There are a lot of ways to retire wealthy.

Stocks, mutual funds, building businesses, and numerous other “investment vehicles” that you can take to get you to a relaxing and wealthy retirement.

However, while most professionals understand that saving a good portion of your paycheck and investing it in the stock market can help you get there, many do not understand how to add real estate into that portfolio without ending up a tired, busy landlord with more problems than time.

It’s for this reason I want to share my thoughts with you today on how you can add real estate investing into your portfolio to accelerate your savings, add to your net worth, and retire with a larger investment portfolio.

Table of Contents

Real Estate Investing Basics

Before diving too deeply into the “specifics” of real estate investing, allow me to quickly give you a brief overview of just how people make money in real estate.

In the most basic sense, most investors buy property looking for two things:

- Cash Flow – the extra income that is left over after all the expenses have been paid;

- Appreciation – the equity built as property values rise and/or the loan is paid down.

There are obviously other interests, such as tax benefits, seeking alternatives to investing in the stock market, or personal needs (such as caring for an elderly parent) but primary, cash flow and appreciation are the two drivers behind a good real estate investment.

Some investors focus more heavily on achieving maximum cash flow, while others aim primarily for appreciation.

While the two terms are not always at odds with each other, you will generally find that properties with more cash flow have a lower chance for appreciation as they are located in more “management-intensive” locations that do not increase in value as quickly.

Thus, as a potential investor, the kind of real estate investment you seek to get into will largely depend on your strategy, personality, and timeline.

Personally, I believe in buying based solely on the cash flow BUT buying in areas where appreciation is possible.

I don’t want a property where I am worried about getting shot just for driving by – but making a stable return on investment each month is also important to me.

Ultimately, the kind of investment you get into is up to you – but I strongly recommend (at least at the beginning) that you plan for cash flow and make appreciation the “icing on the cake.” This way, you are ensuring a profitable investment with minimal risk.

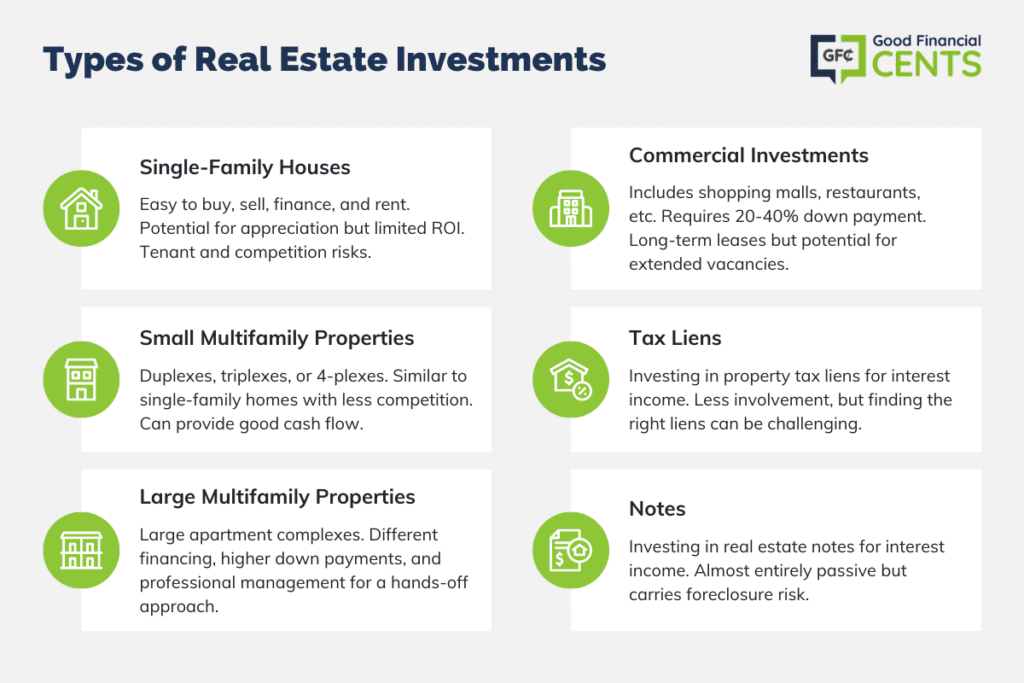

Types of Real Estate Investments

I’m sure you know someone who owns, or maybe you already own a single-family rental.

Great! However, don’t confuse the idea of owning a single-family house as the only player in the real estate investing space.

There are actually many different avenues that you can use to invest in real estate, with varying degrees of difficulty, risk, reward, and time requirements.

And remember, just about every option here can be bought as a normal listing, a short sale, or a foreclosure.

Let’s look at a few of those now:

Single-Family Houses

As mentioned above, this is the most common type of real estate that most individuals are familiar with. Single-family homes are nice because they are easy(ish) to purchase, easy to sell, easy to finance, and easy to rent.

There is always a need for people to live somewhere, so single-family homes can provide security and decent opportunities for appreciation.

However, single-family homes also do not always provide the greatest return on investment (appreciation vs. cash flow), can be easily destroyed by bad tenants, and with the rising competition in the real estate marketplace, it can be difficult to find properties that fit your criteria.

Small Multifamily Properties

These properties would include duplexes, triplexes, or 4-plexes and are found in nearly every community in America – although much more heavily in some neighborhoods versus others.

These properties have the benefit of being easy to buy, finance, and sell like single-family properties but with less competition (most home buyers aren’t looking for this type) and the “economy of scale” that comes with having more than one unit.

These properties can be more “management intense” than single-family homes, but if bought correctly, can provide good cash flow and a stable return on investment.

Large Multifamily Properties

These are the large apartment complexes you see, ranging from 5 units up to hundreds. These properties are financed using an entirely different bank division (commercial rather than residential lending) and can require high down payments, shorter-term lengths, and higher interest rates.

These properties are generally managed by a professional property manager (or a live-in manager, as is the case with my own 24-unit apartment complex), thus providing a more “hands-off” investment.

Commercial Investments

Commercial properties range from shopping malls, convenience stores, restaurants, and more. With similar financing to large multifamily properties, 20-40% is the typical down payment requirement, and again, the commercial department is who you’ll want to talk with at the bank.

Commercial property has the benefit of longer-term leases, but vacancies can often range from months to years in length.

Tax Liens

When an owner of real estate refuses to pay their taxes, the local government municipality can place a lien on the property, sell that lien to an investor, and then the investor can receive interest on the money owed.

This system can truly be a “no toilet” method to real estate investing, but learning how to find the right kind of tax liens can be an art in itself.

Notes

Another method of investing without being an “owner” – a real estate note is created when a lender funds a real estate deal and receives interest from that loan. These notes can be made, bought, or sold just like a real property.

This kind of investing can be almost entirely “passive” but can run the risk of a borrower defaulting on the loan, requiring a costly foreclosure.

Buying and selling mortgage notes is very similar to investing in peer-to-peer lending with companies like Lending Club and Prosper.

Leverage in Real Estate Investing

To leverage or not to leverage, that is the question.

Real estate investing offers a unique advantage over most other investment types – and that is the power of leverage.

Sure, with stocks, you can buy on margin and add some leverage there, but only real estate allows you to buy with as little as 20% down (10% with some programs and 3.5% if you plan on living in the property.)

This means you have the ability to receive 100% of the appreciation but only have to pay for 20% of the property. However, it also means you have the ability to lose 100% of the decline in value if prices fall, wiping out your down payment entirely.

There remains a large debate in the personal finance community as to whether using debt as leverage, such as putting 20% down and financing the remainder of an investment property, is a good idea or not.

Proponents of using “smart debt” look at the math and point out that if you can borrow at, let’s say, 5% and make 15% – you come out ahead.

Additionally, by leveraging your money and finding an incredible deal that provides good cash flow – your return on investment can be huge.

However, opponents to debt and leverage look at the problem debt has on most consumers and point out that, as Dave Ramsey is fond of saying, “100% of foreclosures last year happened to people with a mortgage.”

The choice to use or not use leverage is strictly personal and something to decide between you, your family, and your personal finance position.

Whether you choose to use debt or not, I highly recommend you learn all you can about your intended investment avenue before sinking any cash in – so you maximize your chance for success and profit.

Making Your Plan

Once you have discovered your specific real estate investing niche and decided on how you plan on funding your deal, your next step is to make a plan. As I commonly say, you don’t drive from Canada to Peru knowing only that it’s South – you need a road map, a plan.

A map keeps you on the right path, away from dead ends, and helps you to easily see where the next stop is.

When choosing to invest in real estate, having a plan is just as important. You need to decide the specific kind of real estate investment you want to pursue (as we discussed above) and how you plan on financing that investment (also mentioned above).

A calculation I like to use when investigating a potential real estate investment is known as the “50% Rule.” This rule-of-thumb states that for any real estate investment, the expenses will generally be about 50% of the total income, not including the debt payment.

This means if a 4-plex brings in $2,000 per month in income, you can assume $1,000 per month will go out in expenses, leaving you with $1,000 as either cash flow (if no mortgage was taken) or to pay the mortgage.

If your debt payment was $600 per month, you can reasonably expect $400 per month in cash flow at that point.

Using this rule of thumb (and remember, it’s just a rule-of-thumb, not gospel truth, so be sure to always run the exact numbers on any specific property you are analyzing) you can figure out your return on investment and decide if a property is worth pursuing.

In the example above, if I had paid $20,000 for a down payment on that property, which was supplying $400 per month in cash flow ($4800 per year), I would be looking at a 24% cash-on-cash return on investment from that property, not including any future gain from appreciation.

By defining your financial criteria, you are able to quickly sift through the 90% of real estate offerings that are not good deals and focus only on the ones that will provide you with the kind of investment returns you are looking for.

Self Managing vs Property Management

Finally, you’ll need to decide if you want to manage your property yourself.

If you are looking to buy one single-family home at a time and have a good deal of free time, it’s not too difficult to do.

However, if you plan on buying multiple properties and growing your investment portfolio – or you simply don’t have a lot of time, be sure to plan on having good property management in place and budget accordingly.

Keep in mind that most properties I have purchased have been bank repos, that I bought after a landlord lost his property to the bank. This proves that it’s not always easy being a landlord, and it’s easy to get in over your head.

Unless you have the patience to handle difficult tenant situations and the knowledge to handle those situations correctly – I’d highly recommend getting a qualified property manager.

If you do plan to manage yourself, be sure to properly screen your tenants, recognizing that it is better to wait for the right tenant than to place a bad tenant that will later cause huge financial problems.

For more information on tenant screening, be sure to check out the second-longest post I’ve ever written, “Tenant Screening: The Ultimate Guide.”

Where to Go From Here

No matter what kind of real estate investing you plan to get into, I highly recommend you study all you can to be a good investor before dropping any money into it.

Real estate investing is not as passive as other investment vehicles, but the returns can blow most other investments out of the water when done correctly and when you have a solid plan in place and are investing with intelligence.

The cash flow you receive from your properties can quickly add thousands to your savings account without having to work a day job for it. This can help you retire faster or at least retire with more income, more assets, and more experience.

There are many books, podcasts, forums, blogs, real estate clubs, and other sources of great education out there, and most of it is free. Information has been democratized, so take advantage of the great resources online.

You don’t need to become an expert, but once you choose your specific real estate investment path – at least become familiar with that specific niche.

Dig in, ask questions (such as in comment sections below epic posts like this one… hint hint…), and get to know some local investors who can help you get from where you are now to where you want to be.

Your retirement is yours to make of it what you will. Don’t be afraid to add a new vehicle to your portfolio, and hopefully, I’ve made the case that real estate should be that vehicle.

Let me know in the comments below if you invest in any real estate – why or why not – and any other questions or comments you may have.

Thanks, for sharing this valuable information with us. I share this post with my friends, who works in the real estate industry. They appreciate you. Again thanks for this post.

Wow, this is a very detailed and great starter post for how to get into real estate. I learned quite a bit from it, thanks!

Hi Brandon,

Great article – very informative and relevant. I also would like to add that the costs to transact real estate (commissions) can make or break an investment.

Out here in California the typical commission of 5.4% on the average California single-family detached home ($417k) will cost you over $22,500. That cost is shared by the buyer and seller. We recently did a blog post on the long term impact of this and how it can be avoided: http://www.homecoin.com/blog/?p=420

Again, great article – keep up the solid work!

Full disclosure: I operate the referenced website.

I’ve heard a lot of back and forth as to whether Real Estate is a better alternative than fully funding tax advantaged accounts. I’ve kind of come to the conclusion that if you are not fully funding IRAs/401ks, this should be done before getting a rental property.

Just my 2 cents

Hey Thomas, thanks for the comment!

The MLS use to be sufficient for finding properties, but with the increase in the market it is getting more and more difficult. I think the best way, today, to do it is:

1.) Direct Mail – sending out thousands of targeted letters to potentially motivated sellers and helping those who need help.

2.) Driving for Dollars – driving around and looking for properties that are ugly, have long grass, broken windows, terrible roofs, etc. Often – the owner is desperate to sell but knows that they can’t in the current situation. Sometimes it will be out-of-area landlords who have given up. Write down their addresses, find the owner via public record, and either call or send letters.

As for real estate clubs – I think there are good and bad ones. Some are just about the pitch, some are about information. Try to find the good ones (ask experienced investors for recommendations) and become a friendly face at them. Older, experienced investors LOVE to offer advice and help new investors out – as long as they don’t feel they are wasting their time. Appeal to their ego, let them help you out. Most will do it for an occasional cup of coffee!

Hope that helps! Great seeing you again (in a virtual way, anyways) Thomas!

Thanks for the information and the help as usual Brandon! I need to find some older experienced investors ASAP. Some of the Real Estate Clubs I have found seem to just be looking to sell the dream. Not really good on the help and advice. Thanks again!

Another great post Brandon! I am working on adding real estate to my portfolio as we speak. The biggest thing is just doing it. I have read and asked so many questions but there is nothing like & no experience let getting into. My question if finding those properties. Here in Florida it seems like everything is under contract. What is the best way to find properties?

I want to invest but right now putting all the pieces together has taken longer than expected. I wanted to find a mentor or someone I could to all the leg work for until I can experience to do it on my own but I haven’t had any luck. What do you think about Real Estate Investment Clubs?

Oops! Meant to reply but just wrote the comment below 🙂 See below:

If you do not have the down payment, you can also invest in REITS. Similar stocks and a much lower investment, but still add real estate to your portfolio.

Definitely. I’ve not personally invested in a REIT but I hear good things. Thanks for reading and commenting!