Being diagnosed with prostate cancer can make getting life insurance seem impossible. However, depending on your specific situation, finding good quality coverage with a highly-rated insurer is still possible.

American Cancer Society studies have shown that prostate cancer is the second most common type of cancer that affects American men today – and it is estimated that approximately one in six men will become diagnosed with this condition at some time during their lives.

The good news is that as medical treatment becomes more advanced and the survival rates continue to improve, the best life insurance companies will typically update their underwriting guidelines, making it at least somewhat easier for applicants to qualify for coverage.

Suppose you are in remission and your cancer is being successfully treated. In that case, a life insurance company may accept you for a policy with an additional premium surcharge – a flat extra premium cost.

Table of Contents

- Understanding Premium Surcharges After Prostate Cancer

- Benefits of Life Insurance for Prostate Cancer Survivors

- Prostate Cancer: Not a Barrier to Life Insurance

- What the Life Insurance Underwriters Will Need to Know

- Increasing Your Chance of Getting Approved

- Choosing the Right Policy and Coverage Amount

- Life Insurance With Prostate Cancer Questionnaire

- The Bottom Line – Life Insurance After Prostate Cancer

Understanding Premium Surcharges After Prostate Cancer

Navigating the complex waters of life insurance after a prostate cancer diagnosis can be challenging. One aspect that applicants often come across is the premium surcharge, which might be a temporary or long-term addition to your policy’s costs.

This surcharge is levied due to the perceived risk that insurers associate with insuring someone who has had a significant health scare, such as prostate cancer.

The rationale behind this is quite simple. Insurers try to balance the potential risk with the premiums they charge. Although treatments and survival rates have drastically improved with prostate cancer over time, there remains a certain level of risk from the insurer’s perspective.

It’s crucial to note that as time passes and if the cancer doesn’t reappear, many insurers often reduce or even entirely remove the surcharge, reflecting your improved health status.

However, this surcharge will be removed after a certain period – especially if you have become cancer-free. And, in certain instances, under ideal circumstances, you may even qualify for a “standard” premium rating on your policy.

Benefits of Life Insurance for Prostate Cancer Survivors

While the initial idea of paying an additional premium might seem daunting, it’s essential to consider the broader benefits of securing life insurance, especially as a prostate cancer survivor.

For one, life insurance offers peace of mind, knowing that your loved ones will be financially secure in the unfortunate event of your passing. Given the unpredictable nature of life and health, this is a solace that many families sincerely appreciate.

As a prostate cancer survivor, you also embody the resilience and determination to overcome significant challenges. Life insurance is a testament to that resilience, signaling to your family that you’re planning for their future, irrespective of past health challenges.

Moreover, in many cases, life insurance can also serve as a financial tool, offering benefits like loan collateral or cash value, depending on the type of policy you choose.

Prostate Cancer: Not a Barrier to Life Insurance

Many would think that having been diagnosed with prostate cancer would make getting approved for term life insurance coverage nearly impossible.

If that’s what you believe, let me be the first to tell you it is a myth. Men treated and diagnosed can get approved for a life insurance policy.

Recently, I encountered a 70-year-old male diagnosed with prostate cancer approximately 4 years ago. Six months later, he had a prostatectomy to have the tumor removed. Since then, he has had no metastasis, and everything seems to be in the clear.

He was looking to obtain a 15-year, $150,000 term life policy. It was time to do my homework.

What the Life Insurance Underwriters Will Need to Know

When moving through the life insurance application and approval process, the insurance company’s underwriters may request specific information in addition to that which is already included on the initial application.

This may consist of reports from your doctor, blood and urine testing, or even a third-party medical examination.

Likewise, should you be approved, several factors are likely to affect the amount of premium you will be charged. These criteria include:

- The stage and the extent of the cancer’s progression

- Your age at the time of diagnosis

- The type of treatment that you are currently receiving (if any)

- When treatment was completed (if applicable)

- Results of any follow-up medical testing

It is essential to remember that the less the underwriters know about your situation, the more likely they are to assume that you are a high-risk case – substantially increasing your chances of being denied coverage.

Therefore, in addition to following your doctor’s treatment plan, ensure you are ready with any additional information the insurance company requests.

This will give the underwriters a much more complete picture of your health history and your prognosis in the future. In addition, having this information upfront can also help in reducing underwriting delays during the overall application process.

Increasing Your Chance of Getting Approved

To increase your chance of approval for coverage, there are several steps that you can take. First, it is a good idea to consider working with a life insurance agent who has experience locating coverage for cancer survivors.

Often, agents will specialize in working with clients with health conditions that may make it more tricky to qualify for a policy. These representatives will typically know which insurance companies are more apt to provide the best rates for their client’s circumstances.

Choosing the Right Policy and Coverage Amount

Having a prostate cancer diagnosis in your medical history might initially limit some of your life insurance options. Still, with the right guidance, you can find a policy that fits your needs.

One key consideration is the coverage amount. This should ideally factor in your family’s living expenses, any outstanding debts, children’s education, and any other significant future expenditures.

Additionally, you might want to explore different policy types. Term life insurance, for example, offers coverage for a specified term, say 15 or 20 years.

On the other hand, whole life insurance offers coverage for your entire life while also building cash value.

Given your medical history, discussing your options with a knowledgeable insurance agent can provide clarity on the best path forward, ensuring you get optimal coverage without overextending your finances.

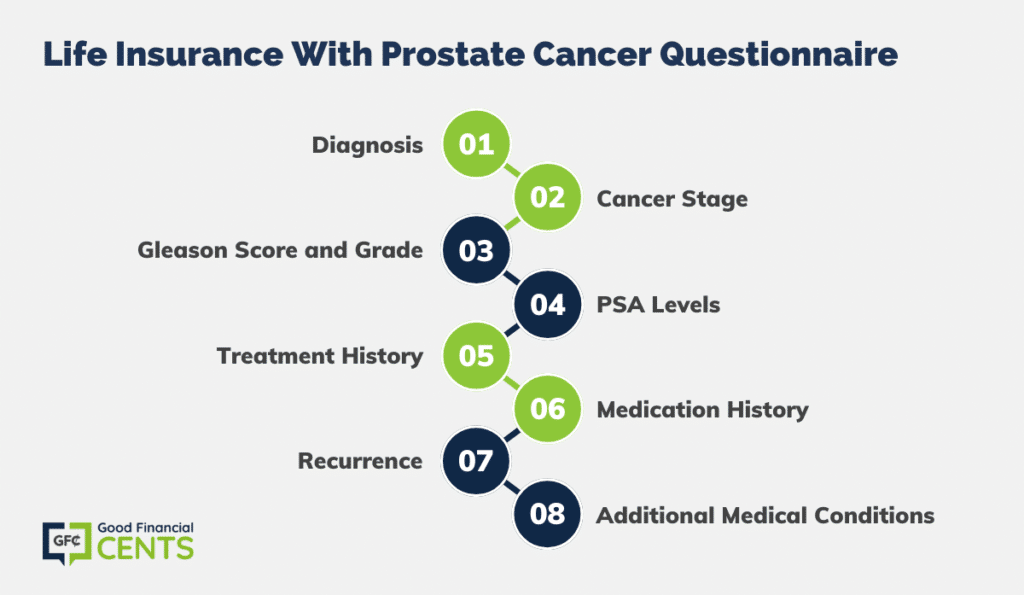

Life Insurance With Prostate Cancer Questionnaire

If you are interested in purchasing life insurance and have been diagnosed with prostate cancer, uncovering all the circumstances behind it is essential. Below is a sample questionnaire you’ll need to answer to ensure we get you with the best life insurance company.

1. a. Please provide diagnosis. b. Please provide the date of the last treatment.

2. What was the stage of the cancer diagnosed? This information should be contained in the pathology report.

A1, A2, B1, B2, C1, C2, D1, D2, Recurrent.

3. What was the prostate cancer’s Gleason score? What was the prostate cancer’s grade?

4. a. What was the PSA before treatment? b. What was the latest PSA?

5. How has the prostate cancer been treated?

- Observation only.

- Radiation therapy.

- Transurethral prostatectomy.

- Hormone therapy.

- Radical prostatectomy.

- Castration.

- Biological therapy.

- Castration (chemical)

6. Has the proposed insured taken any medications to treat the cancer in the past, and are they currently taking any medications?

- Name of medication(s), prescription(s) or otherwise.

- Dates they were taken or prescribed.

- Quantity, including dosage, taken.

- Frequency taken by day.

7. Has there been any evidence of any recurrence: yes or no?

8. Does the proposed insured have any medical conditions? If yes, please describe.

The insurance company will look at all these factors to determine how much of a risk you are to insure.

The higher the risk, the lower your chances of being accepted, and the more you’ll pay for coverage if you are taken. There are also dozens of other aspects that will impact your chances of being accepted for life insurance.

The Bottom Line – Life Insurance After Prostate Cancer

Like many other severe health conditions, prostate cancer is often a roadblock for many when seeking life insurance coverage.

The perception of high risk associated with such a diagnosis frequently deters individuals from considering the possibility of acquiring a comprehensive insurance policy.

However, it’s essential to remember that every individual deserves access to quality life insurance regardless of their health history.

Our dedicated agents are here to ensure that this remains more than just a belief; it’s a reality for many. They possess the expertise and understanding to guide you through the process, ensuring you’re not unfairly penalized due to past health issues.

Your health, especially past conditions, shouldn’t hinder safeguarding your family’s financial future. The core purpose of life insurance is to provide your loved ones with the financial resources they may need in your absence.

Hence, while it’s crucial to secure a policy, it’s equally important to ensure that the coverage amount is adequate.

An insufficient coverage amount, despite having a policy, can place undue strain on your family, almost equivalent to not having insurance. Always aim for a balance that aligns with your family’s financial needs and your budget.

I Was diagnosed with prostate cancer 2 years ago . A year ago march 3 ,2018 . i had my prostate removed , but it wasn’t enough . Cancer was found on the outer ring of the prostate area . I was treated back in sept of 2018 with radiation and also hormone therapy .My first blood results came back 2 months ago .And my psa level was undetected ..My doctor said that the treatments are working ..Am i eligable for a policy or do i need more time .. .. Thank you