The insurance market today has many options that are geared towards addressing numerous needs for individuals and families considering life insurance.

Whole life and universal life are two popular permanent life insurance products to choose from and it’s important that you understand the advantages and disadvantages of both types.

The products under these two umbrellas address a need for lifelong coverage as opposed to the temporary “term” coverage, which protects a policyholder for a certain number of years (typically between 10-30), upon which time it may continue as a very expensive annual renewable term policy.

Rather than face the high costs of annual renewable term, forgetting to move to a permanent policy during a term’s conversion period, or face much higher premiums at the expiration of a term policy, whole life and universal life allow clients to receive a policy with premiums based on their current age and health factors, such as if you suffer from diabetes, or being heavily overweight.

Table of Contents

Whole Life

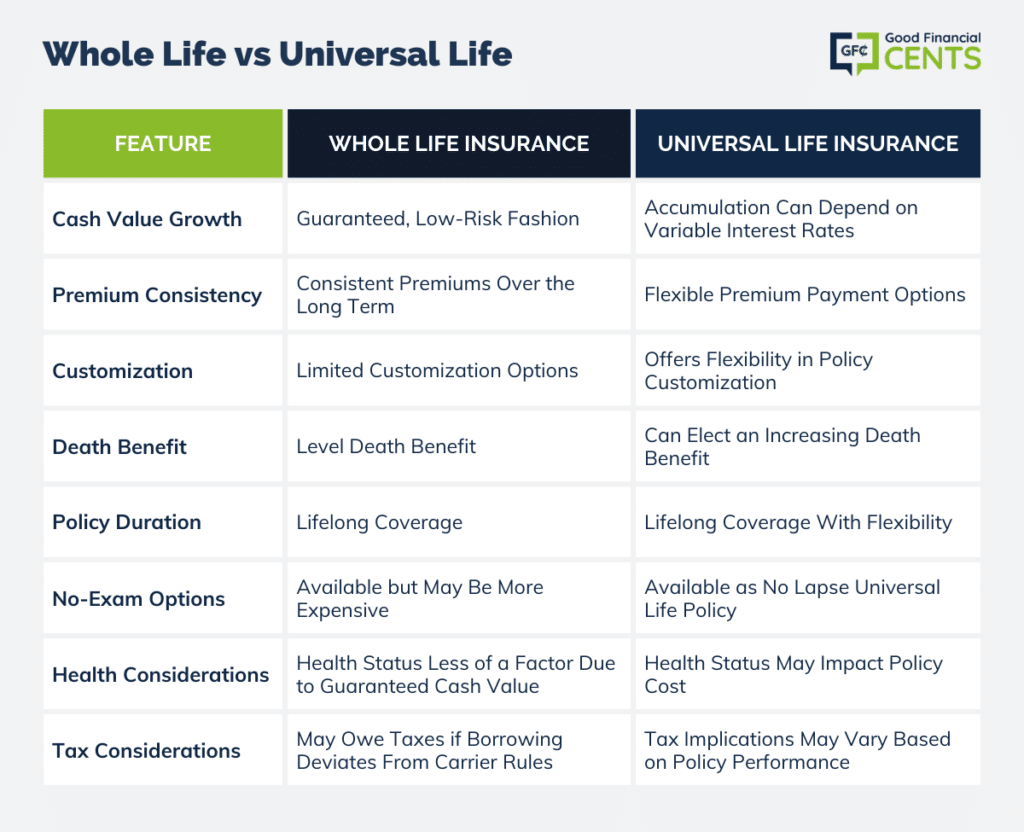

Whole life insurance policies have a good reputation because of their connection with dividend-paying insurance carriers, so the cash value within the policy builds in a relatively low-risk fashion. These funds are then available for the policyholder to borrow against, but one of the downsides is the importance of following strict carrier rules about when and how much money can be borrowed- those who deviate may wind up owing taxes.

One of the biggest appeals of whole life insurance is a consistent premium. Since whole life insurance is structured in this “lifelong” manner, clients who maintain their policies for longer than 20 years will reap the most benefits in cash value.

Universal Life

Universal life offers the same “lifelong” protection as whole life, but policies come with flexible features that interest clients who want some customization. For example, the face amount of the policy can typically be increased or decreased over the life of the policy. Rather than just the traditional level death benefit offered by whole life, policyholders can also elect an increasing death benefit, which factors in the face value of the policy as well as the accumulated cash value.

Premium payment options for amount and frequency allow for further flexibility. If the policyholder becomes unable to pay the premium for a short period of time, the accumulated cash value can cover that premium amount. If that cash value becomes depleted, however, the policy may be in danger of lapsing.

The main difference between the two types of policies is that accumulation in a whole life policy is guaranteed, whereas the performance of a universal life policy can depend. Interest rates for a universal life policy are usually adjusted on a monthly basis as opposed to the annual readjustment of whole life. For those who prefer a little bit more involvement in their policy, universal life offers flexibility as well as cash value accumulation. The protection offered by these policies can interest a broad range of potential policyholders.

The No Exam Route: Whole or Universal

There are a lot of applicants who don’t want to take the medical exam. They don’t want to go through all of the hassles or take the blood tests. Regardless of why they don’t want to take the physical, there are ways around it. A little-known fact is you can get BOTH whole and universal life as a no exam option, but you still have to determine if it’s the best choice.

Life insurance without the health and medical hoops to jump through might sound like the best of both worlds, but there are some hang-ups. Let’s start with a standard whole life insurance policy. There are PLENTY of no exam whole life options, but they aren’t created equally. With a no exam policy, you get quicker coverage, but you also get more expensive protection. Do you value speed or affordability?

It’s a fact of life insurance, if you don’t give all the information they want, you’re going to pay more. No health exam life insurance is going to cost you two or three times more. Now let’s look at no exam universal life insurance. They are much less common and typically call No Lapse Universal Life. The most common no exam universal policy is sold by Sagicor. These policies will allow you to get all the other benefits of a universal policy, but without having to take the exam.

The Sagicor NLUL policy will allow anyone between the ages of 18 – 85 get universal life insurance very quickly and very easily. The underwriting process is different depending on your age. Sagicor has an accelerated underwriting process, most of which is automated. No more waiting for an agent to review all the information or send you papers. You won’t have to do a phone interview or take an exam. It’s as simple as filling out a couple of forms.

The Importance Of Life Insurance And How Much You Need

Finding the perfect life insurance plan is vital for you and your family. Choosing between whole life vs term life, or universal, it’s important that you have adequate coverage from a reputable life insurance company.

Making important decisions is tough, and purchasing life insurance is definitely one of them. What would happen today if you passed away, you would probably leave your family with some serious debt.

Mortgage payments, funeral expenses, car payments, and so much more. All of these expenses can leave your family with a mountain of bills that they can’t pay for. Having a life insurance policy can give your family the resources they need to get through this difficult time without having any added financial strain. Don’t let your grieving family have to worry about how they will cover the mortgage or a funeral.

After you decide which type of insurance policy you’re going to buy, you have to decide how large of a policy you’re going to need, and look at your financial situation to determine that. The first thing, as we mentioned early, is how much debt would you leave for your family?

Make sure that your policy is at least big enough that your family would be able to pay off any final expenses. Sit down and calculate all of your debt and debt that you may have in the future, this number is a great starting point for your policy.

Wouldn’t you want your face value to reflect a few years of what your salary would have been? We think its valuable to use your current income and multiply it by a few years, 3, 5 or 7. While the perfect number hasn’t been found yet, it’s always a good idea to keep this in the back of your mind as you shop for policies.

Getting Lower Insurance Rates

Most people are surprised to see how inexpensive their monthly premiums are. We love letting people know the ways to save money on your life insurance rates. Always compare quotes from multiple companies before you pick one. Each company has a different rating system, which means that each applicant will be looked at differently.

We work hard to save you time and frustration so that your day isn’t filled with speaking to numerous companies and brokers. Fill out the quote form on the side and the best life insurance rates will come to you. You won’t have to keep answering the same questions to a dozen different agents.

Aside from getting quotes from different companies, improving your health can drastically lower your rates. How healthy you are is usually number one in causes of concern from the carriers. After the application, the company will send out a paramedic or nurse to complete a health exam. The results of the health exam could either save you money or cause your fees to go through the roof.

Two of the best things you can do with your health and your life insurance policy is to quit smoking and lose weight. Smoking cigarettes will cause your life insurance premiums to double or triple automatically. Even if you’re in perfect health, using tobacco will break your bank.

Additionally, being overweight isn’t only bad for your health but also bad for your bank account. The more excess weight that you carry, the higher your risk of having health complications, which will translate into more risk and higher premiums.

There are a lot of changes you can potentially make which will save you most, like losing weight or quitting smoking, but you can’t make those changes and then immediately apply for a plan. When you’ve improved your health, regardless of how you’ve done it, you need to wait to apply.

Whole Life vs Universal Life

As you can see, both types of policies have pros and cons. There is no life insurance policy that works perfectly for everyone. Take a look at your specific situation and decide which type will fit your needs best. The most important part is that you have life insurance, regardless of which type it is.

The Bottom Line – Whole Life Versus Universal Life: Which One Is For You

When considering life insurance options, the choice between whole life and universal life insurance depends on individual needs and preferences. Whole life policies are known for their cash value growth and consistent premiums over time, making them suitable for those looking for a long-term investment. On the other hand, universal life policies offer flexibility in adjusting coverage and premium payments but come with variable interest rates. No-exam options are available for both types, providing quicker coverage but at a higher cost.

When selecting a policy, it’s crucial to assess financial needs, including debt coverage and income protection, while striving for a healthy lifestyle to secure lower insurance rates. Ultimately, having any life insurance policy is essential for protecting loved ones in case of unforeseen events.

I am interested in knowing the rate of whole life insurance and the benefits. I am in excellent health…but one never knows…thank you for your guidance.

@Kathleen Please call our toll-free # and we’ll be happy to review your options.