In a recession it’s common for many people to rely on credit cards and loans to balance their finances. It’s the ultimate catch-22 since, during a recession, these financial products can be even harder to qualify for.

This holds true, according to historical data from the Federal Reserve Bank of St. Louis. It found that during the 2007 recession, loan growth at traditional banks decreased and remained deflated over the next four years.

Credit can be a powerful tool to help you make ends meet and keep moving forward financially. Here’s what you can do if you’re struggling to access credit during a weak economy.

Table of Contents

How Does a Financial Downturn Affect Lending?

Giving someone a loan or approving them for a credit card carries a certain amount of risk for a lender. After all, there’s a chance you could stop making payments and the lender could lose all the funds you borrowed, especially with unsecured loans.

For lenders, this concept is called, “delinquency”. They’re constantly trying to get their delinquency rate lower; in a booming economy, the delinquency rate at commercial banks is usually under 2%.

Lending becomes riskier in a weak economy. There are all sorts of reasons a person might stop paying their loan or credit card bills. You might lose your job, or unexpected medical bills might demand more of your budget.

Because lenders know the chances of anyone becoming delinquent are much higher in a weak economy, they tend to restrict their lending criteria so they’re only serving the lowest-risk borrowers. That can leave people with poor credit in a tough financial position.

Before approving you for a loan, lenders typically look at criteria such as:

- Income Stability

- Debt-To-Income Ratio

- Credit Score

- Co-signers, if Applicable

- Down Payment Size (For Loans, Like a Mortgage)

Does this mean you’re completely out of luck if you have bad credit? Not necessarily, but you might need to take the time to understand all of your alternatives.

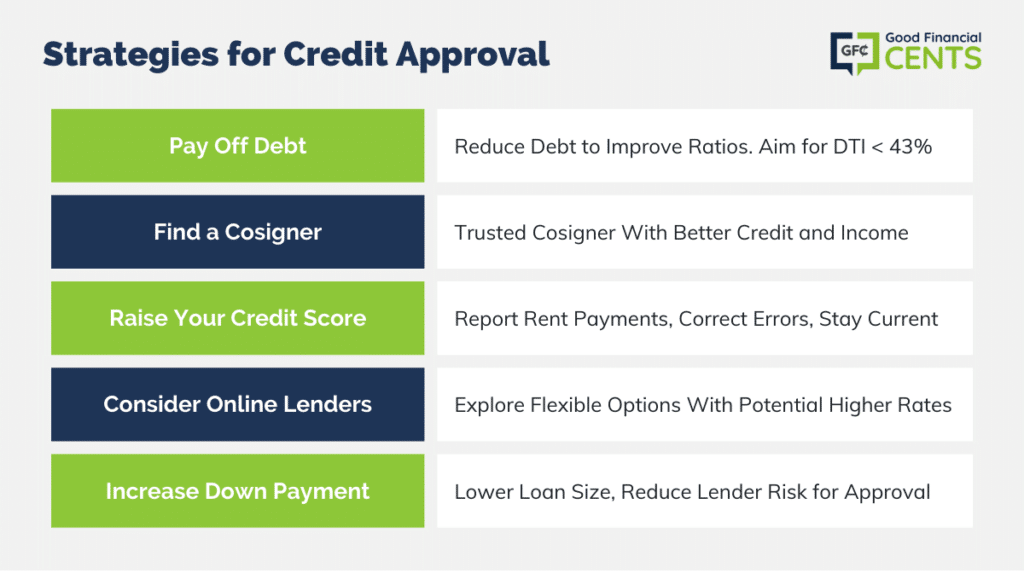

5 Ways to Help Get Your Credit Application Approved

Although every lender has different approval criteria, these strategies speak to typical commonalities across most lenders.

1. Pay Off Debt

Paying off some of your debt might feel bold, but it can be helpful when it comes to an application for credit. Repaying your debt reduces your debt-to-income ratio, typically an important metric lenders look at for loans such as a mortgage.

Also, paying off debt could help improve your credit utilization ratio, which is a measure of how much available credit you’re currently using right now. If you’re using most of the credit that’s available to you, that could indicate you don’t have enough cash on hand.

Not sure what debt-to-income ratio to aim for? The Consumer Financial Protection Bureau suggests keeping yours no higher than 43%.

2. Find a Cosigner

For those with poor credit, a trusted cosigner can make the difference between getting approved for credit or starting back at square one.

When someone cosigns for your loan they’ll need to provide information on their income, employment and credit score — as if they were applying for the loan on their own. Ideally, their credit score and income should be higher than yours.

This gives your lender enough confidence to write the loan knowing that, if you can’t make your payments, your cosigner is liable for the bill.

Since your cosigner is legally responsible for your debt, their credit is negatively impacted if you stop making payments. For this reason, many people are wary of cosigning.

In a recession, it might be difficult to find someone with enough financial stability to cosign for you. If you go this route, have a candid conversation with your prospective cosigner in advance about expectations in the worst-case scenario.

3. Raise Your Credit Score

If your credit score just isn’t high enough to qualify for conventional credit you could take some time to focus on improving it. Raising your credit score might sound daunting, but it’s definitely possible.

Here are some strategies you can pursue:

- Report Your Rent Payments: Rent payments aren’t typically included as part of the equation when calculating your credit score, but they can be.

Some companies, like Rental Kharma, will report your timely rent payments to credit reporting agencies. Showing a history of positive payments can help improve your credit score.

- Make Sure Your Credit Report Is Updated: It’s not uncommon for your credit report to have mistakes in it that can artificially deflate your credit score.

Request a free copy of your credit report every year, which you can do online through Experian Free Credit Report. If you find inaccuracies, disputing them could help improve your credit score.

- Bring All of Your Payments Current: If you’ve fallen behind on any payments, bringing everything current is an important part of improving your credit score. If your lender or credit card company is reporting late payments a long history of this can damage your credit score.

When possible speak to your creditor to work out a solution, before you anticipate being late on a payment.

- Use a Credit Repair Agency: If tackling your credit score is overwhelming you could opt to work with a reputable credit repair agency to help you get back on track.

Be sure to compare credit repair agencies before moving forward with one. Companies that offer a free consultation and have a strong track record are ideal to work with.

4. Find an Online Lender or Credit Union

Although traditional banks can be strict with their lending policies, some smaller lenders or credit unions offer some flexibility. For example, credit unions are authorized to provide Payday Loan Alternatives (PALs).

These are small-dollar, short-term loans available to borrowers who’ve been a member of qualifying credit unions for at least a month.

Some online lenders might also have more relaxed criteria for writing loans in a weak economy. However, you should remember that if you have bad credit you’re likely considered a riskier applicant, which means a higher interest rate.

Before signing for a line of credit, compare several lenders on the basis of your quoted APR — which includes any fees like an origination fee, your loan’s term, and any additional fees, such as late fees.

5. Increase Your Down Payment

If you’re trying to apply for a mortgage or auto loan, increasing your down payment could help if you’re having a tough time getting approved.

When you increase your down payment, you essentially decrease the size of your loan, and lower the lender’s risk.

If you don’t have enough cash on hand to increase your down payment, this might mean opting for a less expensive car or home so that the lump sum down payment that you have covers a greater proportion of the purchase cost.

Loans vs Credit Cards: Differences in Credit Approval

Not all types of credit are created equal. Personal loans are considered installment credit and are repaid in fixed payments over a set period of time. Credit cards are considered revolving credit, you can keep borrowing to your approved limit as long as you make your minimum payments.

When it comes to credit approvals, one benefit loans have over credit cards is that you might be able to get a secured loan. A secured loan means the lender has some piece of collateral they can recover from you should you stop making payments.

The collateral could be your home, car or other valuable asset, like jewelry or equipment. Having that security might give the lender more flexibility in some situations because they know that, in the worst case scenario, they could sell the collateral item to recover their loss.

The Bottom Line

Borrowing during a financial downturn can be difficult and it might not always be the answer to your situation. Adding to your debt load in a weak economy is a risk.

For example, you could unexpectedly lose your job and not be able to pay your bills. Having an added monthly debt payment in your budget can add another challenge to your financial situation.

However, if you can afford to borrow funds during an economic recession, reduced interest rates in these situations can lessen the overall cost of borrowing.

These tips can help tidy your finances so you’re a more attractive borrower to lenders. There’s no guarantee your application will be accepted, but improving your finances now gives you a greater borrowing advantage in the future.