For many people “budget” is a six-letter dirty word, but it doesn’t have to be.

You may be aware that you need a budget to help you reach your long-term financial goals, but many people don’t know where to begin to create an effective budget.

A budget is one of the most critical financial tools you can wield.

Everyone can benefit from having a defined budget, no matter their age or income.

How you manage your money dictates how you live your life, and it will either hinder or help you to reach your dreams.

Whether you’re on the brink of bankruptcy, examining your estate plans, or suppressing your spending, I’ve got you covered.

Read on for my guide to managing your money every step of the way.

Table of Contents

First, Let’s Talk Money Management MISTAKES (So You Can Avoid Them)

First things first, let’s talk about the top 5 mistakes people make when it comes to managing their finances so you can keep as far away from them as possible.

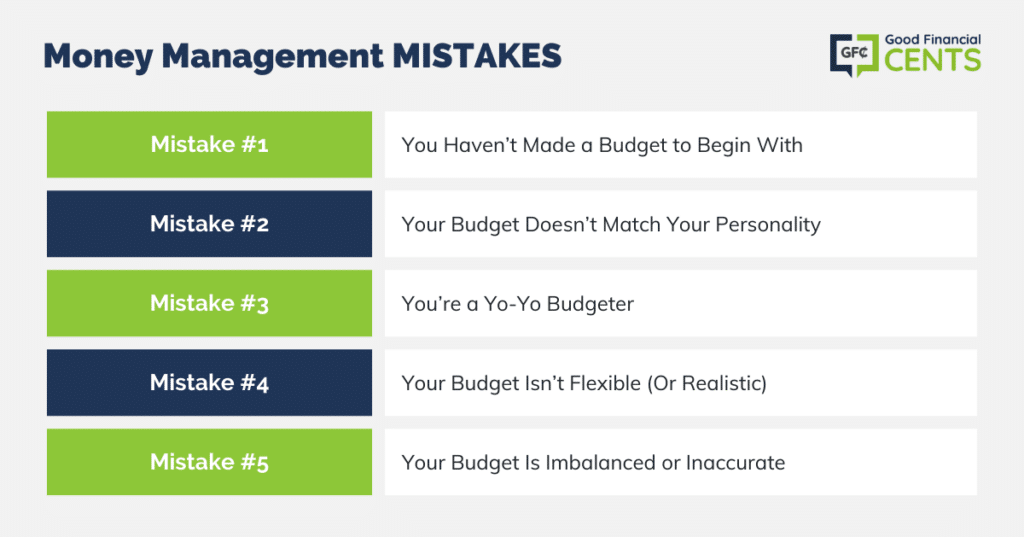

Mistake #1: You Haven’t Made a Budget to Begin With

According to a 2022 Gallup report, only one in three people creates an extensive budget (even fewer actually stick to it), which means two-thirds of Americans have no idea where their money is going.

Not keeping track of your money is one of the most dangerous financial mistakes you can make.

With a plan in place, you can avoid the pitfalls related to spending more than you earn.

There are a number of underlying reasons people don’t create budgets, one being the assumption that budgeting is too difficult.

Luckily, with financial advisors like myself offering advice and recommendations for free budgeting tools, creating your own budget is easier than ever.

Along those lines, people avoid budgeting like the plague because, even with the aid of streamlined budgeting services, it takes time and effort.

It’s easy to fall into the trap of putting your budget off until tomorrow, which, as you know, never comes (otherwise, you’d have a budget).

Even if your current income is substantial, ends are meeting, and debt is getting paid down, you need a budget.

Life can change in an instant, and if you aren’t budgeting, your finances aren’t secure.

It’s as simple as that.

Convinced yet? Let’s move on.

Mistake #2: Your Budget Doesn’t Match Your Personality

In order for a budget to work, it has to fit your personality and lifestyle, and your family’s.

If you have a more casual attitude about money, completely denying yourself any cash for free-spending purposes could doom your budget.

You may have to allow at least a small percentage of the budget for discretionary spending.

Keep in Mind

Without going too far, you have to partially construct your budget around preferences – yours, your spouse’s, and even your children’s.

Mistake #3: You’re a Yo-Yo Budgeter

Perhaps you’ve heard of the term yo-yo dieter, a person who has a long history of on-again, off-again dieting (I’m the perfect example since I go from strict paleo one week to chowing down six doughnuts the next.)

Though they have a desire to lose weight, they lack the will or the discipline to stick to it.

What makes this trend even worse is the fact that yo-yo dieting can actually cause the dieter to gain more weight than they lose over the long term.

The same could be true of you when it comes to budgeting.

You have a strong desire to get control of your finances, but you lack the discipline and/or the commitment to implement a budget and stick with it for more than a few months, or even a few weeks.

And, much like a yo-yo dieter, a yo-yo budget can leave you in worse financial shape than when you started.

Though you may be able to lighten your budget after a year or so, when you first begin you’ll have to be very strict – something like a Budget Boot Camp – which will force you to make radical changes in your life.

But even if you get past the Boot Camp phase, you still have to retain the basic elements of your budget for the foreseeable future.

No backsliding is allowed!

Mistake #4: Your Budget Isn’t Flexible (Or Realistic)

Since expenses tend to rise and fall from one month to the next, your budget will not work if there isn’t a certain amount of flexibility built into it.

When there is a surplus in your budget, bank it to have it available to shore up the months when your expenses are higher than normal.

Some months simply have more expenses than others, and they seem to come out of nowhere.

In other months you can actually fall off the wagon – you spend more than you should, and it puts you in a bit of a hole.

That’s actually normal; as long as it doesn’t happen too often, and as long as your budget has enough flexibility to work around it, you’ll be fine.

Just make sure you aren’t constantly relying on the flexibility of your budget to continue those bad spending habits.

Likewise, plan for contingencies.

While it’s fairly easy to build a budget around fixed monthly expenses like your house payment and debt payments, you still have to make an allowance for contingencies.

For example, if you are driving two cars and both are over five years old, you should make a monthly allowance for car repairs, even (and especially) in the months when none are required.

Mistake #5: Your Budget Is Imbalanced or Inaccurate

Budgets need balance.

If you’re spending too much on certain expenses and not enough on others, the imbalances can eventually cause you to abandon the budget entirely.

For example, If you are allocating too much money to pay off credit card debt and not putting any money into savings, or spending too little on groceries, you could be sabotaging your budget.

If you want to make your payments more effective, take out one of the best credit cards for balance transfers and zap that debt into oblivion with 0% interest for a year or more.

Maybe you can get along without balance for a few months, but if it takes a couple of years or more to pay off your credit cards, you will more than likely abandon your budget long before that happens.

On the opposite end of the spectrum, you might need to scale back your entertainment and miscellaneous budget to pay off debt and cushion your savings account.

If you’re spending more than you’re making, creating a budget and trying to live within it is a complete waste of time. You have a more fundamental issue that will have to be resolved first.

If your expenses are higher than your income, you have three choices:

- Cut your expenses.

- Increase your income

- Use a combination of both.

Once you get your income and expenses in balance, then you’ll be ready for a budget.

How To Budget for Everyday Life

How you budget is totally dependent on your unique circumstances, needs, and financial goals.

Whatever stage of life you find yourself in, read on for my tips for managing your money like a pro.

If you’re the average person looking to take charge of your finances, here are the steps you need to take to get on the path to success.

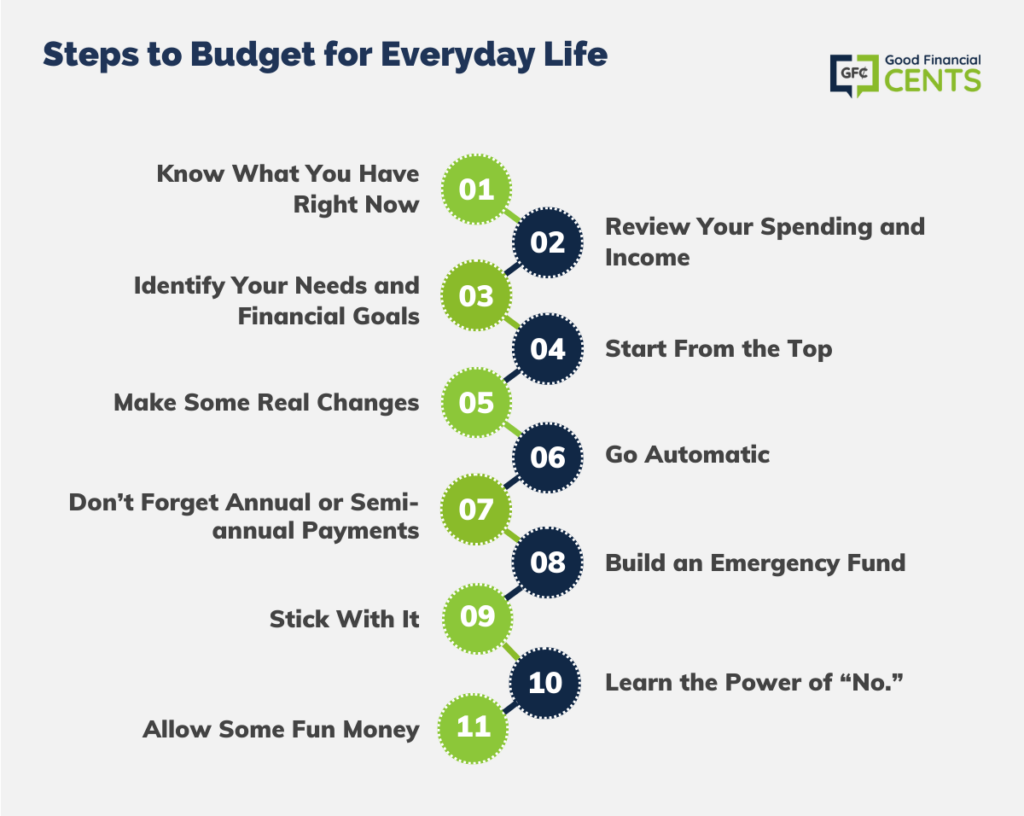

1. Know What You Have Right Now

The first step in creating a budget is understanding where you are right now.

Look at all of your banking accounts, credit cards, debts, buried jars of money in the backyard, and any sources of income.

You should also spend at least one month tracking all of your spending and see where your money is going.

You can get a better idea of larger trends, though, if you follow your money for two or three months.

You can use a ledger or notebook to record income and expenses, but it might be easier if you use personal finance software or sign up for a free budget application.

Assign each expense to a category. (Be sure to track the cash you spend, as well as purchases made with debit and credit cards.)

If you have a smartphone, tracking your spending has never been easier.

Apps like Mint and Personal Capital make budgeting as easy as looking at your phone.

The apps will connect with your bank accounts and credit cards and automatically separate your spending into different categories.

They’ll then display your spending habits in easy-to-read graphs.

2. Review Your Spending and Income

After you have taken the time to track your income and your expenses, it’s time to review how your money is moving through your bank account.

Look at the categories where you are spending the most (it might surprise you!).

Reviewing your spending will help you identify areas of concern before you make your budget, as well as help you realistically allocate where your money should go each month.

If you’re spending more than you earn each month, you’re not alone. A review will help you see where you need to cut back and get back in the black.

Just knowing how much you’re spending in certain areas can have a huge impact on your finances and give you the ability to rein in some overspending habits you might not have known about.

3. Identify Your Needs and Financial Goals

Next, you need to determine what your needs are. These are items you can’t live without (a new TV doesn’t fall into the “needs” category).

You should make sure your budget first covers items like food, shelter, and clothing, as well as transportation to work.

Also, recognize your obligations and bills.

Make sure debt payments are made, as well as utility payments and other important obligations.

You should also designate some financial goals.

Each person will have a different set of financial goals depending on their financial situation and their desires.

You will be more likely to stick with a budget if it helps you reach your financial goals.

4. Start From the Top

When you create a budget, it becomes obvious that you need to make choices.

Before you budget for wants like entertainment, you need to make sure needs and financial goals are covered.

List all of your needs and wants in order of importance.

Your food, clothing, gas money, etc. will all be at the top, and things like buying a pool will be at the bottom.

Be realistic.

5. Make Some Real Changes

The good news is, you’ve created a budget. The bad news is, that it’s probably going to be wrong.

More than likely you have overestimated in some spending areas and underestimated in other areas.

But don’t worry…

The longer you stick with the budget, the better you will become, and guessing how much you’ll spend in all the categories.

After you have created your budget, it should not be set in stone.

Think of your budget as a fluid, living creature you should continue to review and adapt as your life changes.

6. Go Automatic

If you have trouble saving money, the best way to ensure that you stick to your savings plan is to make your savings automatic.

With just about every bank account, you can create an electronic money transfer which will take money from one account to add to a savings account.

This is an excellent way to prevent you from spending the money you should be saving.

You can schedule these transfers to happen at any time, but it’s best to do it shortly after your regular paycheck is deposited.

7. Don’t Forget Annual or Semi-annual Payments

Budgeting for recurring expenses is easy.

Things like power bills, gas money, and water bills are hard to forget, you pay them every month, but don’t forget about those expenses that only come around once or twice every year.

These expenses could be car insurance payments, health insurance, membership fees, and more.

If you have anything like this, build these costs into your budget but divide them into monthly payments on your budget.

If you pay your car insurance bi-annually, then divide that number by six and start saving for it every month.

8. Build an Emergency Fund

One of the most common problems people face when making a budget is not having an emergency fund built in.

Because you can’t see into the future, it’s impossible to budget for all of your expenses every month.

You never know when a pipe is going to bust, your car will need repairs or a heater will go out.

Without having money saved for emergencies, any unexpected expenses can completely derail any good budget.

Many financial experts agree that an emergency fund should be around $1,000-$2,500 to account for any financial surprises.

Having a separate account for your emergency fund will help prevent you from spending it on accident (or on purpose).

9. Stick With It

Don’t create your budget and then forget it.

Creating a budget is important, but using it is more important.

Put your budget in a place where you will see it every day.

Print it out and tape it to the fridge or your front door.

You don’t have to review it every day, but knowing it’s there is important and keeps it front of mind.

If you become frustrated with sticking to your budget or begin to feel deprived of enjoying certain things, remind yourself of the financial goals you’ve set.

If you’re saving for a new car, put a picture of the car out to encourage you to stick with the budget.

10. Learn the Power of “No.”

Being on a budget means you will have to say no to spending sometimes.

You may have to say no to your favorite type of junk food at the store, going to the movies, or going out to lunch with your coworkers.

Being disciplined and learning to say “No” to some of your wants is one of the most important budgeting skills.

Having a budget is great, but it’s useless unless you stick to it.

11. Allow Some Fun Money

Who said budgets can’t be any fun?

Make sure you include a few bucks at the end of your budget as “blow money” or “fun money.”

Having the extra spending money makes sticking to a budget a little easier.

Learn to treat yourself from time to time with this extra money (but don’t spend more money than you’ve budgeted).

About Climbing Out of Debt…

If your main money management goal is to get out of debt, you’ve come to the right place.

There are a series of steps you can take today to get on your way to reaching financial freedom.

The basic budgeting tips above are the place to start, but if you’re in debt, you have a few additional steps to take.

Consolidate or Refinance

Once you’ve taken a hard look at all of your debt, you may find yourself wondering if there is a way to lessen the load before you start paying it off.

One way to lighten your burden is refinancing.

If mortgage rates are better today than they were when you purchased your home, you could save by refinancing.

Is student debt suffocating you?

With a site like SoFi or LendEDU, you may be able to refinance your private student loans to get better interest rates and more reasonable repayment terms.

You can also consolidate your debt, combining your personal loans and credit cards to get lower interest rates, which will speed up your detour from debt.

Get a 0% APR and Balance Transfer Credit Card

Get the card, transfer all your high-interest debt, and crush it during the APR-free period.

Choose an option like the Discover It® card and you’ll get a 21-month APR-free period, plenty of time to get to work on your debt.

In addition to paying off your debt, you can earn some awesome rewards on your purchases with the card, which can also be used to pay down your debt.

It’s a win-win!

Debt Snowball

The go-to method of debt repayment proposed by finance guru Dave Ramsey is straightforward and motivating, with tangible results.

Here’s how it works:

1. Make a list of your debts, starting with the lowest balance and ending with the highest (minus your mortgage), and list the minimum payments and remaining balance.

2. Pay the minimum on all but the lowest balance items.

3. Then use all the money you budgeted for your higher payments to knock out the lowest one.

And repeat until you’re debt-free.

While it might not technically be the quickest method, it’s hard to argue against it being the most motivating.

Like a snowball, your debt repayment picks up momentum and takes off.

Debt Avalanche

The debt avalanche takes a slightly different approach to debt repayment, encouraging you to tackle your debt in order of interest rates rather than balances.

You pay everything you can on your highest interest rate rather than your highest balance and make minimum payments on the rest.

This track to financial freedom will take longer, but you’ll save more money by tackling your highest interest first.

Curbing Your Spending

If you’re trying to cut back on your poor spending habits, I have some surefire strategies to help you succeed.

1. Know your wants and needs.

Yes, you need food to survive, but what food?

Getting takeout twice a week is not a need.

You can reduce your grocery bill by planning healthy meals and cooking at home.

Be honest about where your money is going, and be realistic about your adjustments. These moves aren’t always fun, but they are necessary.

Some financial experts say you waste as much as 15% of your income each month (do you really need that cup of coffee every morning?).

The money is probably there, and a budget can help you put it to better use, providing you with a solid foundation for a better financial future.

2. Be an intentional shopper.

Every dollar that comes into your possession should have a destination in your budget.

To help you achieve your zero-based budget, you need to be intentional with every one of your purchases.

Have you ever gone to the grocery store with no list and walked away with a cart full of junk food and a dent in your budget?

So have I.

Something as simple as making a grocery list and sticking to it can be a game changer.

The more specific you can get with how much your non-essential purchases will cost, the easier it will be to stick to your budget.

Think less whimsical, more willful.

3. Get practical.

When you’re having problems sticking to your spending limits, it’s time to start “cash envelopes.”

With the cash envelope system, all you’ll need is several large envelopes to put money in.

Designate each envelope as a different expense, i.e. a gas envelope, groceries envelope, entertainment envelope, etc.

The money you put in each envelope is the allotted amount you are allowed to spend on that category for the month.

Once the money is gone, you have nothing left to spend in that category.

Cash envelopes are one of the best ways to live within your budget.

As many financial professionals suggest:

Any area that you continually overspend should be switched to cash envelopes.

4. Period.

This is a concrete way to follow your budget and keep track of your spending.

Budgets are awesome. They bring order to chaos, sanity to spending, and freedom to your finances.

In a perfect world, you could budget for everything. But in reality, life happens unexpectedly.

Otherwise, there would be no need for emergency funds.

Read on for advice on dealing with the unexpected that your budget just can’t cover.

Battling Bankruptcy

When you burst onto the entrepreneurial scene, you probably didn’t plan to one day file for bankruptcy from the debt your business incurred.

Or plan for your family to be hit with a devastating illness that sends your medical bills through the roof.

Nor did you expect you and your spouse to lose your jobs almost simultaneously with a mortgage, credit card debt, and student loans beating down your back door.

But life happens.

If you’re facing financial ruin and considering bankruptcy, here are a few factors to think about:

- Bankruptcy can wipe your slate clean, releasing you from having to repay your debts. It gives you the ability to start anew with your finances and blocks creditors from approaching you.

- But bankruptcy doesn’t erase your debt overnight. Most people file for Chapter 7 Bankruptcy, which can take around 6 months to process. And some bankruptcy plans take 5 years.

- And it only applies to you. The aim of bankruptcy is discharge, your legal release from paying back your debts. Notice I said your release. That highly desired debt discharge frees you but not your cosigners, unless they file for bankruptcy, too.

- Filing for bankruptcy is complicated and costly. Shocker, right? As you might guess, the homework is a headache. And if you need a lawyer to help you muddle through the jargon, you could be spending thousands of dollars.

Plus, filing fees can be substantial, and you have to meet a low-income percentage to obtain a waiver for the fee.

- Bankruptcy bares it all. Are you ready to go public with your finances? When you file for bankruptcy, your financial information is exposed and you’re responsible for answering extensive questions about your financial history. Your hearing will probably be a public proceeding, so be prepared.

- Your financial future is at stake. While bankruptcy does free you from your past debts, it hinders your ability to access credit in the future, might halt you from buying (or renting) a home, and can bar you from getting hired by private sector companies (many apps ask if you’ve declared bankruptcy in the last 7 years).

- You have to be honest. If you do decide to file for bankruptcy, the most important component to your application is honesty.

If you misrepresent your finances when you file, your request could be declined. Or worse, your discharge could be revoked if dishonesty comes to light later, leaving you bankrupt without the benefits.

Generally, bankruptcy is not the solution I recommend for dealing with debt, but what if you’ve already filed and find yourself in the limbo I like to refer to as a credit timeout?

If you’re currently bankrupt, take this time to budget wisely with the tips above.

Track your dollars to a “T” and come out of your debt discharge with savings and solid credit.

You can do it!

Expecting Legal Expenses

What if you’ve kept track of your finances over the years and paid down your debt responsibly but unexpected legal expenses hit?

Let me give you a few legal expenses that could (but hopefully won’t) befall you.

Divorce

10 years ago, you skipped down the aisle in wedded bliss, now you’re trudging to the court in a dreaded divorce.

The dissolution of marriage impacts more than your love life, as anyone who’s divorced knows.

Here are a few costs to expect, some weightier than others:

- Legal Fees. The act of legally ending your marriage will come at a cost. How much depends on a number of factors. If you decide on a DIY method of filing, you could pay less at the moment but more in the long run if you’re unfamiliar with all the legal terms.

With an internet service, you pay a little more. With mediation, you’ll be paying a substantial amount more. With litigation and a lawyer in place, you’ll be potentially paying tens of thousands of dollars.

Do your research and weigh your legal needs with your financial situation to find the best option for you.

- Alimony. Alimony is a scheduled payment plan providing spousal support. It’s tax deductible for the payer and taxable income for the payee.

Alimony is usually centered around both individuals’ earning potential and secondarily considers the length of your marriage, the reason for the divorce, etc.

Oftentimes, alimony is paid to a spouse who can’t work because they will be primarily raising the children. It is usually temporary and gets adjusted based on changes to earnings.

- Child support. Unlike alimony, child support is not based as much on earning capabilities, the length of the marriage, or the division of property. Instead, it is doled out with the goal of maintaining your child’s quality of living after divorce.

You and your spouse’s incomes are weighed, plus child care expenses and medical or educational costs, like treatments, medications, or private school tuition. Whether you’re on the giving or receiving end of child support, be mindful of how it will impact your finances.

Manage your post-divorce debt with the budgeting tips here and land on your feet.

Legal Settlements

You might not think yourself to be the typical target of a lawsuit, but here’s the truth.

Whether you’re a billionaire or a babysitter, if an unfortunate situation unfolds under your eye, at your hands, or on your property; innocent as it may be, you could be at fault legally.

Rather than start with a list of awful scenarios (we’ll get to those in a moment), I’m going to start with the good news.

Insurance

Although litigious cases aren’t always something you can account for and cover, there are some affordable ways to protect yourself.

Beyond the basics of required policies like auto, renter’s, and homeowner’s insurance, you can buy an umbrella policy to extend your coverage.

You should also purchase homeowner’s or renter’s insurance to cover your property in the event that someone sues you for what happened on your property.

Let’s look at a few situations covered by umbrella insurance, a list that should give you an idea of some legal costs you could be held responsible for in court:

- Bodily injury liability: if your neighbor’s brother’s friend slips on your deck, your dog bites the mailman, or you cause a car accident where someone is seriously injured, you’re at risk of paying for their bodily injuries unless you’re insured.

If your renter’s or car insurance caps off at $200k, you can supplement that amount with an umbrella policy.

- Property damage liability: if you (or your kids, or your pets) are responsible for damage to someone else’s property, like their car, building, or priceless antique vase, you could be picking up a colossal bill to repair or replace what’s damaged.

- False arrest: You’re on your honeymoon with your new hubby. When you get pulled over in the rental car, much to your surprise, the previous renters left a few baggies in the console(not the wedding gift you expected!).

The police assume it’s yours, you two spend your first night in jail, and your legal fees aren’t covered by the rental company’s insurance. It may sound far-fetched, but scenes like the one I just painted happen pretty frequently.

- Libel: This one’s a bit simpler to explain. Write something negative about a person or company that damages their reputation, and you could be sued.

- Rental Property Owners: If you own an apartment complex, vacation rental, or any other property you rent out, you could be responsible for an injury on that property, like your tenant’s neighbor’s brother’s friend slipping on the deck and winding up with hefty hospital bills.

- Slander: Much like libel, if you say something injurious about another person or party, you could be going to court.

- Shock and mental suffering: If someone claims anguish at your hands, due to something you said or did, or from an accident you caused, they can pursue legal action. Whether their case holds or not, legal fees are high, and you might need some coverage to protect you.

Those are the primary categories of umbrella insurance coverage, but here are a few more places you could incur legal costs in court:

- Discrimination or harassment: Among a host of other claims, if you are a business owner or employer, you can be sued for discriminating against your employees or for harassment that takes place at your company.

Business insurance is a great way to account for these lawsuits which occur often.

- Interference: If you interfere with, say, a contract between individuals and companies and it affects their business negatively, you could be sued.

- Protesting: If your activism carries you to someone’s property, you could be sued for a number of claims, whether things go awry or not, like trespassing or conspiracy.

No one is completely safe from legal liability. At the very least, make sure your auto insurance and homeowner’s or renter’s insurance is substantial.

If you’re wealthy and your daily business dealings put you at an added risk, you might want to invest more in protecting your assets.

And if you’re a landlord or business owner, you absolutely need to consider an umbrella policy to provide the additional coverage you need.

Budget wisely. If you would benefit from a policy offering legal protection, do your research, get quotes, and add affordable coverage to your expenses.

Mapping Out an Estate Plan

One of the most important preparatory financial steps you can take is estate planning.

Here are some basic steps involved in estate planning:

- Choosing a guardian for your children.

- Determining who will be the executor of your will.

- Gathering information on the specifics of your retirement plans and investments.

- Writing a will.

- Establishing trust accounts for each of your beneficiaries (it will protect them from taxes!).

- Detailing your funeral plans.

- Designating any non-profit organizations or foundations to be donated to in the future and the amount to be given.

- Crafting your living will.

- Working to pay your estate taxes and debts.

Planning for your imminent death may be morbid, but it’s the best way to ensure your spouse and descendants receive the inheritance you have in mind for them.

I have loads of advice on the best life insurance and investment strategies to benefit your estate and your descendants the most.

We never know what tomorrow holds.

Do your research and start thinking now about your will and who would best serve as executor.

Managing an Inheritance

Maybe you aren’t trying to leave an inheritance, but figuring out how to spend one you’ve just been given.

It’s a wonderful feeling when a windfall of money lands in your lap, but it can also be a daunting one.

Maybe you’re on top of managing your expenses, or maybe you aren’t.

Either way, adding tens or hundreds of thousands of dollars to the equation at once and deciding where they fit is complicated.

How exactly you distribute your newfound funds depends on your situation, but overall, there are a few do’s (and don’ts) when it comes to managing an inheritance.

What to Do With Your Inheritance

- Pay down your debt. If your goal is to be debt-free, contribute some of your inheritance to that goal, especially if you have multiple sources of debt or debt with high interest.

- Invest. I’ve written tons of helpful content on how to confidently invest your money. The possibilities are endless. A great place to start investing is a Roth IRA.

With a Roth IRA, your retirement will be yours tax-free one day and you aren’t harshly penalized for borrowing from the account before its maturity like you are with other plans.

- Diversify your portfolio. While a Roth IRA is a great place to start, don’t stop there. Diversify your investments by placing money in a multitude of places like retirement, CD laddering, and high-yield online savings accounts.

- Stock your emergency fund. If you build up enough funds to sustain you for 6 months, you’re off to a great start. If you want to be really secure, shoot for a year’s worth of income.

- Make a difference. If tithing plays a part in your life, give 10% to your church. Is there a cause you’re passionate about? Giving part of your inheritance to a charitable organization is a meaningful way to steward it. Make an impact with your money!

- Leave an inheritance. If your budget, debt repayment, and emergency fund are all on track, or if you just want to leave to your children what was left to you, consider sharing the love and rolling your inheritance into theirs.

What Not to Do With Your Inheritance

- Don’t rush. There’s no need to. If you need time to process the details and research your options, place your inheritance in a short-term account like a CD or high-yield savings account while you decide.

- Don’t buy new stuff when you haven’t paid for the old stuff. This should go without saying, but if you’re $50,000 in debt, you don’t need to run straight to the dealership for a new car.

Hold off on major non-essential purchases while you can and try investing and saving instead. Spend and enjoy some of your inheritance, by all means, but don’t go crazy.

- Don’t trust just anyone to manage your money. Not all financial advisors have your best interest at heart. If one pushes you to invest right now and all in one place, they don’t update you on your account, or they adamantly push you past your risk tolerance, look elsewhere.

These are just a few warning signs you need a new financial advisor. Be wary, be wise.

- Don’t take a one-size-fits-all approach. Just because one saving or investment strategy might be solid for your sister’s inheritance doesn’t mean it’s the perfect path for you. Look at your current finances and future goals to decide how to put your money to work!

Tackling Taxes

When tax time comes, are you cool and collected or frazzled and frantically trying to file on time?

With a federal income tax guide, you can determine how you should file and know exactly what information you’ll need to provide.

Beyond your income, here are 10 taxable items you may not be aware of:

- Annuity earnings: If you buy your annuity with pre-taxed money from, say, your IRA, it is 100% taxable. Buy an annuity purchased with post-tax money and part of your return will be tax-free.

- Capital gains: When items like property, stocks, bonds, and precious metals are sold for a profit, they’re taxed.

- Dividends: Based on your tax bracket, qualified dividends are taxed at set percentages.

- Gifts of securities: Shares, stocks, and bonds given as gifts can be taxed.

- Interest accrued on bonds, notes, and treasury bills: It’s taxable.

- Market discounted bonds: These are taxed the year they sell as regular interest income.

- Municipal bond interest: Interest accrued is federally taxable but state and locally tax-free.

- Mutual funds: Dividends and interest can be taxed in a taxable account, with tax-deferred earnings staying safe as long as you don’t touch them.

- Retirement funds: SEP, Simple IRA, and ERISA policies are taxable under income.

- Step-up in basis: Assets tend to appreciate over time, and in those cases, a step-up in basis can help lessen the capital gains tax on that growth for the beneficiary.

With an understanding of how your funds are taxed, you can invest wisely and save money on taxes.

Resources

Ready to get started?

I’ve dedicated years to researching and reviewing the best tools on the market to help you thrive.

There are tons of apps for everything from budgeting to investing to filing taxes.

Take a look at some of the awesome resources I’ve compiled to manage your money like an expert.

Bottom Line: How to Create and Maintain a Monthly Budget

With your newfound money management expertise, you’re on your way to financial success.

What are you waiting for?

Use the tools above and start making gains with your money management today.

Budget really can be a six-letter dirty word. There is so much to consider. But when you have control over all aspects of spending, it’s amazing how much you can save. Thank you! Your article is one of the most detailed I have found on the web.