Maybe you just sat in the doctor’s office and listened to them explain the diagnosis.

Most people can tell you the exact moment they were diagnosed with diabetes. They didn’t know anything about the disease before they had it.

After you’ve been told you’re health has some serious problems, you start thinking about the future. You realize you aren’t indestructible.

This is the moment when a lot of people start shopping around for a life insurance policy, but it isn’t as easy as buying a new cell phone.

It’s not impossible to get life insurance with diabetes, but you need to do your homework first.

Table of Contents

- Diabetic Stats, and Why Diabetes Is a Risk for Life Insurance

- Why Life Insurance Matters for People With Diabetes

- How Companies View Different Types of Diabetes

- The Best Companies for People With Diabetes

- No Exam Life Insurance for Applicants With Diabetes

- Possible Ratings for Applicants With Diabetes

- Evaluating and Comparing Life Insurance Ratings and Premiums

- Getting Coverage as an Applicant With Diabetes

Diabetic Stats, and Why Diabetes Is a Risk for Life Insurance

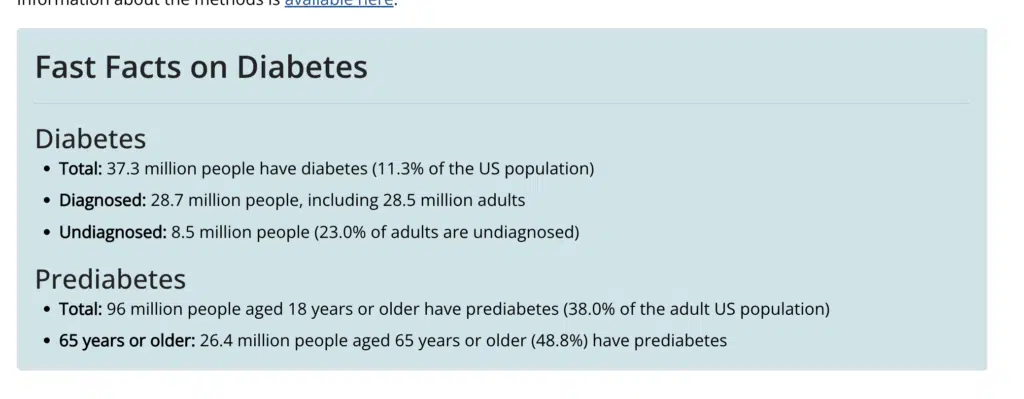

Diabetes is becoming more and more common. Every year, the Centers for Disease Control and Prevention (CDC) completes a report about diabetes and its impact on the United States.

The numbers from 2022 were more shocking than most people expected. There are more than 37 million people diagnosed with diabetes. The CDC reports another 8.5 million Americans with diabetes which hasn’t been diagnosed.

Not only is it common, but it’s also deadly. Diabetes was the seventh leading cause of death in 2021, with almost 90,000 passing away with diabetes as the leading cause.

While anyone can be diagnosed with diabetes, there are groups of people who are at a higher risk than others.

Mainly American Indians, African Americans, and people of Hispanic descent. American Indians were a whopping 15%, African Americans accounted for more than 12%, and Hispanics were another 12%.

Why Life Insurance Matters for People With Diabetes

Life insurance is vital for anyone, regardless of health conditions, but it’s even more so for anyone who has a serious health problem.

If you’re living with diabetes, you know it’s an expensive condition. The medical bills can quickly rack up, and you can find yourself with debt up to your eyeballs.

The worse your health is, the more medical debt you may have. If something were to happen, and you passed away, all of those medical bills and diabetes-related expenses are going straight to your family members.

Having a life insurance plan in place can give you peace of mind knowing this won’t happen. Your diabetes diagnosis won’t stop you from getting one of these plans.

How Companies View Different Types of Diabetes

Not all diabetes diagnoses are the same. The kind and severity of the condition are going to play a huge role in life insurance coverage.

We are going to look at the kinds and how they will change the coverage.

Type 1

Type 1 diabetes (formerly known as Juvenile Diabetes, but also T1D), is one of the least common types of diabetes, but it’s also one of the most severe. In spite of all the research, experts are still not 100% sure what the causes of Type 1 are.

Type 1 requires a lot of attention with insulin and medications since the body doesn’t make any insulin, and it can create some serious problems.

Applicants can still get approved for a life insurance policy, even with this severe condition.

Type 2

Type 2 is the most common kind of diabetes and it can come from lifestyle choices or hereditary conditions.

Your pancreas produces the insulin, but your body isn’t using it effectively. Because insulin isn’t being used properly, the body can’t manage blood sugar levels.

Between the two main types, life insurance for type 2 diabetics is much easier to get, and usually comes at a lower cost, too.

Gestational

When you’re pregnant, your body goes through a lot of changes. One of those is your insulin resistance.

Your body is going to nourish the baby as much as possible, part of this is making glucose for the baby. Your body needs more insulin, but sometimes the body can’t keep up with the extra needs, which can cause blood sugar to go up.

For most people, gestational diabetes isn’t a permanent condition. After the pregnancy, the body should go back to normal, and blood sugars should level out.

The Best Companies for People With Diabetes

If you’ve never shopped for life insurance as an applicant with diabetes, you’re going to run into a few roadblocks.

Not every carrier is going to take the risk to give people with diabetes insurance protection.

Some companies have worked to tailor their plans to those with diabetes.

These carriers have done the research and tweaked their algorithms to ensure they are giving the best plans to those with any type of diabetes.

AIG

AIG is not only one of the largest carriers on our list, but they are also one of the best for people with diabetes. The beginning of AIG goes all the way back to 1919 in China. They are about to celebrate 100 years in the market.

There are a lot of factors they look at when you apply with AIG. Depending on when you were diagnosed (preferably after 60), and your A1C levels, you may be able to get standard rates for AIG. With most companies, you can’t get anywhere near standard rates.

Prudential

You’ll probably recognize their mountain logo. They have spent a lot of money sponsoring events and marketing their products.

Prudential sells several guys of plans. All of their “Pru” options will give you plans you can afford. Through the years, they have carved niches in various kinds of high-risk applicants, like those with diabetes and they were the first to sell insurance to people living with HIV.

For years, they’ve been the leading force in giving less-than-perfect candidates perfect rates.

Protective

Protective was established in 1907, and they have excellent ratings. They hold an A+ grade from A.M. Best. They have been around for a long time, but they continue to impress all of the third-party grading companies.

Protective A1C views are more liberal than other carriers. We see a lot of applicants get better rate classes compared to what they received from other carriers.

They also tend to have faster underwriting than other companies. If you’re worried about having to twiddle your thumbs for months, Protective should be your go-to.

ANICO

American National Insurance Company isn’t new. They aren’t the most well-known companies out there, but they have over 5 million policyholders across every state and Puerto Rico.

In 2021, they were rewarded with Forbes as a member of the “Most Trustworthy Financial Companies” list.

One area where ANICO shines is with their no exam options. They have great rates for anyone willing to skip the medical exam (they have good rates for traditional exam policies as well).

Foresters

In general, Foresters has excelled at selling life insurance to anyone with health problems. Through the years, they have accepted applicants who would be rejected at just about every other company.

If you’ve had problems getting rejected by other companies, Foresters could be your backup option. The one negative of this company is their rates. While they might accept the extra risk, they are going to charge you for the protection.

No Exam Life Insurance for Applicants With Diabetes

More and more companies are boasting about their no-exam options. In today’s culture, we don’t want to wait for anything.

With the traditional insurance plan, you could sit around waiting for life insurance for more than a month. One of the benefits of no-exam life insurance is the speed.

Even without the medical exam, the company will still ask you about a hundred different questions. They will want to get as much information as possible to fill in the gaps.

The big caveat of no exam plans is the premiums that come along. Less info means more risk to the company. More risk means higher premiums.

Possible Ratings for Applicants With Diabetes

As we mentioned earlier, carriers and agents are going to dive deep into your personal info. They are going to explore a lot of factors.

They will want to know:

- Age

- Weight/Height

- A1C Numbers

- Job

- Heart Rate

- Cholesterol

- Prescriptions

Because there are so many factors, and each carrier will put different weights on these factors, the rate class you get could be wildly different depending on the company.

Each company has different rates and views towards people with diabetes.

The highest rate class an applicant with diabetes can get is standard. As long as the applicant is in “relatively good health” and has a reasonable A1C level (around 7).

If you have other health problems, aside from diabetes, then you’re going to be put in a substandard rate class.

Evaluating and Comparing Life Insurance Ratings and Premiums

Understanding the rating systems and how different companies assess risk is instrumental in making enlightened decisions. The spectrum of ratings, influenced by a myriad of factors from A1C levels to lifestyle, guides the premium structures.

By actively comparing and analyzing these ratings and the associated costs across different companies, applicants can discern patterns, identify advantageous options, and navigate toward choices that offer value, affordability, and substantial coverage.

Getting Coverage as an Applicant With Diabetes

Diabetes can add a lot of complications to daily life. It can make simple things a little more difficult, buying life insurance is no exception.

If you’ve applied before and you were declined, or you were accepted but with a massive price tag, don’t give up hope.

You probably picked the wrong carrier. Most people do.

You don’t have to be an insurance genius to find a company that sells cheap life insurance for diabetics. All it takes is dedication and a little work.

You can start by contacting the 5 companies we mentioned above.