You work, you save, you retire – it’s the American way, right?

But what happens when you have done a good job saving and get to be one of the lucky ones to retire early – are you still subject to the IRS rules of being age 59 1/2 before you can touch your money?

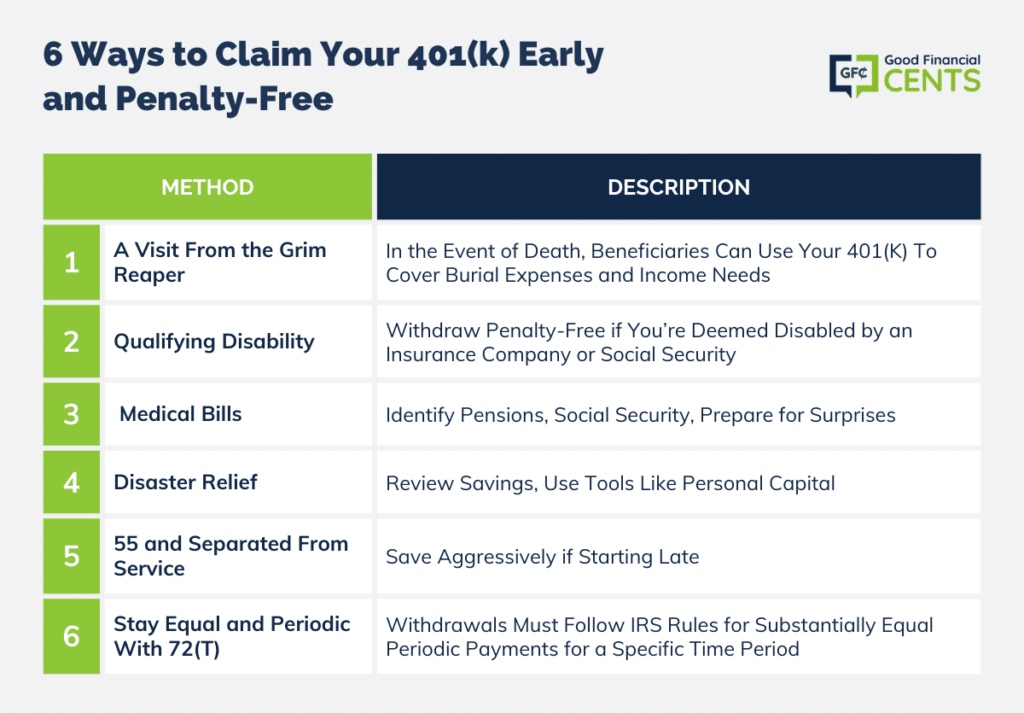

Ways to claim your 401k early and penalty-free

(Side rant: what the heck is up with the IRS and these 1/2 ages anyway? This concludes my rant.)

If you are stressed about having to pay the 10% early withdraw penalty, don’t freak out just yet. The IRS – believe it or not – does allow methods to withdraw funds from your 401k without penalty. Just make sure you follow the rules before you claim your prize.

A Few Notes Beforehand

- You always have the option to take a 401(k) loan (if your plan allows it). Does that mean you should take it? I’m hoping that you have ample emergency funds that you can tap first. Stated another way and more bluntly: You Better have enough emergency funds. Got it? If not, make sure you know the 401(k) hardship withdrawal rules.

- Before you make any withdrawals from your 401(k), do more than just read this post. Consult your financial advisor and/or tax professional to make sure you have your bases covered.

Another thing, the methods shared below allow you to avoid the 10% penalty, but they do not… I REPEAT…..do not prevent you from having to pay the tax.

Now that we have that taken care of, let’s see how you can withdraw funds from your 401(k) penalty-free.

1. A Visit From the Grim Reaper

Okay, I’m sure that death is probably not the option that you wanted to hear. I guess technically you don’t benefit. Rest assured your family will benefit in that they can use your retirement funds to cover burial expenses and supplement other income needs now that you’re not around.

Just make sure to update your beneficiaries << you have been warned.

2. Qualifying Disability

If you have been deemed to be disabled either by an insurance company or Social Security, then you are entitled to withdraw from your 401k penalty-free.

You’ll have to provide a disability letter to your 401k custodian to verify your status and avoid the penalty.

3. Medical Bills

A visit to the emergency room can add up really quickly nowadays. Our middle son banged his head on our bathroom doorway and we found that out really quick.

CHA-CHING!

If you don’t pay them, the next thing you know you have debt collectors hounding you. To avoid the penalty a few things have to occur:

- Withdraw Same Year. You have to take the money out in the same year you incurred the medical bills.

- 7.5% Rule. Take 7.5% of your AGI (Adjusted Gross Income) and that’s to the extent that the unreimbursed medical bills that you’ll be allowed to claim penalty-free from your 401(k).

On a side note, it is not required to itemize your deductions to qualify for this. If you don’t know what that means, then you better pay somebody to do your taxes for you.

And if you think that I had to tap my 401k to pay for my son’s emergency room visit, get your head out of the gutter.

4. Disaster Relief

With all the storms and flooding that have hit the U.S. recently, it’s a comfort knowing that if your area is deemed for disaster relief you can tap your 401(k) for necessary expenditures.

5. 55 and Separated From Service

According to the IRS, those who retire early or are forced out may have access to their 401(k) early. This is their wording:

“Made to a participant after separation from service if the separation occurred during or after the calendar year in which the participant reached age 55“

You can take a distribution from a qualified defined contribution plan, i.e. 401(k), and avoid the 10% penalty. A couple of key things to note in doing this is that it must be from the 401(k), 457, or 403(b), to avoid the 10% penalty.

This actually happened to my father-in-law as his company went through a buyout and he was offered an early retirement package at the age of 55. We ended up taking a distribution from his 401k to have some cash on hand and then rolled the rest into his IRA.

Don’t miss this important point: DO NOT roll over to an IRA if you think you may need some money.

If you have already done a 401(k) rollover into a traditional IRA, you have already missed this opportunity. Once you hit the IRA and you take a withdrawal, you are then assessed a 10% penalty. Rolling to an IRA might make sense later on, but until you know for sure – don’t do it.

6. Stay Equal and Periodic With 72(t)

Another more complex strategy – that I’m not very fond of – is the little-known rule of 72(t). Why am I not fond of it? Because 1. it locks you in for a long time and 2. it’s too complicated for most.

What is the rule 72(t)? The rule of 72(t) states that withdrawals from your 401k have to be “substantially equal periodic payments. You must use one of the three methods that the IRS has determined and then take your payment on a set schedule for a specific time period. It is required that you take those payments for either 5 years or when you turn 59 1/2, whichever comes later.

Example of 72(t)

Let’s say you retire at the age of 53 and you elect to do 72(t) then you must take equal payments for 7 years. If you happen to need more money during that 7-year stretch, then you’ll have to go back and pay the 10% penalty on everything taken out to that point.

Now do you see why I’m not a big fan?

If you start later on, say 56, then you’ll have to take it for 5 years till the age of 61 even though you’ve already hit 59 1/2.

401k Penalty-Free Withdrawals

As you can see, there are ways to tap your 401(k) penalty-free. Just make sure you follow the rules.

Hello,

I’m 63 years old and still employed. I’d like to take money from my 401(k) to pay off my mortgage and put a down payment on a new home. What sort of penalties or tax issues could I potentially face in doing this?

Hi Luanne – If you’re still employed by the same company where you have the 401k they may not allow you to withdraw the money until you leave the company. But on the tax side, since you’re over 59.5 there won’t be a 10% early withdrawal penalty on the amount taken. You will have to pay tax on the withdrawal however, so you may want to take the money over several years to minimize the tax liability. This is even more important since you’re still working and earning money.

Jeff,

I am 52 and working for a Utility company in Texas, with a previous employer 401K rolled into an IRA. a bit over 400k

I wanted to withdraw from my 401K to pay off my mortgage, balance 97k. I have no children or dependants. I fear that if something happens to me health wise the government will just take what I have in the 401k and I won’t be able to use it, so why not use it for me and make my life easier now

@Patrick Personally, I think you’re overreacting to the government taking away your 401k. If you pull the money out to pay off your mortgage you’ll then be giving the government a huge tax gift in the taxes you’ll paying from withdrawing your 401k. Either way, you have full control and can decide to pay it off if that’s the peace of mind you need.

We are purchasing our first home. We are trying to withdraw (hardship withdraw) from a 401k (my spouse is still employed with the company). He has elected to quit participating in the 401k. We want to withdraw monies to help with down payment. He has been trying for months! With many delays.He has provided all the documentation asked for and they have delayed saying they couldn’t open said documents etc. and never informing him they couldn’t. Which of course drug out time, and gave them time to drag out past when the payments were due, therefore not wanting to give the full amount of the hardship request. Finally after confirming they have all the documentation, they now say since the deadline for the deposits to the construction company has passed they want to confirm if we made any of the deposits and if so, we cannot receive the full amount asked for. They have asked to contact the builder personally to confirm if we had made any. It is a large well known retirement management company.

Hi Kaci – According to the IRS withdrawing money from a 401k to purchase a house isn’t a permitted hardship, at least not to get the 10% penalty waived. Are you sure that isn’t the underlying problem?

It actually is allowed for the costs related to purchasing a principle residence.

“Whether a need is immediate and heavy depends on the facts and circumstances. Certain expenses are deemed to be immediate and heavy, including: (1) certain medical expenses; (2) costs relating to the purchase of a principal residence; (3) tuition and related educational fees and expenses; (4) payments necessary to prevent eviction from, or foreclosure on, a principal residence; (5) burial or funeral expenses; and (6) certain expenses for the repair of damage to the employee’s principal residence. Expenses for the purchase of a boat or television would generally not qualify for a hardship distribution. A financial need may be immediate and heavy even if it was reasonably foreseeable or voluntarily incurred by the employee.

(Reg. §1.401(k)-1(d)(3)(iii))”

We do realize we will have to pay the 10% penalty but, shouldn’t he get the amount he requested in the first place?

Yes Kaci, as long as the employer/plan sponsor agree. The IRS has rules on hardship withdrawals, but they leave it to the employer as to whether or not they will allow them, and specifically how. You have to work with your employer on this, there’s no way around it.

I no longer work because my employer couldn’t hold my job any longer so I had got 13000 what left of my 401k so on my 1099 say I had 21000 in there but 4000 was took out for taxes and 1000 for state will I get a refund check

That sounds confusing Valerie. You won’t know about a refund until you do your taxes. The distribution will be added to your other income, and then the refund will be determined.

Hey, Jeff.

Nice to see someone who does indeed answer the questions asked…

My husband has worked for UTC for 38 years and has just retired at the tender age of 62.

We were planning on selling out home and moving South.

He inquired about closing out his 401K with the company and was told “no problem, but you must pay 20%”…

I can’t tell you what he contributed to all those years, thinking one day, we would be living a good life with the monies saved…

Now we find we are losing a great deal…

I really believe these 401K’s are a crock and would be much smarter and richer going in a different form of savings.

There were many at UTC that had no clue, what they were getting into ,,

Hi Sara – Are you just planning to take the money out to buy a house? If so, they have to withhold 20% for estimated income tax. If you plan to roll it over into an IRA, you need to share that with them and see if that will change the answer. Please discuss this in detail with the plan administrator and your CPA. The tax implications can be huge, either way. There are some quirky government plans that do have such a requirement.

Hi Jeff…

I am 55 years old and will be taking early retirement in 9 months. I have 48,300.00 in my current 401k thru my employer and plan on just leaving it alone for several years after retirement because my 2 pensions will support us until social security kicks in. Here’s my question: in 2008 I bought 750 shares of Ford stock…most of that at 2.80 per share…it’s now over 12.00 share, was as high as 14.00. With reinvestment of dividends my 750 shares is now 902 shares….the Ford stock alone makes up about 23% of my portfolio with rest being various mutual funds. I set my 401k up so I could buy stocks/mutual funds outside my company offerings. Should I sell off some of the Ford stock since it alone makes up a quarter of my balance or sit tight? If I should sell some what percentage should I keep?

Thanks for any suggestions you can make!

Hi Darren – There are no hard and fast rules here, but most financial advisors will tell you not to have any more than 5% to 10% of your portfolio in the stock of any one company. I’d lean more toward 5% since Ford is an auto stock, and the auto industry is notoriously cyclical.

Hello. I’m 37 and no longer work for the organization that gave me 401k. Since I’m going back to school, can I roll over to IRA and then withdraw tuition costs that way (so that I avoid 10% penalty).

You’ll have to put the money into a rollover IRA account, and that will incur the penalty. The IRS is aware of workarounds, and creates limits to prevent it.

I took out a loan on my 401k in the amount of 20k. It is being paid back thru deductions for the next 2 years. I was advised at the time that this will not count against me when i do my taxes. I haven’t received my 1099 yet and i want to do my taxes. Question: Will i have to pay any taxes on this since i’m already paying it back? Do i need my 1099 to file with my taxes? Please explain the process. Thank you.

Hi Joseph – The loan should not appear on the 1099. It’s a loan and therefore not a taxable event.

I’m just over 60 years old. When I eventually leave my job, is there any way to get a lump sum from my 401k without paying income tax on the total amount?

Hi Bill – Since you’re over 59.5 there won’t be a 10% early withdrawal penalty. But you still have to pay ordinary income tax on the amount of the distribution. If you made non-deductible contributions to the plan, a pro-rata part of the distribution wouldn’t be taxable, but any tax deferred contributions and all the earnings in the plan will be subject to tax.

Do you still have to pay income tax after 59 1/2 age ?

Yes Akash. As long as the contributions were tax deferred, regular income tax must be paid on distributions. However using the techniques in the article will enable you to avoid the 10% early withdrawal penalty, which won’t apply if you’re over 59.5 anyway.

I am 45 years old married with 4 children. I am looking to take some money out of my 401K. I am starting a new career and need money for education costs for my children and for living exspenses. Am I subject to the 10% fee?

Hi Michael – There’s no way to do that for education with a 401k. You might be able to set up a “series of substantially equal periodic payments” from the plan, which will allow for the distribution of funds over your life expectancy – which could be another 40 years. You’d have to pay income tax, but not the 10% early withdrawal penalty. See if you can set that up with your former employer.

Hi, I was paying 401k for 2 years and got fired after that. How can I withdrawal that money since I no longer work their?

Hi Erika – You should be able to request a withdrawal of the money. But you will probably have to pay income taxes on the amount withdrawn, as well as a 10% early withdrawal penalty if you are under age 59.5. A better option is to have it directly rolled over into either a new employer 401k plan (if they’ll allow it) or into your own IRA. No taxes or penalties with either of those moves.

Can I access my 401k to put a down payment on a home?. I am going to be a first-time home buyer will I be penalized for doing that im planning on using 4k

Hi Naomi – You can with an IRA, but not with a 401(k), at least not for the purchase of a home, first or otherwise. You can always take the money out of your 401k – if your employer will allow you but they probably won’t. You’ll have to pay a 10% penalty if they do. But if they don’t, you might try asking for a loan against the plan.

I have no job in USA now and my current location is INDIA. How can I withdraw all my funds without pay any tax / penalty ?

Hi Shashank – I think the same rules will apply as if you were a US resident. If you’d like to get more information, I’d suggest that you consult with a CPA or a tax attorney, either based in the US.

Good afternoon I work at Sikorsky aircraft and turned 55 this year. My company that owned Sikorsky ,UTC was sold to Lockheed Martin starting in 2016. Would I have to pay the 10 percent penalty with an early 401k withdrawal.And I still work there. Thanks

Hi Frank – You should be able to get your 401k distributed to you under 72t, as a series of equal payments, since you’re 55. But you can also take the 401k and roll it over into an IRA, and pay no tax at all. If you need the money to live on, see if your company will do the 72t.

Thank you for your answer. But what if I need to take a large sum of money out of my 401k in this situation that im in. Would I still have to pay a 10 percent penalty.?

Yes, Frank, as long as the amount withdrawn exceeds the amount of the scheduled distribution. Turning 55 doesn’t enable you to tap your 401k without limit and without penalty. You have to work within the established regulations.

I am 64 and a renter. Is it a mistake to withdraw enough from my 401k to avoid PMI.

Hi Debra – Your going to have to crunch the numbers. You will have to pay regular income tax on the amount of the withdrawal, so you’ll have to measure out that cost versus what you will save in PMI – which is a monthly expense. Can you take a loan on the plan instead of a withdrawal?

Hi Jeff my name is Manuel i’m 55 yrs been employed for company 15 yrs . but was bought out by another company that will be taking over in the year 2017 . Did have neck and spine surgery a year ago , that being said not knowing in the condition status of my employment of possibly forced into early retirement because of being a high risk could I be able to withdraw from my 401 K with out the penalty .

Hi Manuel – You should be able to do a distribution under 72t that allows substantially equal payments. You’ll still have to pay regular income tax on the withdrawals, but not the 10% penalty.

My husband retired at age 55 and took advantage of the IRS age 55 separation rule and is taking distributions from his 401K without a penalty. Would my husband be able to continue the distributions if he takes a temporary job or starts a business?

No Corrine, he can take earn money and still continue with the 72t.

Jeff

I am 38 and i took money out of my 401k for a hardship. Do i have to claim it on my tax return

Hi Jenn – Yes you will. Even though the penalty is waived for a hardship, the withdrawal is still subject to ordinary income tax. The general rule is that if you get a tax break going in, you’ll have a tax liability going out.

Jeff,

I am 55 years old. I am a teacher and I have a TIAA CREFT account. Also I have a couple account (Roth and IRA) with Vanguard. My Vaguard’s accounts are from a previous employer about 15 years ago. I am planning to retire in 4 or 5 years.

Can withdraw funds from your 401k with Vanguard without penalty if use the “stay Equal and Periodic With 72t”, even if I still working?

Hi JC – You can use the series of substantially equal payments under 72t, but not the separation from service provision (applies to 401k only).

I’m 56 the dr office I worked for has merged with another office and right now my 401 is frozen. They said we could withdraw money, will that qualify as a separate from service. My husband is disabled and that money can help out. Thank karen

Hi Karen – You won’t qualify for the penalty exemption for your husband’s disability (it has to be your disability as owner of the plan). But you may qualify under separation from service with substantially equal payments. I think that’s what they’re talking about. Talk with your accountant, or consult with one if you don’t use one. There’ something of a gray zone here because it seems as if you’re still employed with the original employer.

Thanks for the article. I recently separated from my employer of two years and have about 10k that I am withdrawing from a 401k. If I elect to have 100% withheld and sent to the IRS are the funds still subject to all of the taxes and the 10% penalty?

I will be doing it either way to offset the tax liability from freelance (1099) income I have been making but was curious if the fact that the funds never touch my hands matters…

Thank you for your time.

Hi Tony – You won’t know what the tax liability for the distribution will be until you file your income tax in the spring. The withholding is just an estimate to cover the expected liability. You could get a refund as a result of the withholding. After all, if you’ve been unemployed much of the year, your income and your tax bracket will be lower than usual.

Good day. So if Tony decides to withhold 100% of 401k funds and transfer to IRS, and assuming Tony is Less Than 59 1/2 years old, will those 100% funds that were sent directly to IRS still be liable for the 10% penalty?

Yes Antonio, unless you meet one of the exceptions. But if 100% of the 401k is paid as taxes, you’d probably still get a refund. But then I don’t know your complete tax situation.

I retired from the state of ga and receive a monthly retirement check. I went back to work and am in a 491k plan. I am 58 years old and planning to stop working to take care of my mother. Will I be penalized if I take my money out now?

Hi Leslie – I’m not aware of all of the many state plans that are available so I can’t advise you. Please check with your employer to see what the regulations are. There may be a hardship provision that allows you to withdraw the money penalty-free.

You say “If you have been deemed to be disabled either buy an insurance company or Social Security, then you are entitled to withdraw from your 401k penalty free. You’ll have to provide a disability letter to your 401k custodian to verify your status and avoid the penalty.” I am currently on disability approved by my disability insurance, but everywhere else, I read that must be permanently and totally disabled. Will a letter from my disability insurance company work for me?

I’m not sure the IRS specifies permanent or temporary disability. You need to contact your employer with this question, since it’s up to them whether or not they allow hardship withdrawals, under what terms and what the documentation requirements are.

I am 36 years old and i just received a letter stating i accrued a total “pension plan” balance of around $4,000 at a job i held for a little while but am no longer employed for. i would like to access that money to pay some bills and purchase a cheap car to get me back and forth from my new job. Is this possible?

Hi Chad – You should be able to, but you will have to pay regular income tax on the amount of the distribution. You will also have to pay a 10% early withdrawal penalty if you are under 59.5.

I work for a company full time right now, but am thinking about going to part time hours. Part time employees where I work do not qualify for 401k. So, my question is.. If I no longer qualify for this benefit, will I be able to withdraw the money? And, how much in medical expenses do you have to owe in that year to qualify for early withdraw without penalty?

Hi Sonja – If and how much you will be able to withdraw from the 401k while still employed will be up to your employer. What ever you do withdraw will be subject to regular income tax, as well as the 10% early withdrawal penalty if you are under age 59.5. As to the medical withdrawal, you can get a hardship exemption on the withdrawal of an amount to cover medical expenses to the degree that the expenses exceed 10% of your adjusted gross income.

My husband separated from his employment a couple of months ago. He was fully vested after 13 years of employment. He filled out paperwork to take a distribution to pay some substantial medical bills. After receiving the paperwork the company is now telling him there is a one year restriction on touching the money, whether it be for a distribution or rolling the money into a new account. Is this legal?? I always thought once you were no longer employed with a company the 401k money was yours.

Hi Ashley – Unfortunately, the IRS give a lot of latitude to employers on how the handle the specifics of 401k plans. For example, though the IRS permits 401k loans and contribution matches, the employer is not required to provide either. I don’t know for certain, but I believe that have significant flexibility in determining distributions too. You might want to consult with an attorney who specializes in pension law. That will tell you right away if you have any recourse. And sometimes just having a letter sent to the employer from an attorney magically fixes the problem. It’s worth a shot.

Jeff,

I have a traditional pension as well as a 401k. I plan to retire next year (age 55). my pension will be a lump sum amount. Can I roll that lump sum into my 401k and then withdraw without the 10% penalty? or do i have to leave them as separate accounts and withdraw from 401k first?

Thanks

Bobbie

Hi Bobbie – I believe there’s a complication in the exemption rules when you do a rollover, particularly one that close to retirement. Can your pension trustee set up a series of periodic payments? I’d lean toward keeping them separate and withdrawing from the 401k first. You can put the pension funds into an IRA. But please contact a CPA to get specific advice as to what to do. Alternatively, you might be able to get the same advice from your 401k trustee free of charge. Contact them about the pension rollover and see what they recommend. Be very specific in explaining to them that you want to withdraw the pension funds penalty free, after they are deposited into your 401k, and make sure that’s acceptable.

Be real careful on this, as penalties on pension and retirement mistakes can be steep.

Hi live in Calif my employer has a 403 b I have 2 current loans on my 403 if I want can I withdraw the remaining monies thank you

Hi Nancy – I’m not sure what your question is, but if you don’t repay the loans, your employer will declare them as early distributions. You will then have to pay tax on the amount of the loans, plus a 10% early withdrawal penalty. Was that your question???

My wife had a mastectomy in 2014. In 2015 she decided on breast reconstruction. We were under the impression from the surgeon that it was covered by our insurance. He was actually not in network, so we received a bill for 96,000.00 dollars. We need to try and lower this somehow but probably will still need a large amount to settle the debt. We have her 401k from an old employer, she is 51 and we would like to avoid the 10% penalty. we are in 15% tax bracket. She makes approx. 53,000 per year, I am retired. Any suggestions would be a great help.

Thank you

Michael F.

Hi Michael – There is an exemption to the penalty if the total cost of medical expenses for the year exceed 10% of your income, even if you don’t itemize. But I’m pretty sure the withdrawal has to occur in the year in which the liability was incurred. But check with your tax preparer!

Hello, my husband and I have had no income for the last 4 months. My husband decided to withdraw his 401k, so that we have money to live on. I can’t find anywhere that not having any income is a hardship that would be an exception to the tax penalty. Please advice. Thanks

Hi Mackenzie – The IRS does allow for exemption from the penalty under limited circumstances. There’s a list here and I’d suggest that you scan it to see if any apply. If he was separated from his job and was at least 55 years old (or 50 if he held a government job), he may qualify.

Hi Jeff I am currently 54 and would like to buy a retirement house with my 401k money how do I do this to avoid the 35% tax I have already done a homeowners loan back in 2011 thanks

Hi Sherri – You really can’t. There is no homebuyer’s exclusion on a 401k (that’s for IRAs only). So if you withdraw money for the purchase – assuming your employer allows it – you will have to pay both regular income tax and the 10% early withdrawal penalty.

Will your employer allow you to take a loan against the plan that you can use for the down payment? If you can borrow against it, that would be your workaround the taxes and penalty. However, the loan amount will be limited to $50,000, and would have to have a repayment plan.

Talk to your employer and see if this is an option, and what the limitations are.

hi, i am 53 years old and have been out of work for the last 3 1/2 years due to disability, im still disable, and no income, can i use my 401k to help me on a monthly basis and hope one day i will be able to go back and work again.please any information will be appreciated.

thanks

Hi John – You should be able to take a 72t distribution for disability purposes. But please understand that while this will exempt you from the 10% early withdrawal penalty tax, you will still have to pay ordinary income tax on the amounts distributed. Hope this helps!

what about if i start to use the 72 distribution an after , two years I don’t need anymore , can I stop or do I need to use the 72 (months?) what is the ordinary income taxes?

I took out a 401k loan recently and they mailed the check. I received the check but have not cashed it as I emailed the principal and told them it was not needed. My question is if I do not cash the check for the loan will I be charged for the loan anyway as I have not technically accepted it? My payment is scheduled to come from my paycheck, will my employer begin charging me if the loan Check is not cashed and the loan therefore not received?

Hi Jimmy – You’re going to have to discuss that with the plan administrator and see how that will be handled. My guess is that no interest or fees will ultimately be charged, but the payroll deduction may happen if a deadline has been crossed, and you’ll have to be prepared for that. It’s all going to come down to what the plan policy is in this kind of situation, and they may have to make one up if there is no policy (good possibility!). The good news is that it won’t affect your income tax liability at all, so be thankful for that. That said, please move to resolve this as soon as possible to minimize any possible cost to you.

Good morning Mr. Rose. My husband will be 55 in June this year and he has been at the same job for more than 30 years. The company was bought out and there have been many of the more seasoned employs either fired or ‘asked’ to retire. My husband could very likely be one of them. He has a 401K with his job and we want him to be able to access some of it and roll the rest into my retirement plan. Would this be a qualifier to obtain a portion without penalty?

Hi Aimee – First, you cannot roll over the distribution from your husband’s 401k plan to your retirement plan. Retirement plans are tied to the individual, so any movements must be to and from accounts owned by the same person. As to accessing some of the money, you will have to pay ordinary income tax on the amounts withdrawn (and not rolled over), but you can escape the 10% early withdrawal penalty under the “separation from service” by employees age 55 and older, as indicated on this chart. I hope this helps!

Hi my husband recently was told he could roll over his 401k or withdraw it. He wants to get it out but he wanted to do this without a lot of penalties. What can he do? The company he works for went from P&G to Duracell and its $100,000 what can he do to avoid so many penalties?

Hi Kim – There are exemptions, and you can check them out on the IRS website to see if any apply. Otherwise the best strategy is to roll the money over into another plan or an IRA to avoid both regular tax and the penalty.

Do I have to pay the 10% early withdrawal penalty on my 401K when the company I worked for shut down?

Hi Whitney – The 401k should be intact with the plan trustee, so if you take the funds directly and you don’t meet any of the exemptions then, yes the 10% penalty will apply.

If the plan was distributed because the trustee is going down with the company, then you’ll need to speak with a CPA or tax attorney as to how to proceed. It’s more complicated if that’s the case.

I quit my job with the company I was working for in July of last year. At the end of September, I terminated my 401K and took a lump sum distribution, minus 20% for federal taxes. If I add the sum to this years fillings, It puts me in a higher tax bracket and I will be required to pay in for this year. Can I wait till next year to file my 1099-R as income?

My husband was falsely accused of excessive force on an inmate and was suspended from his state corrections job and ultimately fired. He was off over a year in total. They forced him to retire (he is 44) after they fired him and we were told not to spend the money because we had to pay it back when he got his job back. We did not have enough money to pay our bills and didn’t want to lose our house so we took out his deferred comp. He got his job back after a year and we had to pay the retirement money back in. We got the 1099R’s for the retirement money and the deferred comp. I know we have to pay tax on the money, but is there a way to not pay the penalties. It was not his fault this situation happened. The prison acts like nothing happened and made him “whole”, but we are left with the fault out of the situation.

Hi Tara – This is more of a legal issue than a tax issue. I think you need to consult with an attorney, probably one who specializes in employment/wrongful discharge cases. There’s a lot going on here, as I’m sure you already realize.

My company closed down and distributed my 401k minus taxes and penalties. Who is responsible if they didn’t take enough taxes out even though it was over 30% taken out? I went to try to file and they said it wasn’t enough taken out and that I can’t file through the original state that I lived in because it’s been over 6 mons. BTW I’m 53.

Hi Jessica – Since you were the one who received the money in the distribution, you must pay the tax liability. The amount the employer withheld is just an estimate, which is more typically 10% or 20% – so they actually withheld more for you. Since the company closed down, you might be able to get an exception to the 10% early withdrawal penalty which will lower your federal tax liability. Check out the exceptions under a 72(t) distribution.

I’m not sure about the state filing requirement that you indicated. It sounds unlikely, particularly if it means you’ll owe state tax, but some of the states have some provisions that are nothing short of weird! Please consult a tax advisor in the state in question to make sure about that, it just doesn’t sound right.

I am no longer employed by the job where I accrued a large amount of money. When I checked they said I cannot take any type of loan due to the fact I no longer work there. Is that true?

Hi Terry – Your former employer is correct. 401(k) loans are for active employees only, and even at that an employer is not required to make them available. Any money you receive from the plan after separation will be considered to be a distribution.

My employers rules state an employee cannot take early withdrawals from our 401k before age 57 1/2…IRS rules say 55. Which rule takes precedents?

Hi Darren – Your question is actually floating in a gray zone! Here’s the way I understand it. The IRS issues minimum guidelines, which an employer cannot exceed. However, they also allow the employer significant latitude in making the their plans more restrictive. A good example of this is 401(k) loans. The IRS permits them (within certain limits) but the employer is not required to offer them.

There can also be an issue with contributions in your case. IRS rules on early distributions refer primarily to employee contributions. The employer may have other, more restrictive rules in regard to the employer portion of contributions, and even to earnings in the account.

401(k) Resource Guide – Plan Participants – General Distribution Rules may shed some light on this, but I think you’re going to have to get into some deep discussions with your employer on this subject. It’s not likely that you’ll see the IRS overrule your employer if their policies are more restrictive.

Sorry for the error above in my post..I need to withdraw $ 15,000.00, not $11,000.00.

Thank you.

Hi Kellie – You can take a distribution from the 401(k) for qualified higher education expenses (see https://www.irs.gov/Retirement-Plans/Plan-Participant,-Employee/Retirement-Topics—Tax-on-Early-Distributions). This will exempt you from the 10% early withdrawal penalty, but you will still have to pay regular income tax on the distribution. But since you are unemployed and a full-time student, your taxable income is probably close to zero. If you do have to pay tax, it will be minimal.

That link says that only works for IRAs, but I heard the same information about a 401k. Do you know for sure?

Good catch Michelle! I read the chart wrong. Education expenses are only exempted for higher education on IRAs, not 401k’s. In either case, you still have to pay regular income tax on the withdrawal, but not the penalty in the case of an IRA account.

Jeff,

I am 44 years of age, unemployed, and am currently a nursing student. I need to withdraw $11,000.00 to pay for my tuition and related expenses for 2016 to get me through the program. I cannot work whilst in school; the program is too intense. Withdrawing the $15,000.00 from my 401k is my only alternative. My only other debt is a car payment. I don’t want to withdraw my 401k funds in its’entirety, just enough to get me through to graduation to pay for my education, housing, etc. I have no other alternative, this will have to be done, beginning of 2016, because I am exhausting my savings. Can I partially withdraw from my 401k, what penalties will/will I not incur? I am trying to rebuild my life after going through a divorce; this 401k was a part of my divorce settlement. Thank you for any advice you can offer me.

Sincerely,

Kellie S.

I will turn 61 Aug 31 this year 2015. I have between 55 – 60,000 in a 401k.

The return on this money is not enough for a monthly income. Due to employment issues the past three years, I have not been able to add to this or any 401k. This money I feel at this time would only benefit me if I could use it to pay down on my mortgage or home improvement such as insulation. Can I do this without paying taxes or penalties.

Jeff

When you say you will not be penalized for borrowing money when your 55 on your 401k, does that mean you do not have to pay it back?

I am planning on retiring and need money for a down payment for a home I need at least 50 thousand. I am only 53 yrs old..so you are saying when I turn 55 I can borrow this money without penalty and not having to pay it back?

What if I continue to work without retiring when I borrow at 55, is that OK? Or will I be penalized for not retiring?

I have received an injury at work and will not be able to return. What are my options with my pension and my 403b. I also may receive a settlement from the company I work for. I am going to be 56 in Jan. 2015 and have 28 yrs of service

I live in Minnesota. I quit my job and left my 401k in the wells Fargo retirement plan. I have started a new job. I am currently in a payment plan with the irs. I am currently disabled for 8 weeks. I have no income. Can I withdraw from 401k to have monies to pay bills and medical expenses

I’m going to be 44 in November. I was deemed disabled in 2011. I got a letter about a Private Pension Plan Benefits from a former employer from Social Security Administration when I applied for disability. In 2011 it was valued at 14-K. Would I be penalized if I cashed out the plan, or would I be exempt from penalties because of me being disabled? I’d like to use it to get a better newer vehicle. Thank you for your time reading this.

Say by the time I am 63 I have accumalated $400K. Say, me and my wife can live on our SS and pensions. Say we are in the 15% tax bracket. Now I retire at 63 and take just enough out of my traditional 401K to hit the top of the 15% tax bracket and reinvest in a vanguard mutual fund (6-8%), I do this for 7 years and pay the smaller taxes then hit 70. This will reduce my 401K to about 1/2 that is taxable and cut in half the RMD requirement. Will it work and be a benifit to moving the cash out and away from the RMD?

My husband is 60y/o…..he has a 401k profit sharing with his company. He is fully vested. He would like to draw part of his 401 k money out but his company says, “not until he actually retires”.(and his companies retirement age is 60y/o) can he fight this since the IRS says you can draw at 59 1/2?

Hi I’m 55 yrs old and in the middle of a divorce. I will be getting half my spouse’s 401k approx $30,000. I don’t have a 401k at my current job but have one still at my pass job called the

Contractors plan. Can I roll over about $20000 to that plan and keep $10,000 out

For catching up on outstanding debt like car medical etc?

Thank you

Char

Hi Jeff. I’ received my ex 401k which I will have to roll over from his company soon. My issue is I’m 52 and need to pay off debt we incurred. I am self employed , and I was told it was better to draw off small amounts dec n jan so I will have less taxes in the calendar year. I was told that that not only am I taxed n penalized , but when I file income tax that shows income and I’m taxed Again. Is that true ?

Thanks for all the tips, very informational and helpful for any and everyone! I’m young, 30yrs, and we are trying to gather up as much cash as possible for a down payment on our next home…Unfortunately I have had a bad run of health and have caught a few different bugs from where I work (Hospital), so instead of paying these large medical bills out of pocket and having hardly any cash in hand… its nice to instead pull the 7.5% of my Adjusted Gross Income. Even though it didn’t cover all of my bills from two hospitalizations it covered most of it… I have contributed a LARGE amount of my earnings to my 403b and 401k since our employer does some good matching, but in reality I could really use some of that money now vs later.. Was a great way for us to use OUR OWN MONEY! without the penalty… Great advice here for others and lots of situations!

I owe approx 110,000 on the house that I am living in now.I have approx 250,000 in my 401k. I still work and plan on doing so for another 5 years.I will be 61 years old in approx 1 year. Can I take half of my retirement out to buy another house? I want to downsize. What would be taxes and penalties for this?

Thank you,

Kathleen

I have been laid off from my employment due to cut backs. I have a 401k and I am going to have to move in with my son out of state as I am 65 years old and not in great health. Is there anyway to go about taking

the entire amount out with out paying the taxes. as in the move out of state. Thank you

Jeff,

Plan on retiring at 62 and 4 months, will have roughly 215,000.00 in my 401K Plan and 40,000 is a pension plan. Want to take Social Security when I retire yet do not know if I take $50.000 to put in my bank account will the SSN say that I can now only collect part of the $1800.00 a month that I would normally get.

Was told that if I withdraw money from the 401K and pension that I will have to claim this as income. even after retiring

Thanks

Hi Jeff,

I worked for a company that went out of business and I cant find record of them anywhere. I had a 401K plan with approx. 4,5000 and recently got a new job that offers a 401K. How could I find out where to find that prior 401K and possibly transfer it into my new one? thanks

I am 53 Years old and plan to retire when I turn 56 yrs old =2yrs 8 months 7 days.

I work for a public utility …I currently have 626,500 in a managed 401K account (Fidelity) and 221 K in another 401K account (T Rowe Price)..I am currently putting 25K into my managed account company sponsored + 4.5% company match …I currently plan to stop working on my 56th Birthday (Feb 2018)..If I retire from my current employer will I be charged the 10% early withdrawal penalty???

Concerned John

Hey Jeff…

My question is this….I lost my job Dec 2014 and at that time I was 54 years old….I will turn 55 in Oct of 2015 and as of today I’m still unemployed. Now even though I lost that job in 2014 I have remained on payroll to receive severance for 6 months which ends in June. So can I withdraw all of my 401k this year since I turn 55 and if so do I have to wait until Oct to withdraw it?

Jeff,

I have about 80K in a 401K from a company I worked at for 8 years. I never rolled it over so it’s still with that company I guess. I was separated last year and would like to take a withdrawal as a hardship because I am a single mother. I am only 47. Does it matter that I no longer work there? Isn’t there a one time tax free hardship withdrawal? Or is that only a loan? Thanks

Jeff, Thanks for the solid advice. My husband is 58 and I will be 59 1/2 soon. He has a 401K. Since I’m 59 1/2 can we withdraw without penalty even though he is 58?

Thanks.

@Barbara All retirement accounts are tied directly to your own personal social security number and, subsequently, your own DOB. Just because you’re already 59 1/2 doesn’t mean your husband can withdraw from his 401k (unless he’s already retired).

I saw an answer above that partly answers my question, but my circumstances are just a tad bit different. I retired @ 57 years & started withdrawals from my 401K. After nine months, I was asked by my previous employer to come back to work as a temporary employee for what was supposed to be a couple of months work. A year later, I’m still working as a temporary employee. I kept my withdrawals from the 401K as I expected to be let go at anytime. So, my question is, are my withdrawals from my 401K subject to the 10% penalty, even though I separated from service, but returned to work as a temporary employee for the same employer after 9 months of retirement? Thanks

Hi, I took a loan from 401k last year to cover medical bills at age 49. After I took the loan I found out the company I was working for was being sold and changing ownership. As a result most all employees were told we would be losing our jobs by the next year. In the mean time I was offered a job with abother company that was to good to pass up. End result my loan was now considered an early distrabution because the new company did not accept loans. What can I do now that my loan is considered an early withdrawal with a penalty?

Do I need to contact the former 401k pension holder or can I go ahead and claim on my tax return a medical hardship?

Thank you,

Becca

Mr. Rose,

I am 54, and my wife passed away from cancer 9 years ago, and I raise our 12 year old son on my own. I have had some issues that have caused me to have financial hardship over the last year, and I am a Flight Attendant, so having someone watch my son while I am gone is getting harder, to the point where I am paying someone to watch him just so I can go to work.

So I am thinking about resigning my position after 22 years of employment with the same company. I see in #5 where it appears that I can take money out of my 401K without the 10% penalty. Is this really possible? So can I withdraw money and roll the rest into an IRA without taking any penalty for doing that>

Thank you,

Stacy

I am using turbo tax and they keep switching me to under 59 and a half when I took my Fidelity account money out after I have insisted I was over 59.5 . I did this during the same calendar year that I turned 59. Not sure why this is so confusing I have proof I took this money out after I turned 59.5 . What is the law I have looked on the IRS website and see no problems .

Hi Jeff,

I’m a 38 year old American accountant permanently living in New Zealand. I was injured 1.5 years ago and had serious back surgery last October. Due to complications with my surgery and further complications as a result of the subsequent onset of hip osteoarthritis I am physically unable to work (and I am on high dosages of pain killers). I am unable to return to work in the near future and it is unknown if I will ever be able to return to employment. I need to quickly access the balance of my Rollover IRA account as I am about to lose my house. In order to access those funds do I just submit a letter from my doctor indicating that I am permanently disabled for the unforeseen future along with supporting evidence? If so, how quickly can this be accessed (as I have tried my hardest to avoid doing this I am now on the back foot with the bank) without penalty? Thank you for any advice you can provide.

I am ccurrently 70 years old. What is the minimum amount that I have to withdrawal at 70 1\2 years old.

@ Sandy Your RMD will be based on the previous end of year value (on December 31st) and a percentage determined by the IRS (I think it’s currently around 3.5% and increases each year). Your 401k provider should be able to assist you with this.

I was deemed disabled at 59. I was off from work hurt for 2 years prior. I had to close out my 401K and rolled it over into a money market account so that I could use some of it to catch up on bills since being hurt. Today I received a 1099 for filing taxes on the amount rolled over. I was under the impression that you didn’t have to pay any taxes until you withdrew money out of the money market account. What is the right way to proceed?

I was laid off my job on Nov 2014. I turn 55 in Jan 2015. I had to make an early withdrawal from my 401k in Nov 2014 to make mortgage payments for Nov, Dec (and for Jan and Feb 2015). Does this scenario qualify as a hardship withdrawal for 2014 taxes so I can avoid the 10% early withdrawal penalty?

I am 55 , fully veșted in my company 401k plan . I want to quit my job and leave the country for a year . Can I avoid the 10% penalty ? How much procentage can I withdraw ? Do they automatically hold 20% tax ? Or is better to roll the whole amount into an IRA ? Thank you

These are all lame. Best: Become “self-employed”, create a solo 401k account, with yourself as the “employer” (administrator). You can do it through 401kadministers.com for example. Roll all your funds into that 401k – it can stay in the same accounts … just contact Fidelity, etc and just tell them you have a new administrator and give them the info. Then borrow against the 401k as needed, penalty free. You just make note of it through the administrator website, then call your broker (Fidelity, etc), and tell them you want to cash out X amount. Note you will have to create/modify a payment plan to pay your plan back with interest … but all that interest is back to you so all you’re really doing is paying that interest into your future. No taxes, no penalty, all legal, no worries about what happens if you lose a job. Of course you will have to pay 401k administration fees, generally it’s something like 0.25% per year of your total plan assets but that’s a lot less than taxes and tax penalties which you always risk if you have an employer who will cash you out in the event of a layoff. It’s a ton easier than it sounds … just requires a little effort upfront.

Do company rules trump government rules? Why I ask is I plan to retire at 55 and was under the assumption I could start withdrawals from my 401k penalty free at that time but my employers rules are you must be 59 1/2 to make penalty free withdrawals. I’m confused…and very disappointed if I have to spend 4 1/2 mores at a job I really can barely tolerate any more, especially considering I will be 55 in just under 2 years and my wife and I have planned very well for our early retirements at age 55.

I want to start a business and I’m thinking of withdrawing from my 401(k). Let’s say I want to cash out $40,000 that will be used solely for business startup costs, and other business expenses. So $4,000 of that will go to the IRS as penalty for early withdrawal. Can that four grand be listed an itemized expense for the business? If so, would I need to set the business up as an LLC or S-Corp?

i worked for this company for 30 years it folded got another job making above min wages my house note is 3 mo. behind can i file hardship at age 56 without penalty. i do not contribute to 401 k now please help.

Ive been out of work for 1 1/2 years due to a worker comp injury and am on Social security disability. I would like to start taking something from my 401k to help out monthly. I am 61 years old and am 100% vested in my acct. I called my employers bank where the acct is servicedand was told I cant do that until I am terminated?? Was advised I could take whatever I need however, would have to pay 20% fed. tax and no penalty?? Does this sound right???

I was terminated from my employment and had to withdraw my 401K Money. I have not found a job for over 8 months now. I paid a tax of 27% on my withdrawal and it says it went towards federal taxes. Will I get my tax money back when I file my taxes or will I have to pay more money? I was on un-employment for 24 weeks and now it finished and I have not been able to find a job yet.

I was laid off from my company in March 2014. I am now 59 1/2. I have money that I have put in to my retirement plan. I am not working now but need the money. Can I cash out some of the money on my pension now without a penalty and just retire early?

@ Virginia When you say “put in to my retirement plan” does that mean your 401k or an IRA? Either way since your 59 1/2 you can access the money without penalty.

Hi, I am a disabled registered nurse, I worked at a hospital for 11yrs, my retirement letter said I would get $ 617 a month for life but now they are offering me my entire frozen pension plan in a lump sum. Im 45y/0. Will there be a penalty and approx how much can I expect to receive, thanks for a responce

I left my employer 7 months ago. I still have not gotten another job. And I need cash. My 401k is about 2500 dollars do you think I will pay a fee ?

@ Sarah You’ll have to pay tax (ordinary income rate which should be low for you) and penalty (10%).

Sorry , but I’m very ignorant about 401k info. My husband is 42. He is separate from his old job since April of last year. He left his 401k where it was. But now he is getting transfer to a different city on his new job. He has $36, and change on his 401k and we are thinking on cash out to used it at down payment for a house in the city he is getting transfer. We contacted the institution where the plan is. And they send him the paper to do the withdrawal but they told him he will get a check for $29, and change. I’m assuming this is taking out taxes. Do we have to pay anything else after receiving this amount? Thank you

Re:: 401k Distributions–

Very Curious–

I spoke with a Company rep about making a

withdraw from my 401K.. The rules they have are I can take a “One” time withdraw at 591/2. Ok That’s October 28th.. How close to that do I need to be to avoid the penalty? Does it have to be 59 and exactly the 28th of the month.. Born April 28th 1955.. Daniel

According the IRS 590, it’s your actual age. To be safe, I would wait until November to access the funds. Also, be sure to double check with your tax advisor first.

I use to work at walmart in sams not i dont i want to know what happens to my 401k plan since i dont work there any more can i cash it out

I plan to retire at 55 (currently 52 now), my pension would be a lump sum of $350,000 plus my 401k has about $500,000…I would like to roll over my 401k, and live on my pension until i’m 60. are the taxes higher or is there a penalty for using the pension money for living expenses?

@Babs If you’re planning on retiring early (55) you may want to leave your 401k where’s it’s at. How the tax laws work, you can take a distribution at 55 and avoid the 10% penalty. If you roll it into an IRA, you’ll be subject to the 10% early withdrawal penalty unless you exercise 72t.

My company laid me off, gave me $27,235.00 my 401k money, I have 60 days to roll it over. I will have 0 income this year, I own a house and have me as a deduction and my son as a dependent, if I use this 27k my tax obligation would be 0 to minimal correct? How about 10% penalty is there a way that because my tax burden is so low that I will get that back to? I am 47 years old. Thank you

@ Jim that seems to be correct on this year’s tax obligation. The 10% penalty has to do with your age, not your income limit.

HELLO , I TURNED 55 JANUARY 6 , 2014. I STARTED A NEW JOB ON NOV1, 2013. THEY DO NOT OFFER A 401K PAN. CAN I WITHDRAWL MONEY FROM MY OLD 401K PLAN IN 2014. THANKS JIM

@Jim Since you’re 55 and it’s still in a 401k plan you should be able to take a distribution without penalty. Be sure to double check with your tax advisor first.

Jim and Jeff…may be too late now, but from my understanding you can only take the 401k withdrawals from your previous employer without 10% penalty if you retired from that company after the date you turned 55 and did not roll it over to an IRA.

It sounds like you retired from the company with the 401k before your 55th birthday to take the new job on Nov. 2013, just over two months before you turned 55. So you would not be able to take those withdrawals without 10% penalty….Unless you still work for that company as well (working both jobs) and now you are retired from the company with 401k after you turned 55 in January of 2014.

Hi Jeff, i was at a company that i never put anything toward my 401K but they put a paycheck worth for every year i was there on my 10 year anniversary with the company. I am no longer at the company, i left on my own (not laid off or fired) and i received the 401K packet in the mail. Stating i have just over $8500 in there, i want to know the worse case after penalties and taxes (im in CA) What i would end up with after cashing out?

@ Derek You’re looking at 10% early withdrawal penalty plus ordinary income tax which could be 10% to 20%.

Hi Jeff. I am a young woman in my 20’s and I use to work for this company that went out of business. I had a least 2000 thousand dollars in my 401 k. Can I withdraw the money without having to pay a penalty? Is it possible for the money to be taxed at 10% so that I want have to pay the IRS.

Thanks in advance

@ Danielle Even though they went out of business you’ll still need to roll over the 401k into an IRA to avoid the 10% penalty.

i’m a 40+ yr old second-courser who quit my job and decided to go back to college using my 401k ,without incurring taxes, to pay for my schooling. How is this possible? what are the process i need to go thru to make this happen? pls advise. thanks

@ Arnel You would need to contact your IRA custodian to explain the situation and make sure they give you the right paperwork. I would also double check with your tax professional to make sure it gets done correctly.

I separated from service and took out my 401K last year without the 10% penalty. I left money on my qualified pension. Can I cash out some of the money on my qualified pension plan this year without a penalty and roll over the difference into an IRA?

@ Mine Are you 59 1/2 or did you separate at 55? If so, that might be a possibility.

hello Jeff..i just learned of this option to withdraw money from my 401k..i havent worked at this place since 2003..how would i go about doing that..& if funds are needed for a emergency how long is the process..Thanks in advance

@ Toni You need to contact the administrator on your 401k to see what they need to make the withdrawal. The process depends on them at what paperwork is required. I’ve seen some be done in a week while other have taken over a month.

You see who handles your 401k then go on their website resister,then do a withdrawal, in two days you can get a check by UPS for a $ 25.00 charge,that’s taken from your money. I helped a friend to do this.

Jeff, I was offered early retirement in August, 2012. I turned 56 in October, 2012. Can I withdraw some of by 401K without incurring the 10% penalty? I am currently working at another place of employment.

Thanks,

@ Barb. Yes, you sure can.

Jeff,

I am 60 yrs old not working and I would like to know if I could use my 401 k to pay off my house penalty free. My husband still works part time. Or can I put it into a money market account.

@ Deborah, If you are 60 years-old, you should be able to cash in your 401k penalty free.

Hello Jeff,

I’ve been offered early payment options from a retirement fund from a company that I left 10 years ago. I’m 55 this year and currently working at another job. I don’t plan to retire until after age 65. My question: If I elect to take the lump sum will I have to pay the 10% penalty?

@ Tom As long as you are 55, you should be able to avoid the 10% penalty. If you don’t plan to retire until 65 though, it would probably make more sense to roll your 401k into an IRA.

Jeff,

I thought the penalty free withdrawals from a 401k after turning 55 were only acceptable if taken from the company 401k where you were working when you retired after turning age 55.?

Tom stated that he just turned 55 but he left his previous company 10 years ago, that he was considering taking early payment options from.

Jeff, I plan to retire and leave employment from my current employer. I plan on taking a penalty free distribution from my 401K to last me until I’m 59 1/2, and roll over the rest into an IRA. Once I reach 59 1/2, I will take distributions from my IRA. My question is, if I start working for another employer, will that affect my penalty free distribution in any way from my previous employer?

Thanks

@ Bradley

I assume you have reached age 55. You can take another job and still get penalty free distributions from the employer you separate from at 55 or later.

Therefore, you need to determine if the plan you separate from will allow flexible distributions or if they will require you to take a lump sum distribution. Distributions from the plan not directly rolled over will be subject to 20% mandatory withholding.

Jeff, Can you take out all of the money from your 401K if you are willing to pay all of the penalties?

@ Bobbie You can cash out an old 401k, but you can’t cash out an existing one unless they allow some sort of hardship withdrawal.

Hi Jeff, I like to see if you can help me.

I have been working for this US Company for the last 10 years, but my working visa will expire in a few months and I’m planning to go back to my country, and not planning to work in the US anymore.

I’m 40 and I would like to take my 401K and retirement fund without any penalty. Is this possible?

Also, what do I have to do in my next year Tax report to let the IRS that I’ll not work with my SSN anymore?

@ AR I’m not as familiar for those taking US retirement funds out of state. My hunch is that you’ll have to pay the tax and penalty because there will be no way to transfer the money to an out of country retirement plan.

Hello Mr. Rose, I´m sure you can help me up. I write from Panama City, Central America. My husband lived for about 14 years in U.S. worked for Jevic Transportation NC for about 10 years, the company went into bankruptcy and he came back to Panama desapointed because didn´t get the American dream. He throwed out all documents including driver license , etc. We just noticed that he can claim the money invested in the 401 K Plan. Can he do it from here Panama, how?

Thanks in advance for your advices,

Itzel

I would also suggest contacting the administrator of the Plan that your account is in. Each plan parameters are different and may or may not allow for the distributions listed. Steidle Pension Solutions handles my company’s plan. They took over the administration when my previous TPA could not clearly explain our plan distribution rules and parameters. I appreciate knowing that representatives who specialize in retirement plans are now available to answer our many questions. Moving to Steidle has also saved our company over a thousand dollars a year in administration costs. I could not be happier with my decision to use Steidle Pension.