Eating disorders are a common mental ailment in the United States, especially among adolescent girls.

If you’ve suffered from an eating disorder like anorexia or bulimia in the past, it’s going to come up when you apply for a plan.

Regardless of your past, you can qualify for a life insurance policy. We don’t care what condition you may have suffered from, we want you to get a plan you can afford.

Table of Contents

Life Insurance Underwriting After an Eating Disorder

As you can probably guess, they are going to ask you several questions about your eating disorder. Some of them will include:

- Were you diagnosed with anorexia nervosa and/or bulimia nervosa?

- How many episodes of eating disorders have you had?

- When was the last episode?

- Has your weight been stable for at least one year?

- Do you have any other mental conditions like depression, anxiety, alcohol/substance abuse, or psychotic disorders?

- Are you taking any medications to help with your eating disorder?

While there are no medications to cure an eating disorder, applicants may be taking anti-anxiety or antidepressants to prevent another episode. These medications could be insurable.

Your life insurance application is your chance to show that you’ve recovered from your eating disorder and that it’s under control. Be sure to make your application as complete as possible. If your application seems to be missing information, the underwriter could get nervous and decline your policy.

Life Insurance Quotes After an Eating Disorder

Before you can apply for life insurance after an eating disorder, you’ll need to have recovered from your condition. Generally, insurance companies will want to see that you have recovered and maintained a healthy weight for at least a year before they will give you a policy. More time will help your rating because it means you have less risk of a relapse.

Beyond your eating disorder, they are going to review a handful of other factors. Everything from your mental health to your hobbies. To give you an idea of the rating classes, here are some basic rate classes:

- Preferred Plus: Generally impossible for someone that had an eating disorder. Even if you are now in perfect health, insurance companies will still be too worried about a possible relapse to give out the best rating.

- Preferred: Possible in some cases. To qualify, it needs to have been at least 4 years since your past episode and you’re otherwise in perfect health and have no other mental disorders.

- Standard: This is the most common rating. To qualify, it should have been at least four years since your last episode and you are in generally good health. It may be possible to get a standard rating with small health problems like being a bit overweight or having slightly high cholesterol.

- Table Rating (substandard): Applicants who apply within two to four years of their last eating disorder episode will likely get a rated policy. The longer you wait, the better your rating will be. You could also get a rated policy if you have recovered from your eating disorder but still have some other mental or health issues.

- Declines: Applicants who apply while currently suffering from an eating disorder will be declined. Most applications within one year of an episode will also be declined. Your application could also be declined if you are still suffering from other mental issues like depression or if you have some significant health problems that would be made worse by an eating disorder relapse.

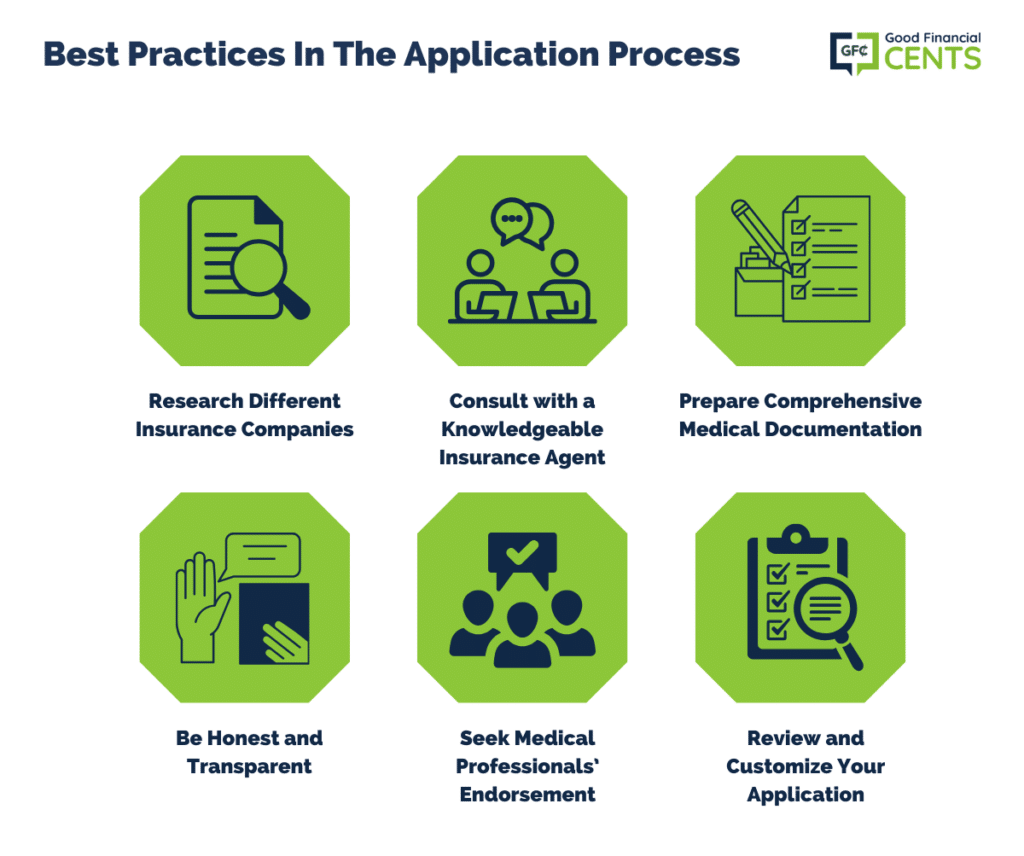

Best Practices for Application Process of Life Insurance With an Eating Disorder

Applying for life insurance can be a daunting process, especially when you have a history of an eating disorder. Here are some strategic tips and best practices to help simplify the application process and increase your chances of approval:

- Research Different Insurance Companies: Look for companies that specialize or are experienced in handling cases with a history of eating disorders.

- Consult with a Knowledgeable Insurance Agent: An agent who understands your unique needs can guide you through the application nuances and suggest the most suitable policies.

- Prepare Comprehensive Medical Documentation: Gather all necessary medical records and documents, including details about your eating disorder, recovery process, and current health status.

- Be Honest and Transparent: Fully disclose all relevant information regarding your health, ensuring that there are no discrepancies in your application.

- Seek Medical Professionals’ Endorsement: Consider obtaining a letter from your healthcare provider that explains your recovery journey and current health status in detail.

- Review and Customize Your Application: Tailor your application to highlight your recovery journey, ongoing health maintenance, and overall wellness.

Adopting these practices can demystify the process, positioning you more favorably for policy approval and suitable coverage terms. Remember, persistence and thorough preparation are key to navigating the life insurance application process successfully.

Eating Disorder Insurance Case Studies

What does all of this mean to you? You might be confused about the rates you’ll get. To help you make sense of all this, we wanted to share some stories of clients we’ve worked with in the past.

Case Study: Female, 32 y/o, suffered from bulimia nervosa at 23, recovered at 25, applied for life insurance at 26, and was rejected

This applicant was bulimic when she was 23. After a couple of years, she made a full recovery and never relapsed. Within a year of recovering, she tried applying, but she was declined. At this point, she thought her past eating disorder would make it impossible for her to get coverage. We showed her this wasn’t true.

We showed him a carrier that regularly deals with applicants who had eating disorders in the past. This helped because the new company was better able to evaluate her application. By applying again at 30, this applicant was able to receive a standard rating.

Case Study #2: Female, 40 y/o, suffered from anorexia nervosa in her teens, relapsed at 24, fully recovered at 26, and had no other relapses, currently taking antidepressants, in great health

This applicant was struggling with depression in her teens and this caused her to become anorexic. She recovered but then relapsed again at 24. After regularly meeting with a therapist and starting to take antidepressants, the applicant made a full recovery. Since then she has been in great health, though she still takes antidepressants and sees her therapist from time to time.

She applied and was accepted for coverage, but she got a rated plan. It’s better than nothing, but we thought she could get cheaper rates. To do this, we told her to get a note from her doctor to send to the insurance company. The letter from her doctor explained her improved health and all the changes she had made.

After she did this, she got a standard-rated plan.

We show you this to give you an idea of what you can expect and to show you that you can get affordable protection, even if you’ve struggled with an eating disorder in the past.

Life Insurance With an Eating Disorder

Suffering from an eating disorder can be both physically and mentally damaging. But if you’ve overcome your eating disorder, then you can still get a cheap life insurance policy to protect your family members.

Insurance companies increasingly recognize the strength and determination of survivors. So, while the past might have presented hurdles, the present offers opportunities to obtain an affordable life insurance policy. This step is crucial, ensuring that one’s family remains financially secure, honoring the hard-won battles against eating disorders.