Is taking money from your 401(k) plan a good idea? Generally speaking, the common advice for raiding your 401(k) is to only take this step if you absolutely have to. After all, your retirement funds are meant to grow and flourish until you reach retirement age and actually need them.

If you take money from your 401(k) and don’t replace it, you could be putting your future self at a financial disadvantage.

Still, we all know that times are hard right now and that there are situations where removing money from a 401(k) plan seems inevitable. In that case, you should know all your options when it comes to withdrawing from a 401(k) plan early or taking out a 401(k) loan.

If you take money from your 401(k) and don’t replace it, you could be putting your future self at a financial disadvantage.

Table of Contents

401(k) Withdrawal Options if You’ve Been Impacted by COVID-19

First off, you should know that you have some new options when it comes to taking money from your 401(k) if you have been negatively impacted by the coronavirus. Generally speaking, these new options that arose from the CARES Act include the chance to withdraw money from your 401(k) without the normal 10% penalty, but you also get the chance to take out a 401(k) loan in a larger amount than usual.

Here are the specifics:

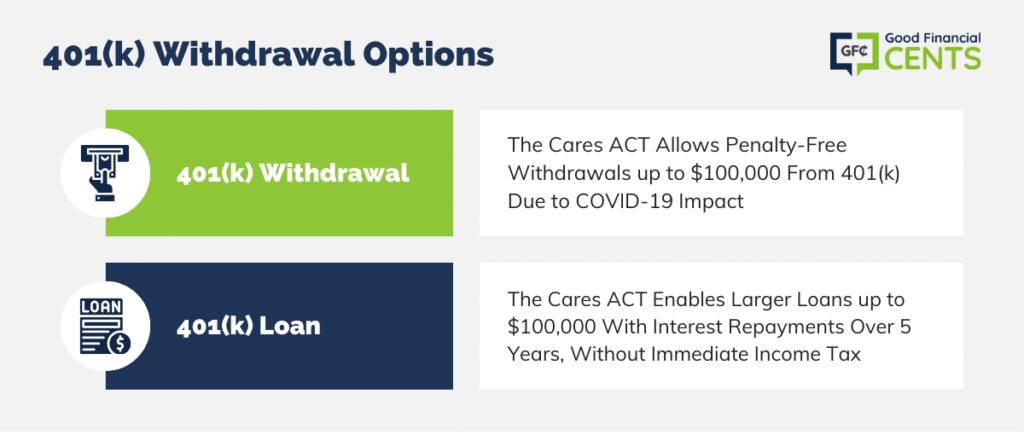

401(k) Withdrawal

The CARES Act will allow you to withdraw money from your 401(k) plan before the age of 59 ½ without the normal 10% penalty for doing so. Note that these same rules apply to other tax-deferred accounts like a traditional IRA or a 403(b).

To qualify for this early penalty-free withdrawal, you do have to meet some specific criteria. For example, you, a spouse, or a dependent must have been diagnosed with a CDC-approved COVID-19 test.

As an alternative, you can qualify if you have “experienced adverse financial consequences as a result of certain COVID-19-related conditions, such as a delayed start date for a job, rescinded job offer, quarantine, lay off, furlough, reduction in pay or hours or self-employment income, the closing or reduction of your business, an inability to work due to lack of childcare, or other factors identified by the Department of Treasury,” notes the Consumer Financial Protection Bureau (CFPB).

Due to this temporary change, you can withdraw up to $100,000 from your 401(k) plan regardless of your age and without the normal 10% penalty. Also, be aware that the CARES Act also removed the 20 percent automatic withholding that is normally set aside to pay taxes on this money. With that in mind, you should save some of your withdrawal since you will owe income taxes on the money you remove from your 401(k).

401(k) Loan

The Cares Act also made it possible for consumers to take out a 401(k) loan for twice the amount as usual, or $100,000 instead of $50,000. According to Fidelity, you may be able to take out as much as 50% of the amount you have saved for retirement.

However, not all employers offer 401(k) loan options through their plans, and they may not have adopted the new CARES Act provisions at all, so you should check with your current employer to find out.

A 401(k) loan is unique from a 401(k) withdrawal since you’ll be required to pay the money back (plus interest) over the course of 5 years in most cases. However, the interest you pay actually goes back into your retirement account. Further, you won’t owe income taxes on money you take out in the form of a 401(k) loan.

Taking Money Out of Your 401(k): What You Should Know

Only you can decide whether taking money from your 401(k) is a good idea, but you should know all the pros and cons ahead of time. You should also be aware that the advantages and disadvantages can vary based on whether you borrow from your 401(k) or take a withdrawal without the intention of paying it back.

If You Qualify Through the CARES Act

Disclaimer

With a 401(k) withdrawal of up to $100,000 and no 10% penalty thanks to the CARES Act, the major disadvantage is the fact that you’re removing money from retirement that you will most certainly need later on. Not only that, but you are stunting the growth of your retirement account and limiting the potential benefits of compound interest.

After all, the money you have in your 401(k) account is normally left to grow over the decades you have until retirement. When you remove a big chunk, your account balance will grow at a slower pace.

As an example, let’s say you have $300,000 in a 401(k) plan, and you leave it alone to grow for 20 years. If you achieved a return of 7 percent and never added another dime, you would have $1,160,905.34 after that time. If you removed $100,00 from your account and left the remaining $200,000 to grow for 20 years, on the other hand, you would only have $773,936.89.

Also, be aware that while you don’t have to pay the 10% penalty for an early 401(k) withdrawal if you qualify through the CARES Act, you do have to pay income taxes on amounts you take out.

When you borrow money with a 401(k) loan using new rules from the CARES Act, on the other hand, the pros and cons can be slightly different. One major disadvantage is the fact that you’ll need to repay the money you borrow, usually over a five-year span. You will pay interest back into your retirement account during this time, but this amount may be less than what you would have earned through compound growth if you left the money alone.

Also, be aware that if you leave your current job, you may be required to pay back your 401(k) loan in a short amount of time. If you can’t repay your loan because you are still experiencing hardship, then you could wind up owing income taxes on the amounts you borrow, as well as a 10% penalty.

Note: The same rules will generally apply if you quit your job and move out of the United States as well, so don’t think that moving away can get you off the hook from repaying your 401(k) loan. If you’re planning to leave the U.S. and you’re unsure how to handle your 401(k) or 401(k) loan, speaking with a tax expert is your best move.

Keep in mind that, with both explanations of a 401(k) loan and a 401(k) early withdrawal above, these pros and cons are predicated on the idea you can qualify for the special benefits included in the CARES Act. While the IRS rules for qualifying for a coronavirus withdrawal are fairly broad, you do have to be facing financial hardship or lack of childcare due to coronavirus. You can read all the potential qualification categories on this PDF from the Internal Revenue Service (IRS).

If You Don’t Qualify Through the CARES Act

If you don’t qualify for special accommodation through the CARES Act, then you will have to pay a 10% penalty on withdrawals from your 401(k) as well as income taxes on amounts you take out. With a traditional 401(k) loan, on the other hand, you may be limited to borrowing just 50% of your vested funds or $50,000, whichever is less.

However, you should note that the IRS extends other hardship distribution categories you may qualify for if you’re struggling financially. You can read about all applicable hardship distribution requirements on the IRS website.

Taking Money Out of Your 401(k): Main Pros and Cons

The situations where you might take money out of your 401(k) can be complicated, but there are some general advantages and disadvantages to be aware of. Before you take money from your 401(k), consider the following:

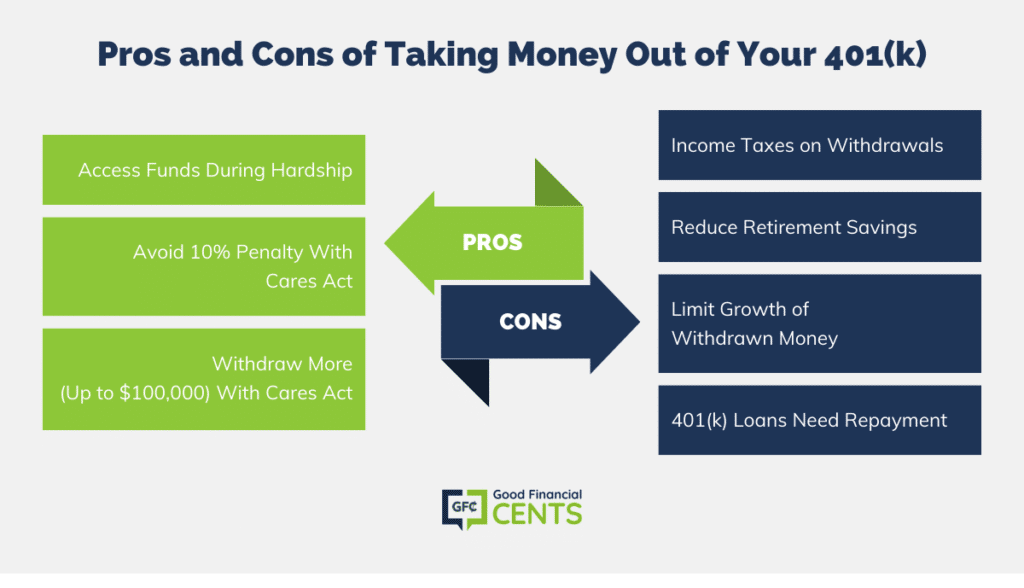

Pros of Taking Money Out of Your 401(k):

- You are able to access your money, which could be important if you’re suffering from financial hardship.

- If you qualify for special accommodations through the CARES Act, you can avoid the 10% penalty for taking money from your 401(k) before retirement age.

- You can take out more money (up to $100,000) than usual from your 401(k) with a 401(k) withdrawal or a 401(k) loan thanks to CARES Act rules.

Cons of Taking Money Out of Your 401(k):

- If you take money out of your 401(k), you’ll have to pay income taxes on those funds.

- Removing money from your 401(k) means you are reducing your current retirement savings.

- Not only are you removing retirement savings from your account, but you’re limiting the growth of the money you take out.

- If you take out a 401(k) loan, you’ll have to pay the money back.

Alternatives to Taking Money From Your 401(k)

There may be some situations where taking money out of your 401(k) makes sense, including instances where you have no other option but to access this money to keep the lights on and food on the table. If you cash out your 401(k) and the market tanks afterward, you could even wind up feeling like a genius. Then again, the chances of optimally timing your 401(k) withdrawal are extremely slim.

With that being said, if you don’t have to take money out of your 401(k) plan or a similar retirement plan, you shouldn’t do it. You will absolutely want to retire one day, so leaving the money you’ve already saved to grow and compound is always going to leave you ahead in the long run.

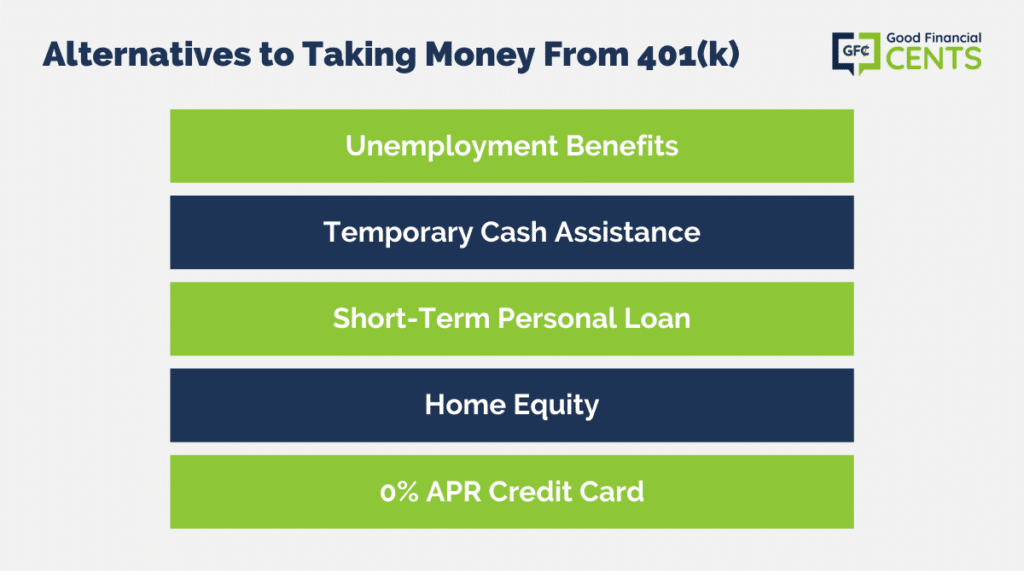

With that in mind, you should consider some of the alternatives for taking money from a 401(k) plan:

- See if you qualify for unemployment benefits. If you were laid off or furloughed from your job, you may qualify for unemployment benefits you don’t even know about. To find out, you should contact your state’s unemployment insurance program.

- Apply for temporary cash assistance. If you are facing a complete loss in income, consider applying for Temporary Assistance for Needy Families (TANF), which lets you receive cash payments. To see if you qualify, call your state TANF office.

- Take out a short-term personal loan. You can also consider a personal loan that does not use funding from your 401(k). Personal loans tend to come with competitive interest rates for consumers with good or excellent credit, and you can typically choose your repayment term.

- Tap into your home equity. If you have more than 20% equity in your home, consider borrowing against that equity with a home equity loan or home equity line of credit (HELOC). Both options let you use the value of your home as collateral, and they tend to offer low-interest rates as a result.

- Consider a 0% APR credit card. Also, look into 0% APR credit cards that allow you to make purchases without any interest charged for up to 15 months or potentially longer. Just remember that you’ll have to repay all the purchases you charge to your card and that your interest rate will reset to a much higher variable rate after the introductory offer ends.

The Bottom Line: Should I Take Money Out of My 401(k) Now?

In times of financial turmoil, it may be tempting to pull money out of your 401(k). After all, it is your money. But the ramifications to your future financial well-being may be substantial. The CARES Act has introduced new options to leverage your 401(k) without the normal penalties.

Find out if you qualify and take time to understand the details behind the options. We recommend speaking to a tax expert if you have any questions or concerns regarding possible tax penalties.

The traditional wisdom is to leave your retirement untouched, and we agree with that. If you’re in a financial bind, consider other options to get you through the rough patch. Tapping into your 401(k) should really be your last resort.