“How does an annuity work?”

“How do annuities differ from other investments?”

“Is an annuity really right for me?”

These are some common questions people have when it comes to annuities.

Why is there so much confusion surrounding annuities? It’s because there are several different types of annuities, all with varying terms and rider options, and many financial advisors (or insurance agents) either explain them poorly or purposefully blur the definitions in order to push one product over another.

I’m here to clear up the confusion and encourage you to carefully consider whether an annuity might be a smart investment option for you. They get a bad rap and they’re definitely not right for everyone, but there are real scenarios when an annuity makes a lot of sense.

Table of Contents

What Is an Annuity and How Do They Work?

An annuity is a fixed amount of money that is paid to someone every year. Boom, we can all go home. Ha, not quite.

Annuities typically seek to lower the risk an investor takes by making one thing certain: regular income. While the benefit might give you peace of mind, it’s not necessarily the best benefit if the money you’re receiving ends up being less than what you could get from other, albeit riskier, investments.

So really, there are two factors to understand about annuities:

- First, they have the potential to lower your risk when chosen over, say, stocks.

- Second, they have the potential to lower how much money you make when chosen over, say, stocks!

This is really important. I’ve seen people scammed into buying ridiculous annuities that have outrageous fees.

Don’t believe me? Read how one woman paid over $3,500 in variable annuity fees and didn’t even know it.

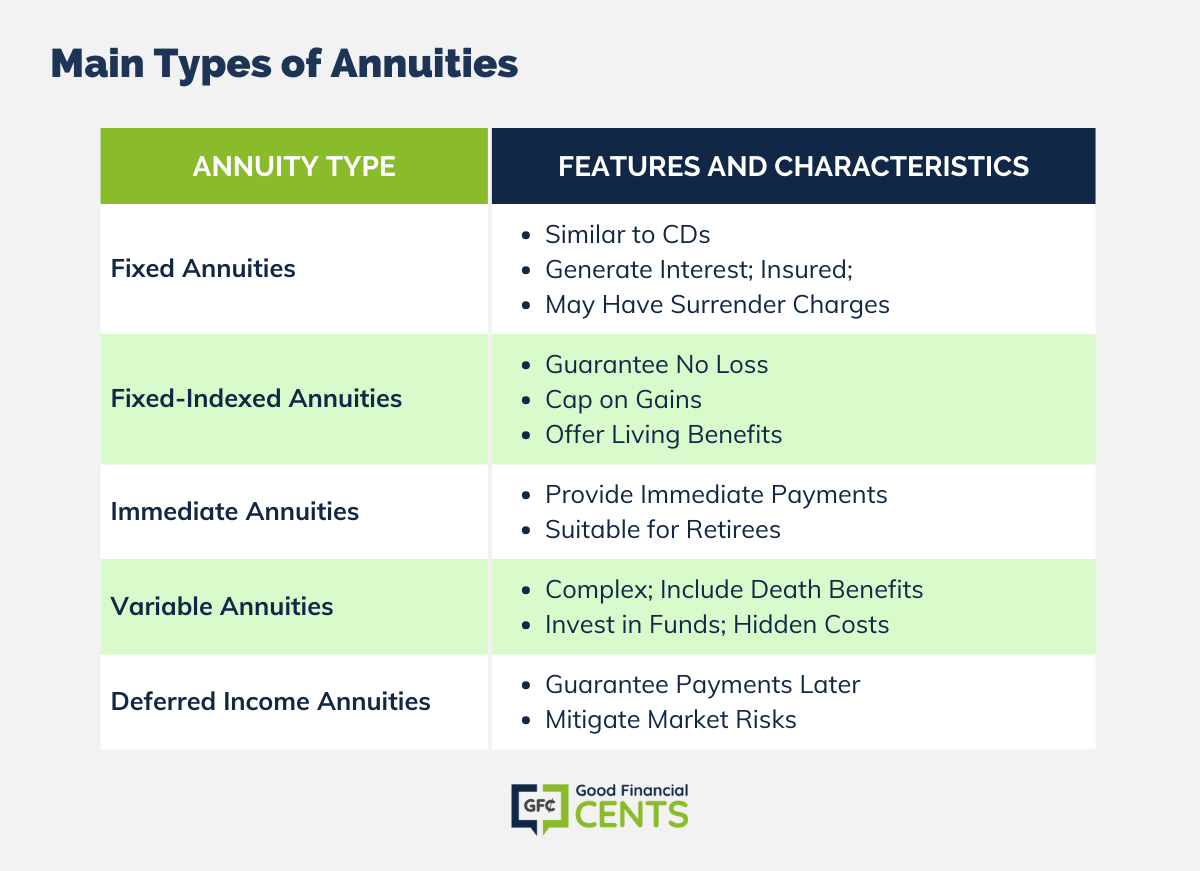

The Main Types of Annuities, Broken Down

To better understand how annuities work, let’s look at some types of annuities and their main features. Keep in mind, that there are other types of annuities as well, but these are some of the most common.

Fixed Annuities

These are very similar to bank CDs or savings accounts. You put in an amount of money, and that money generates interest. This interest is then added to the account.

Pretty straightforward, right?

They are insured by an insurance company, not the FDIC. So, like CDs, fixed annuities are insured, but remember that insurance companies are less stable than the FDIC. It’s possible that an insurance company that sold fixed annuities to you could go under, and if that happens, you might lose your money. The chances of this happening are probably very low, but it’s worth mentioning.

For this reason, ratings are very important. There are several agencies that test the financial strength of companies that issue annuities. I recommend doing a simple search online for these ratings before deciding which company to go with.

Other differences between fixed annuities and CDs include:

- If you surrender an annuity prematurely, you may have to pay a surrender charge on the principal (versus just losing your interest in a CD)

- Annuities are subject to retirement account rules since the interest is tax-deferred. So if you surrender an annuity prematurely, you may also be subject to a 10% penalty from the federal government.

Annuities are supposed to lower the amount of risk you take on in your investing strategy. And, while fixed annuities are certainly on the safer end of the spectrum, the above penalties should be factored in as a risk when you’re considering purchasing a fixed annuity. Even if you don’t intend to surrender, life’s circumstances may prompt you to do so, resulting in a loss.

While those are some negatives about fixed annuities, there’s one positive that’s especially worth mentioning: the rates are usually higher with fixed annuities than with CDs.

I remember I once had a client who wanted a guaranteed return but CDs weren’t paying anything. I found him a 5-year fixed annuity paying 3%, which was significantly better than the measly returns CDs were paying. If you need help finding the best annuity quotes for your needs, use the form on this page and we’d be happy to help!

But, remember, fixed annuities aren’t right for everyone. When I was young, my mom wanted to set me up with an investment. What did she choose? You guessed it: a fixed annuity.

At the time I really didn’t know there were much better investment options out there for me. You know, ones where I could take more risk because I had practically my whole life ahead of me. I appreciated what my mom did for me, but I ended up cashing out and opening a Roth IRA. I found out later that my mom’s financial advisor was an insurance agent, and their recommendations can sometimes be skewed. Make sure you know what you’re signing, and look for a professional you can trust who will take the entirety of your financial situation into consideration.

Fixed-Indexed Annuities

A fixed-indexed annuity (also known as a “hybrid annuity“), guarantees that you can’t lose money. Try getting that benefit by investing in the stock market!

Of course, there’s also a downside: most have caps. That means if the stock market is doing really well and the index skyrockets, you probably won’t earn as much as you could have if you’d invested straight into the market. This isn’t true of all fixed-indexed annuities, though. Make sure you completely understand what you’re buying.

Fixed-indexed annuities also offer living benefits, which can provide an income for your life as well as to your spouse in the event of your passing.

Most of the confusion regarding these types of annuities is in regard to the fuzzy details that shady advisors provide.

If an advisor pitches you a product that “guarantees a 6% return without any risk to your principal”, this advisor doesn’t care about you and all they are doing is trying to do is make a sale.

Do these annuities offer a 6% (or whatever number) return? Well, kind of. It’s not interest earned on your principal, like how you’re used to thinking about bonds or CDs. Instead, this is added to your future income benefit that you can take at a later time, like during retirement.

It’s very similar to the way Social Security benefits increase for each year you delay taking it. Same deal here.

Really, understanding how fixed-indexed annuities work is fairly simple, as long as you’re working with an advisor who has your back and isn’t only interested in earning the quick commission.

Immediate Annuities

Immediate annuities provide payments right from the beginning of the annuity’s inception. These payments can be fixed or variable.

These are great for near-retirees or retirees. But, it does mean forking over a lump payment, and after you get past the 30-day “free look” period, there’s no turning back.

This is different from fixed-indexed or variable annuities, where you still have access to the principal (albeit, subject potentially to a surrender charge).

Variable Annuities

I’m going to tell you right up front: I don’t like variable annuities. Variable annuities are quite complicated, and while they may contain a lot of “features” or “benefits” that sound inviting, you have to be careful.

When you hear about “guaranteed death benefits” (a benefit for beneficiaries should the annuitant die before payments begin) and “income guarantees” or “guaranteed withdrawal benefits,” remember to read the fine print to see how they actually work.

Variable annuities contain mutual funds (called “sub-accounts”) that are typically selected from a pool of 80 to 300 funds. While that might seem like a lot, keep in mind that were you to shop the market on your own, you would find thousands and thousands of options to choose from.

Moreover, variable annuities do not guarantee your principal and they bury a lot of hidden costs and fees, in things like mortality expense (M&E), riders, sub-account costs, etc. All in, investors could be paying close to 4%.

If you own a variable annuity and want to know you much you’re really paying, request your free Annuity Stress Test at bfffinancial.com.

Deferred Income Annuities

Deferred income annuities are very much what they sound like you receive guaranteed, lifetime payments at some later date. This “later date” is typically a year or later from the time you start the deferred income annuity.

Why should someone sign up for a deferred income annuity? Because the benefit from a deferred income annuity is likely more than an immediate annuity. Why? Because the insurance company knows that the longer you live, the less time you have on the planet. This reduces the amount of time they may have to make payments to you. Moreover, they don’t have to pay you for a number of years.

Deferred income annuities can be an advantageous part of a retirement plan, providing a tremendous amount of peace of mind! You can purchase a deferred income annuity 10-15 years before retirement, and then rest assured that you will have income at retirement.

Remember the stock market drop after 9/11? How about after the housing crisis? Many retirees found themselves with severe losses in their portfolios after these events. Purchasing a deferred income annuity alleviates much of this concern.

These policies are pretty popular, and they’re worth your consideration. Talk with a comprehensive financial planner to explore this option.

A Simple Annuity Example

To better understand annuities, picture this. Say you have a wealthy uncle who is great at investing in the stock and bond market. He is financially secure and you’re unsure about investing in the stock market because you don’t want to lose money.

So, you make a deal with your uncle. You’ll send him payments over time (or perhaps a lump sum), he’ll go ahead and use his experience and his high tolerance for risk to invest the money, and he’ll send you payments every year that may include a portion of what he has made in the markets.

Now, your uncle wants to teach you responsibility and doesn’t want to provide this service free of charge (or maybe he’s a bit hungry for some more dough), so he’s going to charge you some fees. The fees differ depending on how you set up the deal.

You’re happy because (1) you want your principal protected, (2) you want guaranteed returns, and (3) you like the idea of predictable income. Your uncle is happy because he’s able to use his financial security to make some more money through the deal.

That, in a nutshell, is how an annuity works.

While this is a simple example, remember that annuity contracts aren’t so simple. Again, read them!

How Do Annuities Differ From Other Investments?

I’ve already answered this question somewhat earlier in the article, but let’s dive into a little more detail.

Many investors think of the stock and bond markets when considering where to put their money. So, that’s what we’ll focus on here.

When you buy shares of a stock, you’re buying ownership in a company. The price per share will fluctuate and it is up to the investor to buy low and sell high (to make a profit). However, this isn’t always easy – especially if the investor is buying over short periods of time.

A stock index is a measure of how well a group of stocks are doing as a whole. Perhaps you’ve heard of an “index fund.” Index funds track an index to provide similar returns as you would see from the index.

Bond index funds operate in a similar fashion. However, at the core, bonds are basically debts that are owed to you, the investor.

Now, what does all this have to do with annuities? Well, fixed-indexed annuities track an index (most commonly the S&P 500) but remember, they have constraints on them many times. While you won’t lose the money you put into a fixed-indexed annuity, your potential for index fund-like gains might be limited by caps.

What this means is that you are lowering your risk by going with a fixed-indexed annuity. I like fixed-indexed annuities, but they still aren’t for everyone.

Another way annuities differ from other investments has to do with liquidity. With mutual funds, ETFs, or managed portfolios, if you need the money, it’s relatively easy to get to. Annuities are a different story.

Variable, fixed, and fixed-indexed annuities typically have a contract period that will range from 3 to 12 years – this is why you read the contract before you sign! While most allow an annual free withdrawal (10% per year of the principal plus interest earned is common) any amount above that is subject to a surrender charge. I’ve seen surrender charges as high as 9% before so this could be a huge blow if you were in need of some quick cash.

That’s why I tell anyone who is interested in the security of annuities to never put all of their money into annuities.

Is an Annuity (Really) Right for You?

Maybe.

Typically, I ask investors these questions to see if an annuity makes sense for them:

- “How important is the protection of your principal?”

- “How important is having a predictable income stream in retirement?”

Your answers can be a good indication of whether an annuity is a good choice for you. But, even if you think an annuity sounds great, I STRONGLY recommend you work with a reputable agent who will do a thorough analysis of your financial situation to help you find the right product and terms for your unique situation.

If you have an annuity and aren’t sure if you should continue with it (or how much you’re paying in fees), I offer a free Annuity StressTest.

Bottom Line

Don’t let annuities freak you out. They make sense for some and not for others. Working with a trustworthy financial professional will give you a good understanding of whether an annuity should have a place in your investment portfolio or if another strategy makes more sense.

Thank you so much for explaining Annuities in simple terms. I was just looking for what annuity mean but I could not help myself reading everything about annuities without getting confuse.

“On paper”, a fixed indexed annuity seems to be the best all-around choice. I have two of them (American Equity and National Western). Their upside potential with no risk of principle makes sense. But the “Gotcha!” comes every year when the life insurance companies do their “calculations” to determine what if any gain you’ll receive. It would take a seasoned financial advisor to translate the garbly gook of if’s, and’s and but’s in the contract. Hopefully some federal oversight programs will be put in place to audit what the life insurance companies are reporting. On a related subject: MYGAs. I had 4 of them before converting to fixed index annuities. These are fantastic vehicles for getting a high interest rate with little risk – and you can withdraw portions of the principle.

This reference will be so helpful for anyone who isn’t sure how annuities work. There’s so much in the press about annuities that it’s hard to find one article to read to explain it all. This is definitely one I’ll share with my readers / clients.