Anyone who drives will likely know that insurance is a necessary part of the experience. In fact, at least some amount of coverage is a requirement in most states.

But finding the right type and amount of car insurance is something that may not be as easy as you think.

While following state-mandated guidelines may be one way to give yourself a starting point, it may not always be the very best way to go about getting yourself the coverage that you really need because when push comes to shove, you could come up short if you get into an accident and need to file a claim.

While most people carry their car insurance card somewhere in their wallet or glove box, how much do you really know about the coverage that you pay for each month? Getting a primer on what you’re actually covered for – and what you may be paying for that you don’t need, and vice versa – could make a big difference the next time you go out looking for a new policy.

Table of Contents

Car Insurance 101

In its most basic sense, most auto insurance policies are divided into a couple of basic types of coverage. These include:

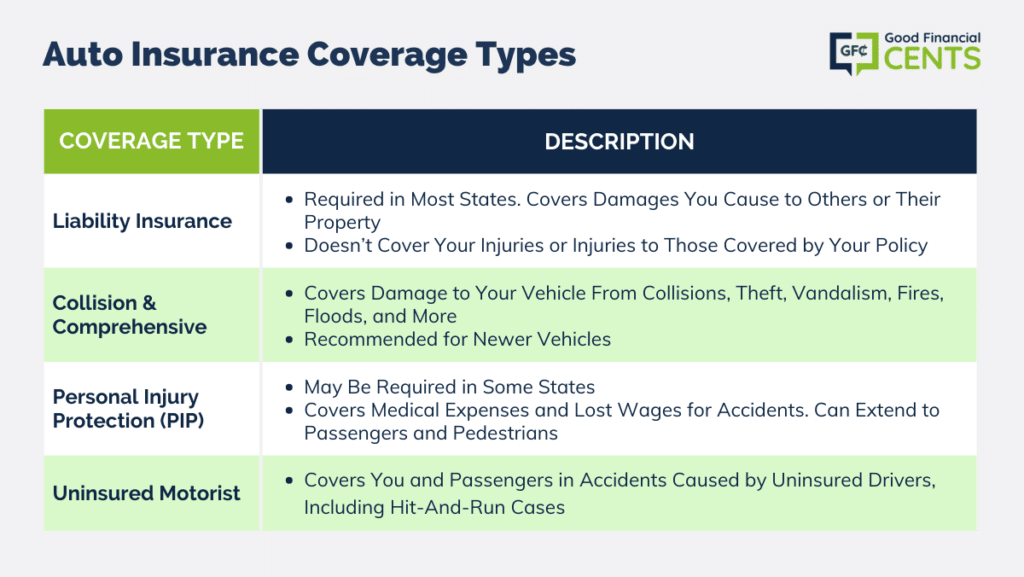

Liability Insurance

Most states require that drivers carry at least a minimum amount of liability coverage. This is the coverage that will pay the cost of damages that you do to others – either people or objects – with your vehicle.

It is important to understand that liability coverage does not cover your own injuries or injuries to other people who are covered under your auto insurance policy.

Typically, liability insurance is stated as a series of three numbers. For example, your policy may show it as: 50 / 200 / 25. What that means is that you have the following coverage:

- The first number means that you have $50,000 (in this particular example) in coverage for each person who is injured in the accident.

(Remember, this coverage does not include injuries to you or others who are included in your policy.)

- The second number refers to the total amount that the policy covers, in thousands, for each accident. In this example, the total amount of coverage would be $200,000.

- The third number refers to the amount of property damage that would be covered in thousands. In this particular example, the amount of property damage covered would be $25,000.

Collision and Comprehensive Coverage

In addition to liability coverage, auto insurance policies can also cover collision and comprehensive damage.

This refers to the coverage for damage to your vehicle if it hits – or is hit by – another vehicle or object.

While many drivers who own older and less valuable vehicles may not carry this type of coverage (or they may carry very low levels of this coverage), collision and comprehensive coverage does make sense for those who own newer vehicles, as the cost to repair and/or to replace these vehicles can be quite high.

Personal Injury Protection

Personal Injury Protection, or PIP, is oftentimes also referred to as no-fault insurance. Like liability coverage, this can also be required coverage in some states.

This type of auto insurance covers medical expenses – and sometimes lost wages – if you have been hurt in an accident. In some cases, the policy might also cover passengers in the vehicle, as well as pedestrians.

Uninsured Motorist

Having uninsured motorist coverage can help to cover both you and your vehicle passengers if you are involved in an accident that is caused by a driver who does not have insurance. This type of coverage can also cover hit-and-run accidents.

How Auto Insurance Policies Are Priced

When obtaining auto coverage, there are many factors that go into the potential price of a policy.

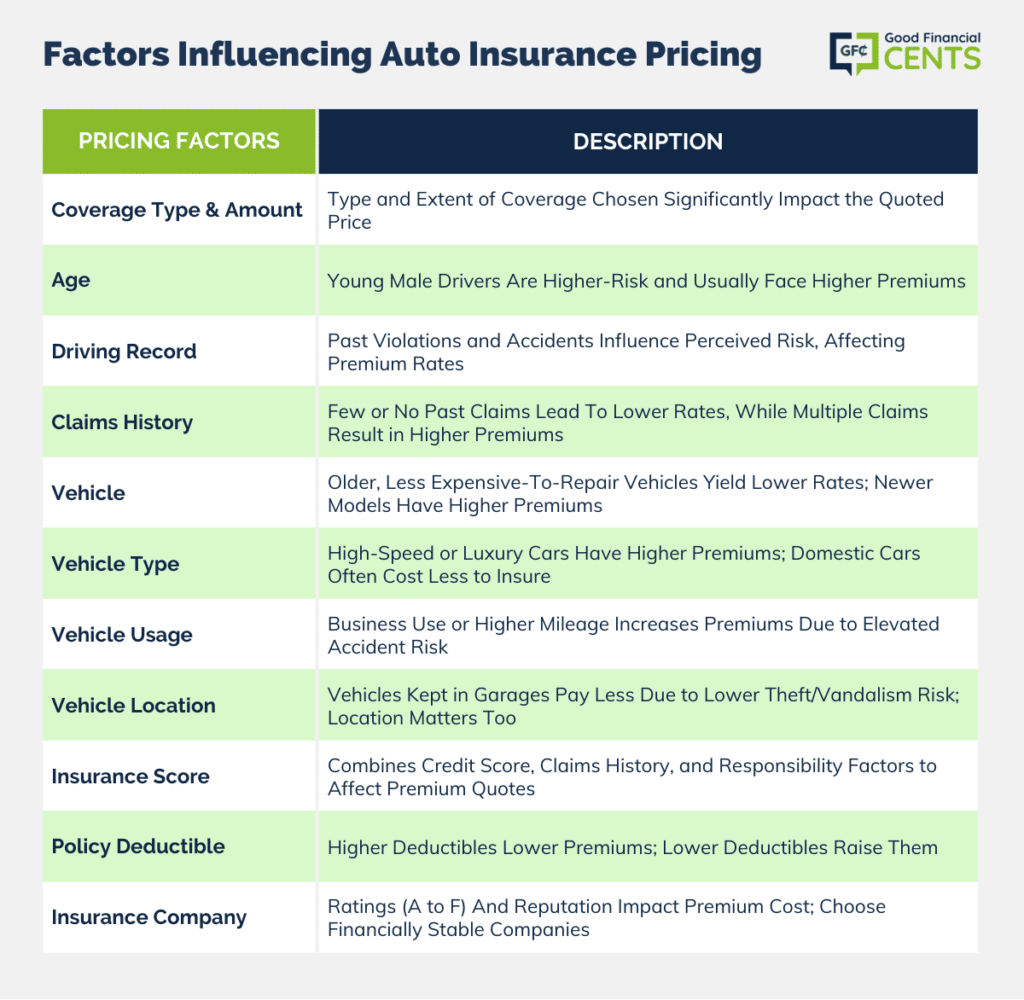

First, these will include the above criteria. The type of coverage that you choose, as well as the amount of coverage that you decide on, will have a big impact on the price that you are quoted.

The following criteria will affect the auto insurance prices you are quoted:

Age

The age of the driver / insured can play a big part in the price of the premium that you are quoted. This is especially the case if the driver is a young male – as statistically, these are the riskiest drivers to insure for auto insurers.

For this reason, rates for a 20-year-old male driver will usually be much higher than they are for a 40-year-old female.

Driving Record

The driving record of the vehicle owner will also be a key determinant in how much you are quoted. Your driving record reflects any moving violations, such as tickets or DUIs, that you’ve had in the past, as well as any accidents that have been reported.

This also shows the auto insurer how much of a risk you may be to insure. More violations and/or accidents on your record can mean more risk to the insurance company, and in turn, this can mean a higher premium for your personal policy.

Claims History

Past claims history is another big criterion that the adjusters will take into account. This is another way to show how risky of a driver you have been in the past.

If you have little or no past claims history, then it is likely that you will not be seen as a high risk to the insurance company, and you will likely be rewarded with lower rates than someone who has recently filed one or more claims.

If, however, you have filed many claims, then it is likely that you will be quoted higher auto insurance rates going forward.

Vehicle

In addition to the driver, the vehicle that you are insuring will also have a bearing on the amount of premiums that you pay.

For example, if you drive an older model vehicle or a vehicle that is not very costly to repair or replace, or even if you need RV insurance, then you likely will not be quoted very high rates.

However, if your vehicle is a newer model that would be expensive to repair or replace, then your car insurance quotes will likely be much higher.

Owning a vehicle that has the capacity (or temptation, depending on the driver) to move faster on the roads will also be quoted higher rates in most cases.

For example: a bright red sports car will typically be more expensive to insure than a grey minivan.

Finally, having a vehicle that is not manufactured domestically will tend to have slightly higher rates because the parts to repair these vehicles tend to run more than parts manufactured inside the United States.

Vehicle Usage

The amount and how you use your vehicle also play a major role in the overall cost of your premiums.

First, the insurer will want to know whether you use the vehicle for business or personal use.

You can expect to pay higher rates if you are using the vehicle for transporting business people around on a regular basis versus simply driving the vehicle to and from work by yourself.

Also, you will be asked how many miles, on average, you drive. Those who drive more miles per year will typically pay more for their insurance than those who drive less.

This is because the odds of getting into an accident are higher for those who are in their vehicles and on the road more often.

Where the Vehicle Is Kept

Where you keep your vehicle is another key factor in the price of your auto insurance. The insurer will want to know if you keep your vehicle in a garage or driveway or parked on the street at night.

Those who park safely in a garage at night will generally pay less for coverage than others since vehicles are safer from theft and vandalism, as well as from the elements. Your geographic location can also make a difference.

Those who live in areas that get poor winter weather may have to pay more for auto coverage than those who drive on roads that are primarily dry and warm year-round.

Insurance Score

A person’s “insurance score” is a new factor that has come into play with insurers over the past several years. This score takes into account your credit score, past claims history, and other related factors that rank how responsible you are.

The higher your credit score, for example, and the lower your past claims history, the better your insurance score will typically be, thus the lower your auto insurance quotes are likely to be.

Policy Deductible

There are several types of insurance policies – including auto insurance – that require the policyholder to pay a policy deductible.

With deductibles, you are required to pay a certain amount of money out of pocket towards the repairs on your vehicle before the policy will pay for the remainder of the charges. In most cases, deductibles will range from between $250 to $1,000.

If persons A and B have the same exact coverage, except that person A has a $250 deductible and person B has a $500 deductible, person B will have lower premiums each month.

If you have a good emergency fund in place, you can handle a higher deductible and save yourself money on premiums.

The Company

In addition to all of the factors above, the auto insurance company can have a lot to do with the price that you are quoted.

Auto insurance companies are provided with letter ratings from A to F – similar to a school report card – from rating agencies such as A.M. Best, Standard & Poor’s, Moody’s, and Fitch.

It is usually best to stick with companies that have ratings of A or better.

You should always review the financial stability and claims-paying reputation of the insurer prior to deciding on where to purchase your auto policy. The company that offers the lowest quote may not always be the best company to go with.

Where to Look for the Best Quotes Now

When looking for quotes, it is best to work with a company that has access to more than just one insurer.

This way, you will be able to compare several policies – along with the many features and benefits – as well as a wide variety of unbiased premium quotes.

If you’re ready to begin shopping for car insurance quotes, we can help you to find all of the important information that you’re looking for – and we can do so quickly, easily, and conveniently – directly from your home computer, and without the need to meet in person with an agent.

In order to get the process started, all you have to do is simply use the form on this page.

When shopping for insurance, whether it be auto, health, life, or even burial insurance, it can sometimes seem overwhelming.

There’s a lot of information out there – and it’s hard to determine where you’ll truly get the very best deal. Use the form on this page to help you to narrow down your options and to find the plan that fits your needs, along with the premium that fits your budget.

- QuoteWizard Comparison Platform saves an average of $65 a month

- Millions served since 2006

- No personal information required for quotes

- Get low rates from top companies

- Over 43,000 local insurance agents

Bottom Line: Getting the Right Auto Insurance Quotes for You

Navigating the world of auto insurance can be complex, but it’s vital for every driver. Understanding the coverage options is crucial. Liability insurance covers damages to others, while collision and comprehensive protect your vehicle.

Personal Injury Protection (PIP) and uninsured motorist coverage provide added security. Factors affecting premiums include age, driving record, claims history, vehicle type, usage, location, insurance score, and policy deductible.

Use online tools to compare policies and premiums conveniently. Ultimately, prioritize comprehensive coverage that meets your needs and budget.