annuities, but at the end of the day, purchasing an annuity is on par with making a trade with an insurance company. They’re taking a lump sum of cash from you.

In return, they are giving you a stated rate of guaranteed return. Sometimes that return is fixed (with a fixed annuity), sometimes that return is variable (with a variable annuity), and sometimes your return is dictated in part by how the stock market does and gives you downside protection (with an equity-indexed annuity).

If you are getting a form of guaranteed return, your risk is a lot lower. Unlike the backing of the Federal government, your annuity is backed by the insurance company that holds it (and perhaps another company that further insurers the annuity company). Nonetheless, your money is typically going to be very safe in these complicated products.

10. Cash Value Life Insurance

Another controversial investment is cash value life insurance. This life insurance product not only pays out a death benefit to your beneficiaries when you die (like a term life insurance policy) but also allows you to accrue value with an investment portion in your payments.

Whole life insurance and universal life insurance are both types of cash value life insurance. While term life insurance is by far a cheaper option, it only covers your death.

One of the best perks of using cash value life insurance is that the accrued value can not only be borrowed against throughout your life but isn’t hit with income tax.

While cash value life insurance isn’t for everyone, it is a clever way to pass some value onto your heirs without either side being hit with income tax.

See our recommended life insurance companies.

Medium Risk Investment Options

All of these options carry more of an average risk profile and are variations of traditional stock/bond investing. You may want to consult a financial advisor when looking at these options.

11. Crowdfunded Real Estate Investing

If you like the idea of investing in real estate but shudder at the thought of being a landlord or home prices where you live are too expensive, real estate crowdfunding could be the solution!

Real estate crowdfunding became popular after Congress passed the 2012 Jobs Act, which essentially allowed real estate investors and developers to raise money from the public to fund their projects.

Let’s say a developer has plans to build a 200-unit condominium in Las Vegas. In the past, he could only raise funds for this project from private investors in his network. These days, however, he can list his project on a real estate crowdfunding platform and anyone in the public can invest!

Fundrise operates like Lending Club, except all of the investments are geared toward real estate. They keep risks low and interest high by carefully vetting the projects they invest in.

12. Dividend-Paying Stocks and ETFs

One of the easiest ways to squeeze a bit more return out of your stock investments is simply to target stocks or mutual funds that have nice dividend payouts.

If two stocks perform exactly the same over a given period of time, but one has no dividend and the other pays out 3% per year in dividends, then the latter stock would be a better choice.

With dividend stock mutual funds, the fund company targets stocks that pay nice dividends and does all of the work for you.

13. Corporate Bonds

Unlike U.S. Treasury bonds, corporate bonds are not backed by the government. Instead, a corporate bond is debt security between a corporation and investors, backed by the corporation’s ability to repay the funds with future profits or use its assets as collateral.

Since you are taking on risk by investing in a company, the returns on corporate bonds are higher than other types of bonds, no matter how creditable the company’s reputation is. While that’s reassuring enough for some investors, if you’re looking for truly low-risk corporate investing, you should consider bond funds.

Bond funds come in the form of ETFs or mutual funds and help to diversify your investment across a number of bonds.

Robo advisors provide a great opportunity for investing in bond funds. If you’re looking to choose what types of funds to build into your portfolio but don’t want to deal with the hassle of constantly balancing your account and re-allocating funds, these might be best for you.

14. Municipal Bonds

When a government at the state or local level needs to borrow money, they don’t use a credit card. Instead, the government entity issues a municipal bond. These bonds, also known as munis, are exempt from Federal income tax, making them a smart investment for people who are trying to minimize their exposure to taxes.

Taxes on Muni Bonds

Most states and local municipalities also exempt income tax on these bonds but talk to your accountant to make sure they are exempt in your specific state.

What makes municipal bonds so safe? Not only do you avoid income tax (which means a higher return compared to an equally risky investment that is taxed), but the likelihood of the borrower defaulting is very low. There have been some enormous municipality bankruptcies in recent years, but this is very rare. Governments can always raise taxes or issue new debt to pay off old debt, which makes holding a municipal bond a pretty safe bet.

You can buy individual bonds or, better yet, invest in a municipal bond mutual fund at brokers like:

- TD Ameritrade

- Ally Invest

- E*TRADE

15. Preferred Stock

Adding on to the dividend stock theme is preferred stock. Preferred stock is a type of stock that companies issue that has both an equity (stock) portion and a debt portion (bond). In the hierarchy of payouts to forms of investments, preferred stock sits between bond payments (which come first) and common stock dividends (which come last).

Preferred stocks are not traded nearly as heavily as common stock, but do have less risk than the common stock. It is just another way to own shares in a company while getting dividend payments.

You can track down preferred stock investments at:

The Bottom Line on Low Risk Investments in June 2026

As you get closer to retirement, it’s important to reduce your risk as much as possible. You don’t want to start losing capital this late in the game; since you have many years of retirement ahead of you, you want to preserve your cash.

The best low-risk investments can help you do just that. By letting you earn nominal amounts of interest on your money with little risk, you can help your nest egg keep up with inflation without losing your shirt. Just remember to read the fine print and educate yourself along the way. And if you’re ever in doubt over an investment product or service, speak with a qualified financial advisor and ask as many questions as you can.

Check out some of our individual stockbroker reviews to help you get a better grasp on what will meet your investment needs:

FAQs on Low to Medium-Risk Investments

The lowest-risk investment is typically a savings account at a bank or credit union. Savings accounts are insured by the Federal Deposit Insurance Corporation (FDIC) for banks or the National Credit Union Administration (NCUA) for credit unions, so your money is safe. They also have very low minimum balance requirements and allow you to access your money at any time. However, they typically have low-interest rates, so you may not earn a lot of money from your investments.

Medium-risk investments are those that carry a moderate level of risk, and they may offer the potential for higher returns than low-risk investments. However, there is also a higher chance that you could lose money.

Some examples of medium-risk investments include:

1. Mutual funds: These are investment vehicles that pool money from multiple investors and invest in a diversified portfolio of stocks, bonds, and other securities.

2. Exchange-traded funds (ETFs): These are similar to mutual funds, but they are traded on stock exchanges like individual stocks.

3. Corporate bonds: These are debts issued by companies, and they may offer higher interest rates than government bonds. However, they are slightly riskier because they are not backed by the government, and the company could default on its payments.

4. Individual stocks: Buying individual stocks carries more risk than investing in mutual funds or ETFs because you are betting on the performance of a single company rather than a diversified portfolio.

Individual stocks can offer the potential for higher returns but are also subject to market swings. If you are investing in stocks, consider dividend stocks as a solid option.

Some investments have zero risk, such as investing in a U.S. Treasury bill or a certificate of deposit from a bank. These investments are guaranteed by the federal government, so investors are virtually guaranteed to get their principal back plus interest.

How to invest in preferred shares

So basically nothing pays much, but if you want to play around with money try one of these. You bet!

Not sure anyone can be trusted in today’s world. There are so many scammers everywhere.

Hi! Excellent content! Looking forward to other tips you can give us regarding investments. Thank you!

very well written and informative…most articles advised retirees or close to retirement to take on more risk..i like the idea to be conservative while in or near retirement..

“In my experience, CIT Bank has a great reputation for offering some of the most competitive CD rates.”

You’re kidding, right?

Cit Bank, for a jumbo account, is sitting around 1.75% for a 5 year CD. Compared to over 3% for USAA, Capital One, etc….Even Wells Fargo, for a non-jumbo account is 2.47-2.50%

1.75% is not even remotely competitive, and their other rates aren’t even worth mentioning.

You should cast your gaze further than Cit Bank.

USAA website shows jumbo CD rates for 12 months at 1.85%. I do not find +3% as you stated. Where can you get 3% for a CD?

Kindly elucidate on franchise investment and its rate of return. I mean franchising investment where an investor invests his money to earn profit. Thanks

i would like to start investing my money on a number of things incl JSE, unit trusts, index tracker funds, stock markets tax free benefits for long term and possible forex trading. Please advise asap before i commit my money without any prior knowledge

I am interested to invest 1.0 lack dollars

Excellent information. Thank you.

The top item on your list of “best low risk investments with the highest returns” is PEER TO PEER LENDING? Are you completely INSANE? I tried it on Prosper a few years ago and ONLY went with B+ rated or better. Half the people took the money and ran and there was NOTHING we could do about it. Stupidest thing you can do with your money, hands down.

I was searching for a way to invest money but I lost my investment in the stock market so I was constantly looking for something more stable and I am very skeptical about being scammed long story short I found a Team and platform that allows me to make 1% per weekday on my investments best part is it works just like a saving account and is fully licensed. Now I want to introduce other people to it because it is not fair for our hard earned money to be scammed using shady investment tricks.

Not to burst your bubble Kevin, but 1% per day sounds a lot like a scam – or day trading. Think about it, if you could make 1% per weekday, and there are 260 weekdays per year, that’s a 260% return based on simple interest alone. I’ve not heard of a return even close to that that wasn’t a scam. Please be very careful.

I want to invest $1700.00. I’m not certain which route to take if an annuity or a savings account? I hope you can help me.

Hi Rosa – With that amount of money I’d emphasize keeping it safe and avoiding fees (that come with annuities). A good high yield savings account or CD with an online bank would be your best bet.

I have a 457 plan with ICMA. I have invested $92,578 of my own money in it over a period of 23 years. The account now has $138,000 in it. Is that normal for a 457 plan? I only found out about year 20 that we were supposed to manage the accounts ourselves. I know absolutely nothing about managing an investment account and many of the funds my money was in were making 0% per quarter but I was still being charged extravagant fees by ICMA.

Hi Jon – After 23 years that sounds ridiculously low, especially after how the financial markets have performed for the past 9 years. I’d discuss it with your employer, the plan administrator or the investment manager who charged all the fees.

SO I am wondering how much of your money went to *fees*…..did you ask?

A Nigerian prince sent me an email and is sending me 50 million dollars. He just needs my banking info so he knows where to send the money. I can’t wait…

Are you kidding…….SCAM…..trying to screw you out of the money in your account. People can NOT be trusted these days……actually some financial institutions can NOT be trusted either….(so) I discovered. It is sad.

Im thinking of investing 275K in a moderate risk Merril Lynch plan. It is not insured and I’m 2 years from retirement. What would you put it in? any insured options?

Hi Keith – Since I don’t know you personally, I won’t/can’t make specific investment recommendations. You might want to discuss this with an advisor at Merrill Lynch.

Forget Merrill Lynch, dare to invest in downtown Gulberg (Lahore, Pakistan) in a mixed use apartments building and you end up earning more than 30% per annum do a little research to brighten your after retirement life a cozy one.

Yeh……right.

The best LOW RISK investments for HIGH RETURN??? I’m shocked at this article. The financial institutions would love to paint a beautiful picture of how cash value life insurance and annuities and 1% savings accounts etc (everything you see in the article above) can give you everything you could possibly get as far as safe returns. Check out Fisher investments before you invest in one of these and ruin your savings.

Folks, do your research and due diligence. You will in almost every case listed above loose money to inflation and/or fees. I would never do business with any major financial institution, especially Merrill Lynch. They (MERRILL LYNCH) solicited me through a phone call back in the 2000’s and I listened to their pitch and invested my 401k in their fund picks. Every one failed miserably and years later I saw they got in trouble for this very thing by the SEC because they were in it for the fees and expenses and not for my success. Important lesson learned for me and since, I have found numerous places to get investment info. There is a saying no risk, no reward. That is very true. If you want any decent return (10-20%+), you must be able to stomach some risk. You just have to get used to some losses. Nobody is 100%. There are many groups out there who have some great ideas that would support higher returns for some risk, and not everything I have found with any one org is 100% for me. I have to pick and choose the pieces which I feel benefit me. The Motley Fool, Stansbury Reasearch, Oxford Club, Formula Stocks Pro, Zacks, Fisher investments all have pieces which, if you spread the risk, will produce returns beyond anything this article even hints at. Don’t line the pockets of your investment manager, PAY YOURSELF and manage your own money. Reasearch some of these and you will see for yourself. Don’t let someone talk you into believing a lie. There are returns out there. Those wall street guys aren’t super human. You are just as smart as them and you don’t need a degree in finance or economics to know where to invest your money. There are so many baby boomers out there that they see opportunity to cash in on their (OUR) financial ignorance. Take control of your finances and you will be a success. Didn’t mean to write all this but it’s true. America, we need to teach our children financial success at a young age. Just saying.

Hi Jim – I’m sympathetic with your thoughts, but there’s no perfect investment out there. We tried to address the portion of a portfolio that will be held in relatively safe investments, which every portfolio should have. We never said that any of these investment options are a cure-all. As to Fisher Investments, I’ve done some research on them and they aren’t a perfect solution either. You have to achieve balance, and invest where your comfortable.

Jim’s reply is an exact illustration on how everyone’s investment process and choices are unique to them. I think this article offers some great insights, especially for anyone curious to refresh their knowledge on the options, etc.

Hi Jeff, do you only advice investments in banks? can you guide me in how to invest in any business, like a small restaurant in a food court or something else in order to the a safe and fast return? I have around 80k to make and investment, thank you so much Jeff, regards from Cancun Mexico

Hi Oskar – I can’t give advice on investing in specific business ventures. Each has to stand on its own merits, and work in a particular location. I’m not in a position to give advice for anything that specific. Sorry!

Hi, I live in Nigeria but I would like to invest in lending club,did open the site and I wanted to register but there was some constraints like having to chose my state which i didn’t fall into an option there how would I go abt it thank you…your doing a great job here

Hi Precious – To my knowledge, Lending Club is only available to US residents. That’s why I believe you were having a problem.

hi jeff.

i actually fall to this category too. i watch your video on youtube on “11 Passive Income Ideas” and i think the p2p is better for me… is PROSPER too limited to USA or worldwide.

i just need something i can invest into. if there are other P2P investment sites you can recommend that is legit… please share with us.

thank you

Hi Wale – Most P2P investments are country specific. That’s due to national laws in each country. Try googling “peer-to-peer investing” in your own country, and see what comes up.

Is p2p lending only for US, Canada or Australia residents?

Hi Sharon – It seems to be mostly in the English speaking countries, yes. But mainly the US and UK. Not all P2P lenders are in all countries, and some are in one country only. You really have to do your research.

I’m a part time student. I work and save in bank without interest. Please can someone tell me where to invest around the world without risk or low risk. ( the website of the investment).

Hi Godwin – You might seriously look into high yield accounts with online banks, like Ally Bank. You can get 1% with no risk whatsoever.

Jeff,

Your website is excellent for those who has no much idea like me in investing money. Thank you very much. Clay

You’re welcome, Clay!

Jeff,

looked into P2P a while back. I think it was Lending Club. Seemed to me that you could not invest more that $25,000, or some limit like that. Or did it mean you could not invest more than $25,000 in a single loan, but that you could invest more through more loans. Can you help with this? What if I wanted to invest 50k, 100k? Is that possible with P2P? And I think some states were excluded, but not mine.

Hi Sen – That limit is a state law limit, not a Lending Club limit. This page from Lending Club says the following:

“Certain states have particular limitations on the amount that you may invest, but under no circumstances are you permitted to purchase Notes in excess of 10% of your net worth (exclusive of the value of your home, home furnishings, and automobile). Please see our State and Financial Suitability Policy for more details.”

So if you disclosed $250,000 in net worth, you’d be limited to $25,000 on Lending Club, or any other P2P platform in your state.

I am truly astounded to see cash value insurance on here. There couldn’t be a bigger rip-off. You fail to mention that you’ll pay a hefty interest rate on anything you borrow. You also fail to mention that cash value is lost upon payment of death benefit or visa versa. If life insurance is needed it’s ALWAYS better to pay the lower premiums of term and chose almost any of these other options.

Hi James – I said it’s controversial, and it’s not for everyone, but it does have a purpose. For people who need life insurance, but aren’t good at saving money (which describes millions of people!), cash value life insurance functions as a forced savings plan. Not the best vehicle, for all the reasons you’ve pointed out, but not entirely without use either.

I am so confused! I am a doctor who cannot get ahead of the interest on my education loans. The amount I owe is snowballing and it wakes me up at night in a cold sweat. I have very little money to invest at the end of the month but would like to do so with the goal of paying down/off my loans in large lump sum(s).

Where do I begin?

Hi Monica – Since you are earmarking savings to payoff debt, you should be as conservative as possible with your investments. CDs would probably be the best choice. You don’t want to have any risk of loss, since that would hurt your ability to use the money to payoff debt.

Jeff,

What’s the most i should be paying for a fee based account for asset management. I’m seeing all of these online options and a local person was telling me i would pay 1.75% to get my money managed-is that too high?

Hayes

@Brent I think it really depends if that is the “all in” cost. What I mean that is the advisor could be quoting you 1.75% as their advisory fee but that doesn’t include the cost of the actual investment holdings like as mutual funds or ETF’s which can drive up the cost even more.

Jeff,

Are you a broker yourself? None of my business but I am curious to ask this question. I am looking to invest with a handful maybe less of trusted individuals so that we could all capitalize equally and distribute the take when reached at a certain amount goal. What would be the best option to take here? I am looking to invest and have a generous return from the market in which I invest. The point of this is however, who or what or where do I (we) invest the funds in to seek back a return? For me personally I am looking to pay off some debt I have and invest in buying a home in the next 5 years.

I am currently 31 years of age and wished that I have done this years ago.

Hi Tim – You really need to sit down with that group of individuals and have a consensus as to where you want to invest. On in individual level with a five year time horizon, I’d probably go with an equal mix of peer-to-peer lending for higher return, and CDs for safety. But that’s just an opinion. I don’t know what your personal situation and risk tolerance are.

Hi Hayes – I’d say not more than 1% for a personal investment manager. But you can do a lot better than that. For example, Betterment will manage your account for as little as 0.15%.

Peer to Peer lending is the best utilization for your money if you are investor and best source of funding if you are Borrowers. It provides a platform where an investor can fund the borrowers without going through the traditional banking system.

Hey Jeff,

Thanks for sharing

I’m not sure if it was this episode or not but I have the same issue with wanting to jump head first into things. I need to do a better job with due diligence some times.

Frank

i think your main problem is that you are treating less than 5 years of good performance as your ‘EDGE’ while people can be lucky 5 years in a row.

Sometimes we have to concede that we are just not good enough active managers around.

@ Kyith I guess I’m not following you. Did I mention something about this in the podcast? I was sharing some of my bad investments not anything I made money on in the past 5 years.

Hi Jeff, there is a relation to why i reference 5 years. I listen to all your podcast not just here but at Todd Treissder and Entrepreneur on Fire and that i know you are pretty big on active management and peer to peer lending.

while highlighting caveats like this is extremely good, there is a concern that even for those more successful deals can originate because more of a luck factor (due to a rising tide) rather than the “EDGE”

by only doing it more than 5 years consistently gaining good result perhaps we can lay it down to competence.

the same for peer to peer as the better default result can be a manifestation of folks facing less problems. that could be rather different when another receission comes.

it will be good also to cover the different time cost required to gain a certain level of competency to consistently not make such problems.

Nice post and a helpful list. As I’m guessing that you might concur the message I convey to folks in or near retirement is that the biggest risk they face is not a loss from their investments its being too risk averse and running the risk of outliving their assets. I sure you noticed but TIPs funds really got slammed in Q2, a bit of an over reaction to the Fed, but none the less TIPs have done better over the past several years than the underlying economics of the instruments might suggest.

I too am interested in P2P lending. I guess I will have to get up off my butt and give it a chance vs. dragging my feet.

I didn’t know that there are as many low risk investments that can give high returns available before, I only knew mutual funds and money market funds and I don’t have any idea about the rest. Really helpful post, thanks Jeff!

I really need to start with P2P lending. It has just been tough for me to stop putting money into the stock market the last couple of years.

Good day sir,

I have been following your post for quite some time now and honestly speaking,am beginning to have a better understanding about the world of investment.

Sincerly speaking,am a newbie to the world of investment and I think that’s the reason I have made so many financial looses online.I realy want to ask “which Low risk investment would you recommend for some one like me with little capital” that grows steadily within a year or less?please do reply because I realy want to get out of the “rat race circle” Thanks alot

You mentioned steady growth within a year or less. The reality is that’s not how investing works. You can try to pick individual, undervalued stocks and sale when the price goes up, just beware of the risk involved and manage your account with any one of the many online broker site that were designed for such things. Aside from that, you should get in the habit of saving and not living beyond your means. If you’re not really saving now, start with what you can. $5 then turn it into $20 etc. Long term goals and then working backwards to put a plan in place to achieve those goals is the name of the game. It doesn’t happen in a year, it’s discipline and sound principles that stretch over the course of twenty, thirty years plus. Diversify and protect yourself along the way. Hope this helps.

US SAVINGS BONDS via www.TreasuryDirect.com

Sad to see the ease in purchasing a paper bond at local bank has been discontinued.

With the “intricacies” of having to purchase online via TreasuryDirect, move paper bonds to on-line account, I fear far too many grandparents gifting will eventually cease. Even the parents tend to shy away from using as is so complicated.

Should you pursue, ensure you read & I recommend print a copy of the 13 page instructions; even then all is not clear when multiple changes are being made. I must adminth The Wizard was of benefit in capturing the data.

However, if a wrong date of purchase is entered, Treasury Direct is not set up to detect this. Though it will detect if Bond # does not match the Type or Denomination. Interesting! If not identified at entry point, then might it be overlooked at time of “cashing in”? USE CAUTION WHEN ENTERING YOUR DATA.

I’m a big fan of P2P lending. So far this year, my net annualized return is over 15%. I’m really hoping I can maintain those numbers over the long term.

I have been looking at this as well, however, since I’m in Michigan, I can’t do it!

Jeff, I am glad you included p2p lending on this list as a middle risk investment (and thanks for linking to my article by the way). With Lending Club hitting $1 billion and becoming cash flow positive I don’t think it should be considered a high risk investment. I think it is the best risk/reward investment available today – one where double digit returns are quite possible.

@ Peter The more I dig into p2p lending the more I get excited about it. Especially considering the recent pull-back in the market. My Lending Club account has returned a consistent > 9% return since 2008. I’m also going to open an account with Prosper, too; just haven’t had the time.

For my clients that are more online savvy, I encourage them to at least look at and consider p2p lending as a part of their portfolio.

Just how volatile have the markets been the last two months? Would you be surprised to know that August and September 2011 rank amongst the top 5 most volatile periods in the last 50 years? I was. I knew things were bumpy but I didn’t realize they were Top 5 bumpy.

Great article! just wanted to comment that its also a great idea to reallocate your investment portfolio during volatile times. Keep up the goof fight Jeff and Miranda!

Great post. Thinking long term is important, especially if you are dealing with a retirement account. Creating a long term plan that fits your risk is key.

Recent international political instability, it is very risky.

Its OK if you buy high but never sell low.

As always, good advice Miranda! I was hoping that I wouldn’t read anything in the article about trying to “time” the market, and I’m happy to see you’re one of the few that doesn’t try to go down that road.

I’m a strong believer in “market efficiency” a accept that virtually all bad news and good news available (either through research or statistical analysis) is already reflected in the current financial market.

Investing in healthy growth and value companies over the long haul along with the other suggestions you’ve offered, is the only realy “sure fire” way of getting through this volatile period.