According to the AIG Life Insurance IQ Study, 51% of Americans either don’t know if they have a life insurance policy or don’t have one at all. Although 70% of respondents acknowledged that life insurance could protect their family’s chances of living a financially stable life, many still go uninsured.

What many don’t realize is life insurance premiums are most affordable when you’re young and healthy. And you’ll never be younger or healthier than you are today which means your premiums could be at the lowest they’ll ever be.

Even if you have chronic health conditions or you’re not so young anymore, it’s still worth making sure you have life insurance now rather than waiting until it’s even more expensive.

Whether you’re buying your first insurance policy or getting a second policy because your needs have changed, learn more about the options that are available.

Table of Contents

How to Get Life Insurance Quotes

You can certainly go from website to website, getting quotes from each individual insurance company. But you can also use life insurance brokers to find the best policies for your situation, or even rate-shopping life insurance marketplaces.

Most people obtain life insurance in this way, but be forewarned: the underwriting process can take a long time (months, even), and require a lot of hassle on your part.

Another option if you need life insurance faster and more conveniently is to use a company like Bestow or Ladder, which allows you to get coverage within minutes, in some cases.

Compare Average Rates

Next to getting quotes from multiple sources, it’s also important to compare rates between different policy types. For now, we’ll focus on term life insurance.

It also has easily adjustable coverage, based on your life events.

According to a study by S&P Global Market Intelligence, the discovered the average life insurance premium for all types (term, whole, variable, etc.) was just over $990.

For this comparison, we’ll use Quotacy, an insurance marketplace, to look at premiums for term policies in three policy increments:

For comparison, we’ll use Quotacy, an insurance marketplace, to look at where you can generally expect rates to start when compared across multiple companies. We’ll look at premiums for term policies in three policy increments:

We’ll also compare these increments across different term lengths (10 years, 20 years, and 30 years), based on ages 25, 35, 45, 55, and 65.

Term Life Insurance Quotes for Males

| Age at Policy Purchase | Death Benefit | 10-year Term Monthly Premium | 20-year Term Monthly Premium | 30-year Term Monthly Premium |

|---|---|---|---|---|

| 25 | $250,000 | $9.75 | $12.26 | $17.72 |

| 25 | $500,000 | $13.64 | $19.11 | $28.68 |

| 25 | $1 million | $20.04 | $30.59 | $48.25 |

| 35 | $250,000 | $9.77 | $13.45 | $21.09 |

| 35 | $500,000 | $14.06 | $21.24 | $35.24 |

| 35 | $1 million | $21.92 | $33.99 | $64.51 |

| 45 | $250,000 | $16.81 | $26.42 | $42.88 |

| 45 | $500,000 | $27.62 | $46.44 | $79.38 |

| 45 | $1 million | $46.81 | $87.87 | $151.21 |

| 55 | $250,000 | $37.48 | $61.26 | $120.71 |

| 55 | $500,000 | $67.57 | $114.74 | $232.23 |

| 55 | $1 million | $123.24 | $221.61 | $457.05 |

| 65 | $250,000 | $101.76 | $199.16 | Custom Quote Only* |

| 65 | $500,000 | $191.29 | $385.08 | Custom Quote Only* |

| 65 | $1 million | $362.69 | $743.72 | Custom Quote Only* |

*Available by custom quote only since a 30-year policy extends to age 95, practically guaranteeing a death benefit payout. The insurer will need to do a full underwrite to offer a quote.

Term Life Insurance Quotes for Females

| Age at Policy Purchase | Death Benefit | 10-year Term Monthly Premium | 20-year Term Monthly Premium | 30-year Term Monthly Premium |

|---|---|---|---|---|

| 25 | $250,000 | $8.61 | $10.79 | $14.68 |

| 25 | $500,000 | $11.22 | $15.72 | $22.73 |

| 25 | $1 million | $15.81 | $23.05 | $37.82 |

| 35 | $250,000 | $8.92 | $11.94 | $18.28 |

| 35 | $500,000 | $11.96 | $17.87 | $29.69 |

| 35 | $1 million | $18.92 | $29.91 | $52.15 |

| 45 | $250,000 | $15.15 | $21.33 | $33.51 |

| 45 | $500,000 | $24.22 | $37.41 | $61.32 |

| 45 | $1 million | $38.24 | $67.91 | $116.36 |

| 55 | $250,000 | $28.21 | $45.38 | $91.54 |

| 55 | $500,000 | $50.05 | $84.39 | $176.50 |

| 55 | $1 million | $90.94 | $158.86 | $330.74 |

| 65 | $250,000 | $64.97 | $134.30 | Custom Quote Only* |

| 65 | $500,000 | $122.14 | $257.70 | Custom Quote Only* |

| 65 | $1 million | $223.86 | $485.77 | Custom Quote Only* |

What Term Life Insurance Quotes Reveal

The quotes in the tables above reveal notable factors that impact a term life insurance quote. Here are a few takeaways:

- The male-female variance increases with age.

- Premiums are significantly higher with a longer policy term.

- Premiums are significantly higher when purchased later in life.

Notice that for 30-year term policies for 65-year-olds, a custom quote is required regardless of the death benefit. That’s likely because after a certain age, your health is more likely to become a big risk factor.

This is precisely why it’s so frequently recommended you purchase life insurance as early in life as possible.

Other Factors That Affect Life Insurance Premiums

While it’s true enough that age and gender are two of the most basic factors in determining life insurance premiums, there are many, many more.

Your Health

This is a complicated factor since the possibilities are so extensive. You can have relatively minor health conditions, like well-controlled hypertension, that result in only a slight increase in your monthly premium.

| More serious health conditions, like diabetes, heart disease, or kidney disease, can cause premiums to climb higher. |

The same is true with one-time events, like a battle with cancer.

If you have or have had any of these conditions in the past, your application may be reviewed on an individual basis for risk factors, based on your personal situation. You might also be asked to undergo a medical exam.

When you experience certain health issues is another factor. For example, a cancer episode 10 years ago will have a lesser impact on your premium than a recent diagnosis. Other health-related factors are your weight-to-height ratio, as measured by your body mass index (BMI), and any medications you’re taking.

Family Health History

Even though this is a factor that’s completely beyond your control, it can influence your premium. Most insurance applications ask if anyone in your immediate family has or had any major health conditions.

Immediate family will generally be limited to your parents and siblings. This includes severe health conditions, like cancer, heart disease, diabetes, or kidney failure. Most life insurance companies are primarily concerned with family members who developed major health conditions before reaching age 70, particularly those that resulted in early death.

Smoking and Tobacco Use

Smoking and tobacco use is the single biggest premium determinant within your control. And from a life insurance premium perspective, being a nonsmoker is perhaps the biggest advantage you can give yourself.

The best way to illustrate the impact of smoking is by comparing the premium rates for smokers versus nonsmokers, between men and women. The table below shows the lowest rate quotes across multiple companies from the Quotacy network for a $500,000 20-year term life policy.

| Age at Policy Purchase | Male Nonsmoker | Male Smoker | Female Nonsmoker | Female Smoker |

|---|---|---|---|---|

| 25 | $19.11 | $53.33 | $15.72 | $34.58 |

| 35 | $21.24 | $84.14 | $17.87 | $68.33 |

| 45 | $46.44 | $205.27 | $37.41 | $150.44 |

| 55 | $114.74 | $471.74 | $84.39 | $333.19 |

| 65 | $385.08 | $1131.34 | $257.70 | $844.89 |

Notice the premiums for smokers are several times higher than for nonsmokers.

For example, the premium for a male smoker at age 25 is nearly three times the rate for a nonsmoker. The multiples are approximately the same for female smokers. At age 35, that rises to four times the premium level, where it continues at the same multiple at higher ages.

A 35-year-old male would pay an additional $63 per month for the same amount of life insurance coverage — essentially, paying more than $750 annually for the “privilege” of being a smoker.

The dramatically higher premiums for smokers illustrate the impact of smoking on longevity, and the need for insurance companies to accommodate the greater risk through higher premiums.

According to the Centers for Disease Control, smoking causes over 480,000 deaths per year. Below are examples of how smoking increases your risk of developing certain serious health conditions.

- Coronary heart disease: 2X to 4X

- Stroke: 2X to 4X

- Lung cancer: 25X for men and 25.7X for women

- Chronic obstructive pulmonary disease: 12X to 13X

You should also know life insurance companies consider occasional smoking, cigar smoking, tobacco chewing, and use of e-cigarettes (vaping) in the same light.

Other Behaviors That Affect Rates

Two other pastimes that have a similar effect on life insurance premiums are excess alcohol consumption and illicit drug use. Both of which increase the likelihood of an early death.

It’s not as easy to conceal these habits as you might think. For example, excess alcohol consumption can come to light through one or more DUIs/DWIs, or even alcohol-related incarceration.

Illicit drug use can be determined by a criminal background check, or even through blood tests taken over the years that have revealed the presence of the substances in your bloodstream.

Your Occupation

Admittedly, this one catches most people completely by surprise. That’s largely because the vast majority of occupations don’t represent any kind of risk factor. A small group of occupations have been determined to be high-risk.

According to the Bureau of Labor Statistics, the 10 most hazardous occupations (in order of most fatal work injury rates) are:

- Logging workers

- Fishers and related fishing workers

- Aircraft pilots and flight engineers

- Roofers

- Refuse and recyclable material collectors

- Driver/sales workers and truck drivers

- Farmers, ranchers, and other agricultural managers

- Structural iron and steel workers

- First-line supervisors of construction trades and extraction workers

- First-line supervisors of landscaping, lawn service, and groundskeeping workers

Those are just the 10 most hazardous. But there are other occupations, like police officers and firefighters, that are also considered to be higher-risk occupations.

If you fit into one of these occupational classifications, you’ll pay an adjusted premium based on your occupation’s high risk of death.

Risk Factors Affecting Your Life Insurance Premium

- High-risk hobbies. What you do in your spare time impacts your life insurance premiums. Certain activities, like skydiving, racing of any type, deep-sea diving, backcountry skiing, rock climbing, and many others, are considered high-risk.

- Your driving record. If you have multiple moving violations or one or more at-fault accidents, you’ll pay a higher premium, especially if you have a DUI/DWI on your record.

- Your credit history. Life insurance companies have detected a connection between poor credit and higher rates of mortality. This could be the result of financial stress impacting credit, but it also with the potential to affect your health and behavior.

- Your criminal record. If you have any convictions in your past, especially within the last few years, it could have an impact on your premium. The age and nature of the incident are significant. For example, a criminal conviction 25 years ago might have no impact at all. But one from five years ago, might.

Whole Life Insurance Rates

Some consumers might be interested in whole-life insurance. If so, all the above risk factors that determine premiums for term life coverage, apply to whole life insurance.

The main differences between whole life insurance and term life are:

- The whole life is permanent. Once you sign up for a policy, it provides lifetime coverage except for non-payment of a premium.

- A whole life can include a cash value accumulation. Part of your premium can go into the cash value of your policy. The cash value also earns interest, which further increases the balance. You can take loans against that cash value.

- The premium never changes. Whether you pay annually, quarterly, or monthly, your whole life insurance premium will remain the same for the rest of your life. This is unlike term life insurance, where the premium will adjust if you renew the policy after the original one expires.

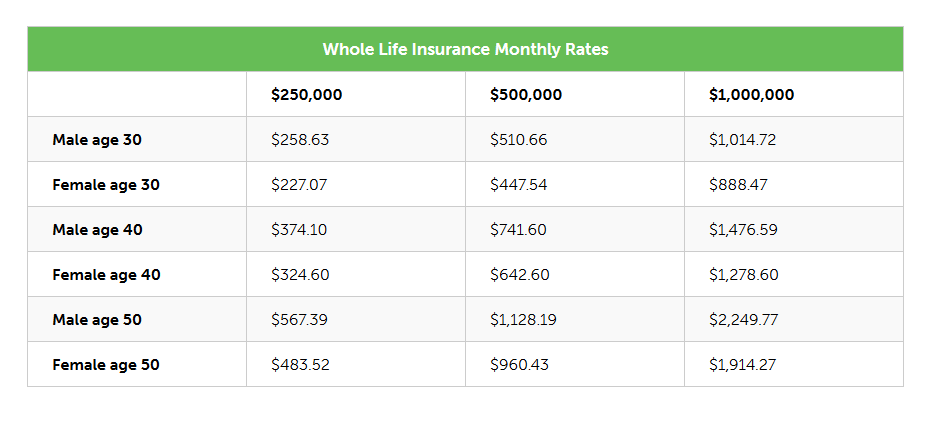

- Whole life insurance can cost a lot more. Whole life insurance is generally 10 to 15 times higher than term insurance for an equivalent death benefit, according to Quotacy. A difference between the two premiums is the portion of whole-life premiums that go toward your cash value.

Below are samples of whole-life quotes from Quotacy, on similar policy amounts at different ages for both males and females. Again, these are where rates start from when comparing across multiple companies, not necessarily the averages or even what you might pay.

*Image courtesy of Quotacy

Insurance agents often promote the idea of the cash value feature of whole life insurance. You can earn a guaranteed rate, although it might be lower than you can get elsewhere. It’s best to purchase a whole-life policy based on the death benefit, however, and treat the cash value as just an added perk.

Some of the whole life premium goes toward commissions and fees — especially in the first few years of the policy.

How to Purchase Life Insurance

When applying for life insurance, supply as many details about your personal profile as possible, particularly about your health, occupation, hobbies, smoking status, and family health history. The more accurate the information you provide, the more reliable the premium quote you’ll receive.

If you have any health conditions or activities that might affect your premium, submit an application with one of the best life insurance companies we recommend that can accommodate specific risk factors you have. Some insurance companies are known to specialize in special situations. For example, some insurers offer tailored life insurance policies for those over 50.

It’s strongly recommended you first look at term life insurance. Term life insurance can be a more affordable option. For example, it’s helpful when you have a young family. In this scenario, you’ll need more life insurance but may likely have a small budget to work with. Term life can let you buy more coverage you can adjust up or down as things in your life change.

Whether you apply for term or whole life, the process starts by getting a quote. From there, you’ll likely need to fill out a more detailed application with the insurance company that will be providing your policy. They may or may not require you to submit to a medical exam.

Once you’ve chosen a life insurance policy, the insurance company will request the first premium installment upfront. By making a payment, your policy goes into effect as of the date of application, subject, of course, to the insurer’s approval.

Finding the Right Life Insurance Policy

We strongly recommend — as do some financial advisors — that you go with a term life insurance policy. It’s not just that it’s less expensive, but that frees your cash flow for other purposes, like investing it yourself or securing a new home.

Premiums vary by gender, age, personal profile, and even geography, so shop around to get the most coverage at the lowest cost.

Life Insurance FAQs

Some financial advisors recommend you have at least 10 times your annual salary in life insurance coverage. For example, if your salary is $50,000, $500,000 is the minimum recommended.

Employer-sponsored life insurance is a good benefit to have, but in most cases, it’s insufficient. Typically, it only covers one or two times your annual salary. Another downside to relying on employer-sponsored life insurance is that it’s tied to your employment. If you leave your job or are terminated, you’ll lose your life insurance.

It might not matter if you don’t have any dependents, like a spouse, children, or anyone else who might be dependent on your income. But if you do, having no life insurance could put their financial survival at risk in the event of your death. Life insurance can help provide for your loved ones after your death — or at least cover your final expenses.

You might need to consider a guaranteed acceptance life insurance policy. This is the policy type an insurance company offers if you don’t qualify for traditional life insurance.

The death benefit is limited to not more than $50,000, and often a lot less. The premium is also high compared to the death benefit. At the very least some life insurance coverage can help if you’re in poor health, and can provide sufficient funds to cover your final expenses.